Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

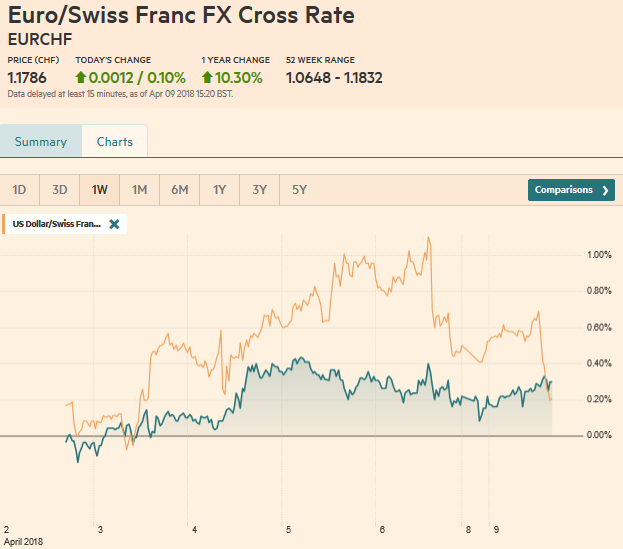

Swiss FrancThe Euro has risen by 0.10% to 1.1786 CHF. |

EUR/CHF and USD/CHF, April 09(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesUS shares slumped before the weekend amid concern that Trump Administration was prepared to escalate the trade tensions with China. However, cooler heads are prevailing, and there is a recognition that the conflict is still in the posturing phase. No sanctions have gone to into effect. As the Economist points out, nearly 100 of the Chinese products the US proposed slap a tariff on are not currently being exported to the US. The US has a 60-day public comment period, and China has not given a date for implementations, but will take its cues from the US. The MSCI Asia Pacific Index rose 0.55%, its biggest gain and highest close in nearly two weeks. All the markets in the region rose. Hong Kong’s Hang Seng’s 1.3% advance led the regions, and after it was the index of H-shares that trade in Hong Kong (China Enterprise Index), which was up 0.9%. The Nikkei gained of 0.5% and posted its highest closed since mid-March. |

FX Daily Rates, April 09 - Click to enlarge |

| Europe is following suit. The Dow Jones Stoxx 600 is up 0.5% near midday and it is seeing its best levels since March 19. Financials, information technology, and industrials are leading the way higher, and only the energy sector is struggling.

Commodities are also rebounding from their worst drop in a few weeks. Oil and industrial metals are higher, with copper at three-month highs. Oil is trading about 0.5% higher after falling around 4.5% last week. While benchmark 10-year yields are mostly 1-2 bp higher, the US dollar is little changed. The yen and Swiss franc are a touch softer, while the euro and sterling are straddling unchanged levels. The Canadian and Australian dollar are slightly weaker, while the Scandis are firm. The only significant option of note that is expiring today is a nearly $850 strike at JPY107.00. |

FX Performance, April 09 - Click to enlarge |

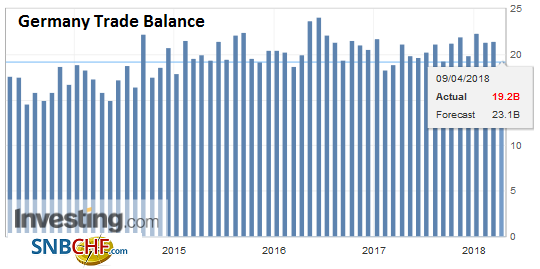

GermanyGerman trade figures disappointed, even though the trade surplus widened to 18.4 bln euros from 17.3 bln in January. Exports and imports both fell. |

Germany Trade Balance, May 2013 - Apr 2018(see more posts on Germany Trade Balance, ) Source: Investing.com - Click to enlarge |

| The 3.2% drop in exports (seasonally adjusted is the biggest decline since August 2015 and means that German exports have not risen since last November, which itself is the only gain since last August. Imports fell 1.3%. The Reuters survey found a median expectation for a 0.3% increase. |

Germany Exports, May 2013 - Apr 2018(see more posts on Germany Exports, ) Source: Investing.com - Click to enlarge |

