Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

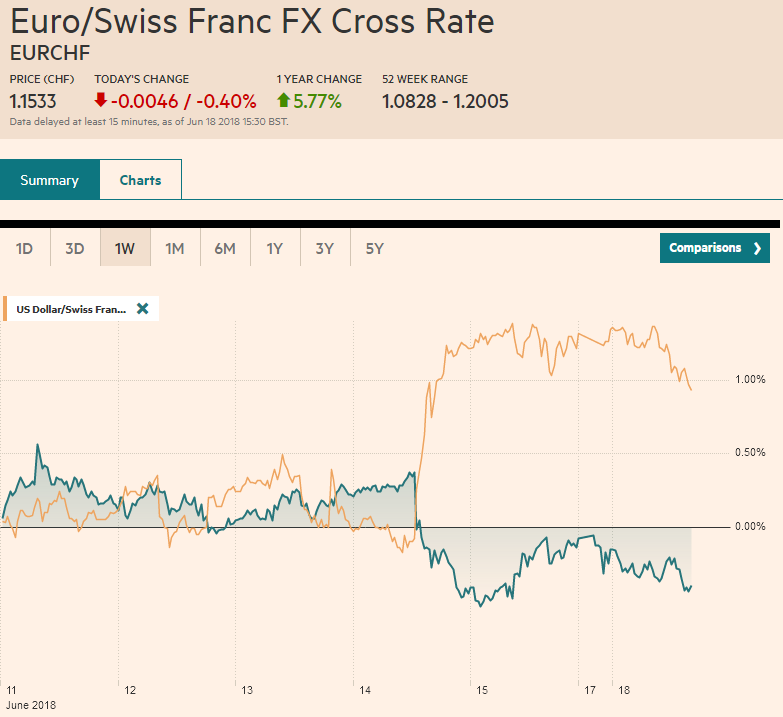

Swiss FrancThe Euro has fallen by 0.40% to 1.1533 CHF. |

EUR/CHF and USD/CHF, June 18(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is rising against most of the major and emerging market currencies. The prospects of escalating trade tensions and the divergence of policy that was confirmed by the major central banks are disrupting the markets. Norway’s central bank meets later this week. It expected hawkish hold may be helping the krone within the Europan complex, but is no match for the US greenback. Still, after some follow-through gains, the dollar’s upside momentum is faltering today, and technically we look for some backing and filling. Turnaround Tuesday may have already begun. China, Taiwan, and Hong Kong markets were closed for the Dragon Boat holiday, but the MSCI Asia Pacific gapped lower. It lost about 2/3 of a percent to extend the downdraft to the fourth consecutive session. No market in the region escaped the sell-off. We note that the strong selling of Korean shares continues, and foreign investors sold nearly as much as they in the first half of the month. Since President Moon Jae-in’s party won last week’s local election, the pressures on the conglomerates to sell non-core affiliate holdings, the anticipation of higher corporate tax and an increase in minimum wages has spurred a reversal of sentiment. Japan reported a trade deficit of JPY578 bln in May, which was more than twice what economists expected. The market focused on the 8.1% rise in exports. It is the strongest growth rate in four months. Imports were also stronger than expected, rising 14%, which is more than twice the pace seen in April. The dollar is trading in about a 20 tick range on both sides of JPY110.55. Nearby options that expire today at JPY109.70 ($450 mln) and JPY111.00 ($405 mln) do not look to be in play. The Dow Jones Stoxx 600 also gapped lower today. It is off nearly 2/3 of 1% near midday in London. Most sectors are lower, though telecoms and financials are resisting the push. Last week’s 1% rise snapped three-week decline, but the bounce seen last Thursday, when the ECB confirmed what many in the market had suspected, no rate hike for another year, has been nearly completely retraced. |

