Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

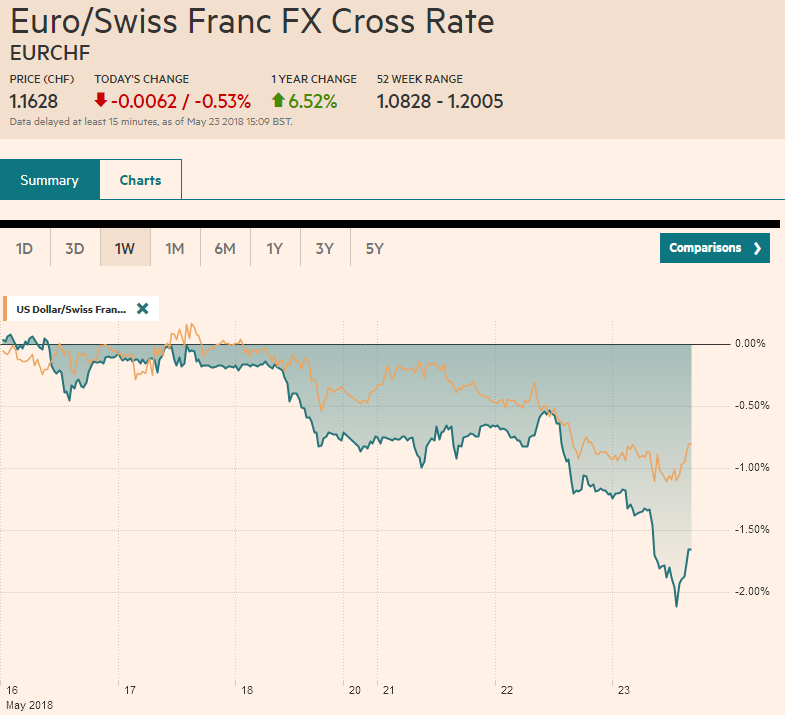

Swiss FrancThe Euro is down by 0.53% to 1.1628 CHF. This is the fifth day in sequence that the Swiss Franc appreciated. Italy political drama is has spurred a significant rally in the Swiss franc. Over the past five days, it has been the strongest of the majors, rising 1.1% against the dollar and 1.8% against the euro. Today, it is the only major currency beside the yen that is gaining ground. Italian assets were given a reprieve yesterday, but the selling resumed today. The 10-year yield is up 11 bp, and the spread over Germany has widened by 16 bp. The Italian stock market is off 1.7%, roughly twice as much as the Dow Jones Stoxx 600. Yesterday, the euro found support near the top of the band of support we identified in the CHF1.1660-CHF1.1680 area. The euro has cut through that area today like a hot knife in butter. It fell to CHF1.1600 before steadying. Old support should now be resistance, with the next technical target near CHF1.1480. |

