Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

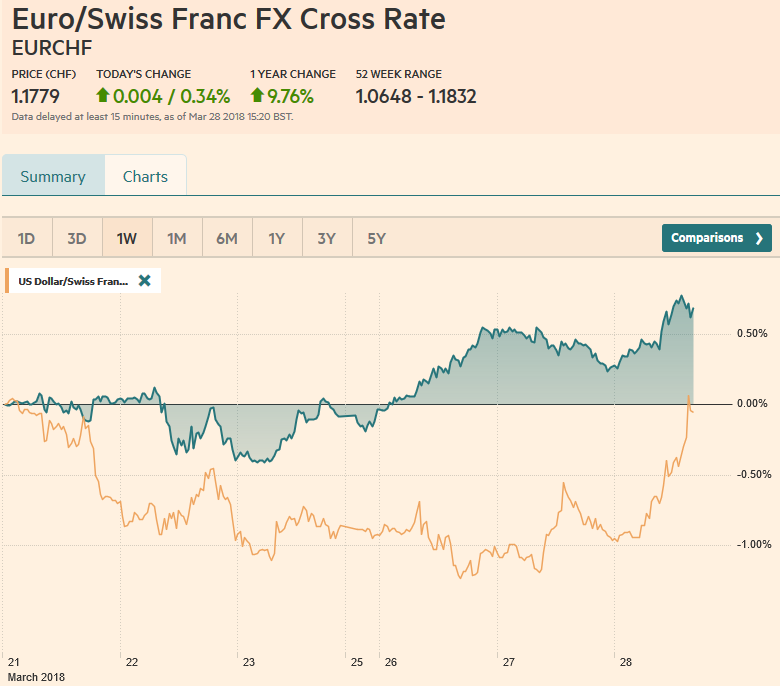

Swiss FrancThe Euro has risen by 0.34% to 1.1779 CHF. |

EUR/CHF and USD/CHF, March 28(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesToday may be the last day of full liquidity until next Tuesday, after the Easter holidays. We identify three developments that are characterizing the end of the month, quarter, and for some countries and companies, the fiscal year. Equity market sell-off, bond market rally, and the continued rise in LIBOR. The sell-off in stocks at the end of last week amid what we think was exaggerated fears of a trade was subsided and stocks rallied on Monday, but US stocks slumped yesterday, which is dragging global markets lower today. Last year’s low volatility seems a distant memory. Since last month’s swoon, the VIX has mostly held above 15 and below 25. It is near 23 now, which is a little more than twice last year’s average. |

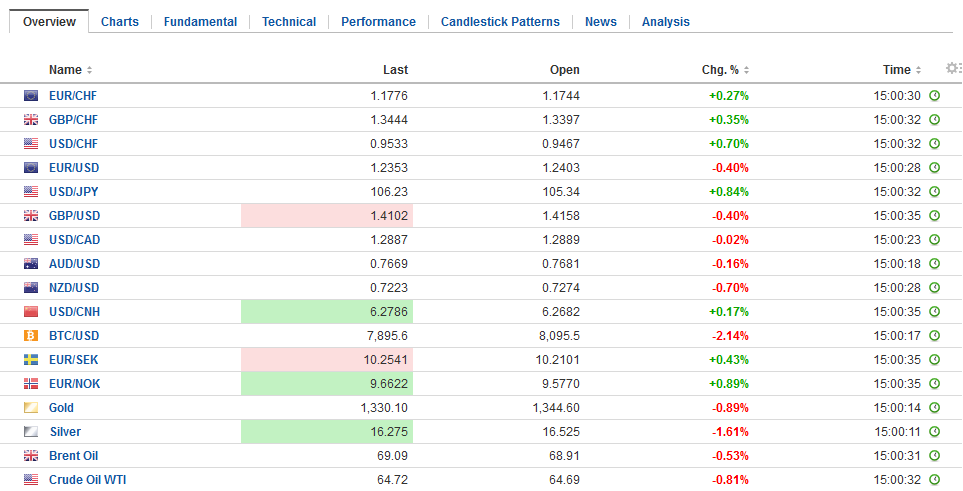

FX Daily Rates, March 28 - Click to enlarge |

| Technology shares, which had led the global rally are in retreat. Privacy issues and problems with self-driving cars may be the proximate triggers. The information technology sector in the US lost nearly 3.5% yesterday, twice the loss of the S&P 500. The MSCI Asia Pacific Index slumped 1.35%, giving back most of the gains of the past two sessions. Information technology and telecoms appeared to be a major weight. It is a similar story in Europe. The Dow Jones Stoxx 600 is off about 1.25% in late morning turnover, while information technology is off 2.7%.