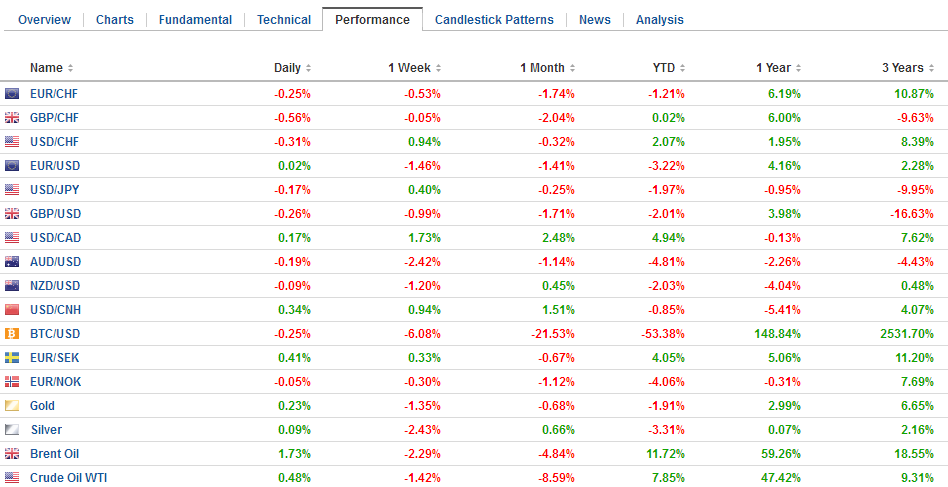

FX Performance, June 18 - Click to enlarge |

Sterling’s pre-weekend bounce fizzled. It has returned to test the $1.3200 area. Brexit concerns are outweighing prospects of a hawkish hold by the Bank of England later this week. Prime Minister May has navigated between the two wings of her party but only by delaying decisive decisions. That road is coming to an end. There is some thought it could come this week, though May has defied the odds several times in the past year or so. A convincing break of $1.3200 would allow sterling to complete the large double top formed in the spring that projects to $1.30-$1.31.

The euro has been confined to a little more than a half-cent within the pre-weekend range. German politic anxiety eclipsed the angst over Italian politics. The pressing issue is immigration, and the Interior Minister Seehofer, who’s CSU faces a tough challenge by the Afd in local elections in a few months. Seehofer, with the support of his CSU parliamentarians, want to turn down refugees who have applied for asylum in another EU country. Merkel, with the support of the CDU, has rejected this immediate course.

A compromise has been struck, giving Merkel the two weeks she sought to strike a deal in Europe. The EU heads of state summit is scheduled for the end of the month (June 28-29), and Merkel needs to come back with a way forward. The problem lies in finding a fix that can be agreed up by the EU that would appease the Seehofer and the CSU. The new governments in Italy and Austria are pushing in the opposite direction.

Meanwhile, the fourth annual ECB forum in Sintra, Portugal kicks off today. It is like the Fed’s Jackson Hole confab, where numerous central bankers and academics present. This year features, Draghi and Lane, Powell, Bullard and Summers, and Australia’s Lowe (mostly Tuesday-Wednesday). The theme is prices and wages. While there is headline risk, the main course of policy seems set after the recent flurry of central bank meetings. We argue that main take away from those meetings was a confirmed that policy divergence is set to continue to the next year, that premium US pays to borrow short-term money will continue to rise relative to the other major economies.

Oil prices are recovering from their earlier steep losses. August Brent fell 3.3% before the weekend amid speculation that oil producers could boost output by a million or more barrels a day. OPEC meets at the end of the week. News today suggests a much smaller increase is anticipated (300k-600k barrel per day), and given that increased output in Saudi Arabia and Russia, the market appears to have absorbed some of that increase.

Recall that OPEC output fell well more than the agreement had called for, and so simply returning to the quota would boost output. That said, it does seem ironic that US President Trump has renewed his concern about higher oil prices when the US sanctions against Iran and Venezuela is part of the story rise in prices. WTI for August delivery was driven through $64 to reach its lowest level in a couple of months before bouncing back. It peaked last Thursday a little above $67 a barrel, near the month’s high.

The economic diaries in the US and Canada are light to start the week. Several officials, including Dudley, Duke, Bostic, Gorman, and Williams speak, which is nearly a third of the Fed. The trajectory of Fed policy is clear. The current monetary setting is still thought to be accommodative. The Fed anticipates it to evolve to become restrictive, that is to say, above the long-term equilibrium rate by the end of next year. Note that the latest Fed stress tests results are due out later this week (June 21).

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,EUR/CHF and USD/CHF,newslettersent