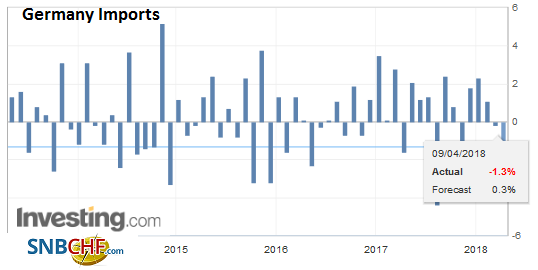

| It was the second consecutive month that imports fell, which is the first back-to-back decline in nearly two years. It follows softening survey data and last week’s poor industrial output report (-1.6% vs. expectations for a small increase). |

Germany Imports, May 2013 - Apr 2018(see more posts on Germany Imports, ) Source: Investing.com - Click to enlarge |

The New Zealand dollar is the strongest of the majors, gaining almost 0.5% to recoup what is lost in the past two sessions. The Kiwi is perceived to be less exposed to the trade-tension story due to is export product mixed (agriculture primarily). The Australian dollar is trading at its lowest level against the New Zealand dollar since last July, falling for its fifth consecutive session. The technical indicators are getting stretched.

Both Japan and German reported February trade figures. Japan’s current account surplus on a seasonally adjusted basis was halved in February to JPY1.024 trillion from JPY2.023 trillion in January. It was a bit smaller than the median expectation in the Bloomberg survey and some of the miss can be attributed to trade itself. The trade surplus was JPY188.7 bln rather than JPY250 bln as expected. It may be worth repeating that the driver of Japan’s current account surplus is not trade but its investment income account, which reported a surplus of JPY1.9 trillion.

Japan also reports capital flows with the current account figures. The MOF’s data shows Japanese investors sold $33.6 bln (JPY3.6 trillion) of US Treasuries in February, the fifth consecutive month of sales. The increase in LIBOR is making hedging dollar-investments more expensive and many attributes the absence of demand to this despite the widening interest rate differentials. Separately, Japanese investors bought nearly JPY304 bln of German bonds and nearly JPY600 bln of French bonds. On the other hand, they sold Australian bonds (~JPY124.4 bln) for the first time since June 2017. Japanese investors were also sellers of UK and Italian bonds.

China reported its March reserves over the weekend. The nearly $9 bln increase was a little less than expected, and appears to be largely a function of the dollar’s decline against other leading reserve currencies. If the increase is in fact due to valuation adjustments, then there may not be change in demand for US Treasuries. Our larger point that a decision by China to boost reserves will nearly by necessity require to boost holdings of US bonds remains valid.

The dollar has risen against the yuan for a fourth consecutive session and Bloomberg runs a story, quoting “people familiar with the matter” claiming that PRC officials are evaluating the potential impact of a gradual depreciation, apparently in the context of trade tensions with the US. This is part of the posturing and showing that a range of measures are at the disposal of Chinese officials. We suspect Chinese officials are loath to change the broad currency and interest rate strategy in response to the trade provocations. That said, after appreciated 7% last year and another 3% this year, the yuan has scope to ease off should the US dollar build on its broader recovery. China’s President Xi addresses the Boao Forum in Asia tomorrow. It is China’s version of Davos.

The economic calendar today in North America is light with no US data or Fed speakers. The US is selling $90 bln of T-bills today, and over the course of the week is raising more than $50 bln in coupon sales. The main economic data of the week is the CPI, which is expected to tick higher. Politics is front and center. Facebook CEO Zuckerberg testifies before Congress on Tuesday and Wednesday. Merkel and Macron are slated to visit the US ostensibly in hopes of getting the administration to relent and make the temporary exemptions from the steel and aluminum tariffs permanent. The Summit for the Americas at the end of the week may see a break through on NAFTA following US concessions on domestic content rules.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?

Tags: #USD,$AUD,$CAD,$CNY,$EUR,$JPY,$TLT,EUR/CHF,Germany Exports,Germany Imports,Germany Trade Balance,newslettersent,NZD,SPY,USD/CHF