In Japan and Europe, the only sector that is higher on the day are utilities, and that seems to be a function of lower bond yields. That is the second development characterizing the capital markets. The US 10-year yield fell through the recent floor around 2.80% yesterday and is now slipping below 2.75%. It is the lowest yield since February 6, when it briefly spiked to 2.65% amid the equity market meltdown. Australian and New Zealand’s 10-year benchmark yields fell 6-7 bp, while the UK Gilt yield is five basis points lower at 1.37%, which is the lowest since January 24. Core yields in Europe are lower, while peripheral yields are a little firmer. The 10-year German bund yield is slipping below 50 bp for the first time since January 9. |

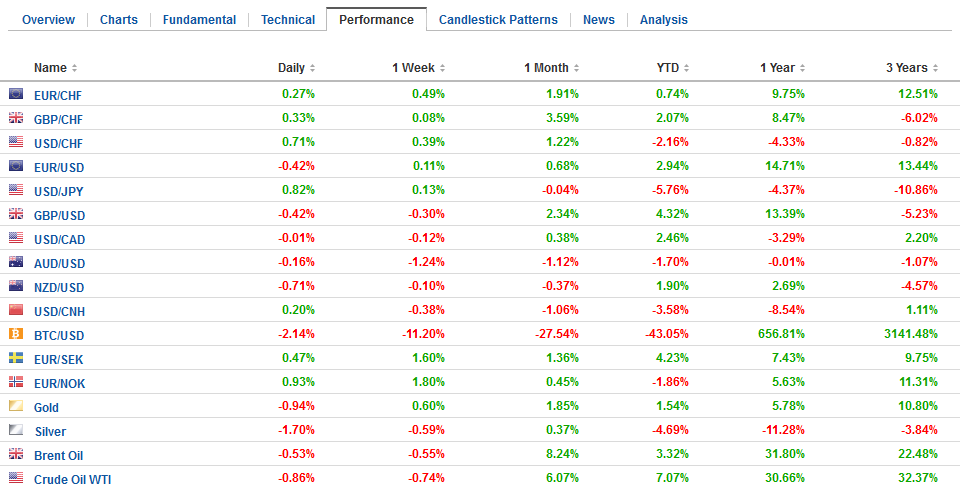

FX Performance, March 28 - Click to enlarge |

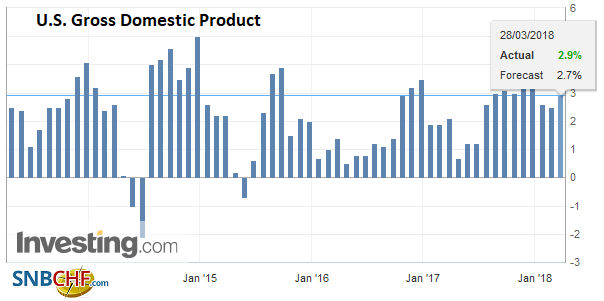

United StatesUS data today includes another revision of Q4 17 GDP. A somewhat stronger inventory build is expected to lift the annualized pace of growth to 2.7% from 2.5%. February advanced goods trade balance and retail/wholesale inventories will be used to estimate Q1 18 GDP, but are unlikely to alter ideas that the curse of a weak Q1 GDP (since the Great Financial Crisis) may were evident this year too despite the tax cuts and spending increases. |

U.S. Gross Domestic Product (GDP) QoQ, Apr 2013 - Mar 2018(see more posts on U.S. Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