EUR/CHF and USD/CHF, May 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

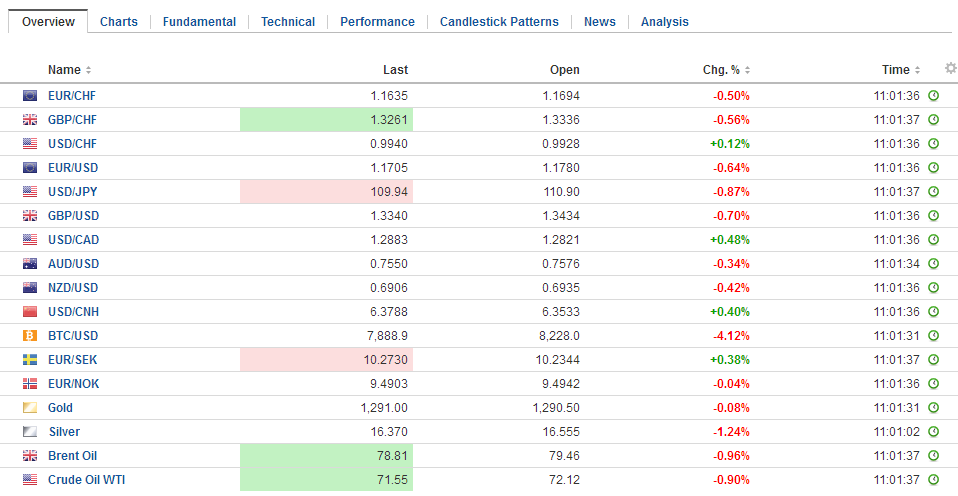

FX RatesThe US dollar has extended its gains against most of the major currencies. Momentum, positioning, and divergence continue to drive it. The euro briefly traded a little below $1.17, an important technical area and has enjoyed a bounce in late morning turnover in Europe. There is a 707 mln euro option struck there that expires today and 1.1 bn euros at $1.1750. The billion-euro option at $1.1785 may not be relevant anymore. The dollar’s pullback that began Monday but ran out of steam early yesterday was snapped up. The positioning in the futures markets, as of a week ago, still points to large speculative (momentum and trend following market segment for the most part), euro exposure. The flash composite PMI for the eurozone confirms that the slowdown seen in Q1 has carried over into Q2. |

FX Daily Rates, May 23 - Click to enlarge |

| On the other hand, the yen has surged. It is up 1% against the dollar. There has been much talk today of Japanese accounts buying yen against the Turkish lira. The Turkish lira has been a favorite high yield story for Japanese households. The Turkish lira is off about 3.3% near midday in Europe, while it had been down 5% earlier. It has fallen 8.5% over the past week and is rivaling the Argentine peso for the biggest decline over the past month (TRY-15%, ARS -16.5%).

The important point about the yen’s strength is that may not be best to understand it as safe-haven demand, but rather the unwinding of a short-yen carry trade. The yen’s use as a financing currency is the key and not the attractiveness of Japan’s asset markets. Stops were trigged as the dollar fell through the JPY110.00 level. It peaked on Monday near JPY111.40. It is slipping through the 20-day moving average for the first time since April 4. The JPY109.70 area that has been tested corresponds to a 61.8% retracement of this month’s gains (from May 4 lows near JPY108.65). Nearby support is seen in a congestion area around JPY109.30. There is a $370 option at JPY109.50 that expires today, and $2 bln struck at JPY110. |

FX Performance, May 23 - Click to enlarge |

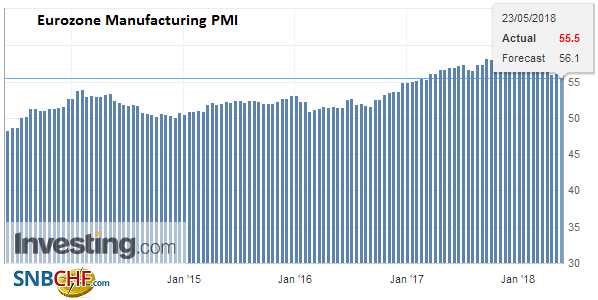

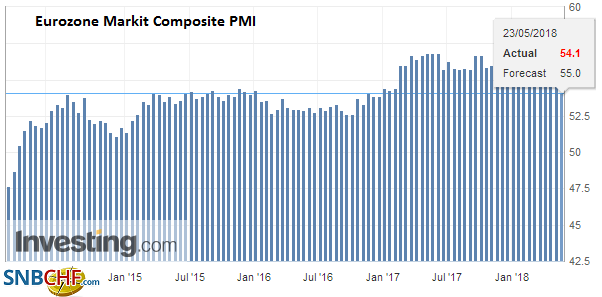

EurozoneThe flash May PMI eurozone report disappointed. It impacts expectations for next month’s ECB meeting. Remember how at the end of last year, many seemed to anticipate that the ECB’s word clues would quickly evolve toward a solid commitment to end the asset purchases. However, the facts, in this case, the economic performance has gotten in the way. Prices and economic activity have gone in the wrong direction. If last time Draghi was “caution tapered by confidence,” the ECB may say that it is its confidence that has been tapered. |

Eurozone Manufacturing PMI (flash), May 2013 - 2018(see more posts on Eurozone Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

| The composite reading fell to 54.1 from 55.1 in April. It is the lowest reading since November 2016. The composite PMI averaged 56.4 in 2017 and 57.0 in Q1. Both services and manufaturing fell. German manufacturing weakened (56.8 from 58.1), though the French PMI rose to (55.1 from 53.8). German services PMI eased to 52.1 from 53.0. The French service PMI fell to 54.3 from 57.4. |

Eurozone Markit Composite PMI (flash), May 2013 - 2018(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

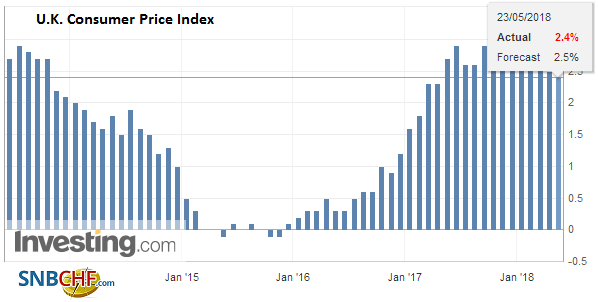

United KingdomIn the UK, price pressures eased. Headline CPI eased to 2.4% from 2.5%, while the CPIH (which includes owner housing costs) slipped to 2.2% from 2.3%. The core rate slowed to 2.1% from 2.3%. The report does nothing to bring forward a BOE rate hike. The implied yield of the December short-sterling futures contract is a couple of basis points lower today. The implied yield of 64 bp is the lowest in four months. Sterling has made a new low for the today, a little below $1.3350. The measuring objective of the large double top we have been monitoring is in the $1.30-$1.31 area, and sterling is wasting little time. Nearby support is seen around $1.3300, which is also where the lower Bollinger Band is found. |

U.K. Consumer Price Index (CPI) YoY, April 2013 - 2018(see more posts on U.K. Consumer Price Index, ) Source: Investing.com - Click to enlarge |

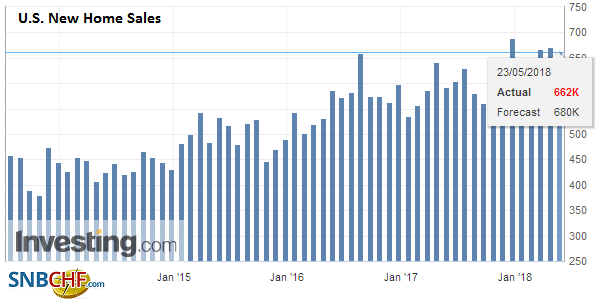

United StatesMarkit reports the flash US PMIs, but the flash readings have not caught on in the as it has in Europe. April new home sales are also released. Sales are expected to have slowed after strong gains in February and March (3.6% and 4.0% respectively). The average monthly gain in 2017 was 1.7%. The highlight of the day may be the FOMC minutes. The market is as confident of a hike next month as it gets. Investors focus on the minutes is on the significance of adding “symmetrical” (twice) to the FOMC statement in terms of the price stability mandate and the yield curve. Don’t expect much closure. The fact that prices increases and wage growth are not accelerating gives the Fed scope to be gradual in raising rates. It is clear from official comments that the Fed itself is divided on the signals from a negative yield curve. |

U.S. New Home Sales, April 2013 - 2018(see more posts on U.S. New Home Sales, ) Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CHF,$EUR,$JPY,EUR/CHF,EUR/CHF and USD/CHF,Eurozone Manufacturing PMI,Eurozone Markit Composite PMI,gbp-chf,newslettersent,U.K. Consumer Price Index,U.S. New Home Sales,USD/CHF