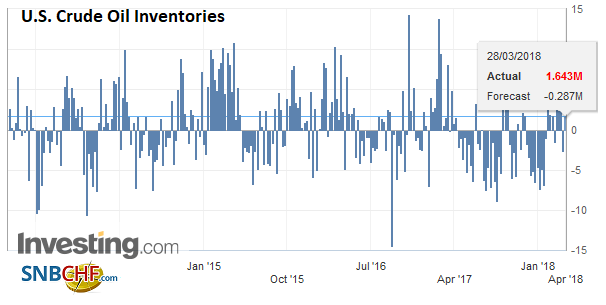

U.S. Crude Oil Inventories, Apr 2013 - Mar 2018(see more posts on U.S. Crude Oil Inventories, ) Source: Investing.com - Click to enlarge |

|

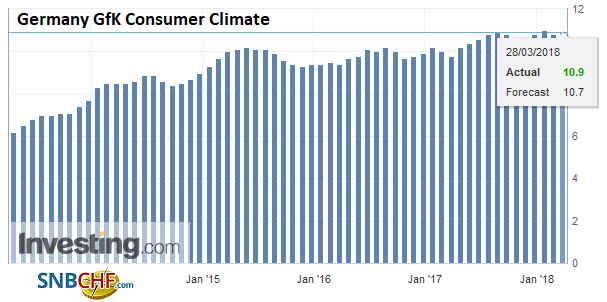

Germany |

Germany GfK Consumer Climate, Apr 2013 - Mar 2018(see more posts on Germany GfK Consumer Climate, ) Source: Investing.com - Click to enlarge |

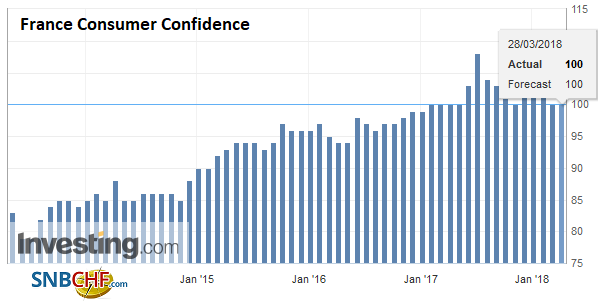

France |

France Consumer Confidence, Apr 2013 - Mar 2018(see more posts on France Consumer Confidence, ) Source: Investing.com - Click to enlarge |

Switzerland |

Switzerland ZEW Expectations, Apr 2013 - Mar 2018(see more posts on Switzerland ZEW Expectations, ) Source: Investing.com - Click to enlarge |

The third characteristic of the capital market is the continued relentless increase in dollar LIBOR. It appears to have fallen in only five sessions here in Q1 18 and ICE three-month LIBOR has not fallen in over a month. Some argue that with US T-bill sales set to slow after the recent deluge, that some pressure may be relieved. Alternatively, if the pressure is also emanating from tax laws that encourage US companies to repatriate (bringing mostly offshore dollars onshore) and the disincentives from lending between parent and subs (for both domestic and foreign-based companies) then the pressure may persist.

At the same time, the dislocation is seeing dramatic but opposite adjustment in the cross-currency basis swaps market. On three-month tenors the premium for dollars against the yen, which reached more than 100 bp on top of LIBOR at the end of 2017, briefly traded at a discount yesterday for the first time since early 2012. It is back to a premium today (~16 bp+ LIBOR). Cross-currency basis swaps for dollars against sterling reached 80 bp on top of LIBOR in the middle of last December. The premium for dollars switched to a discount last week and that discount is now near 17 bp. A discount for dollars has barely existed since 2008. The premium for dollars over euros approached zero yesterday for the first time in nearly four years and now is a little more than six basis points on top of LIBOR.

This conflicting forces, higher USD LIBOR, and lower dollar premium or even a discount in the cross-currency swaps market has far-reaching implications even if the causes may not be fully understood. It raises the cost of hedging, which means it reduces the attractiveness of buying US fixed income–Treasuries as well as corporate bonds–, though this week’s US have gone relatively smoothly. The auctions continue today with $15 bln two-year floater and $29 bln seven-year notes.

The US dollar is mostly firmer today. Sterling is the main exception as it edges higher, though well within yesterday’s broad range. If the consolidative tone persists, sterling may hold below $1.4200. Initial support is seen near $1.4140. The euro is also experiencing an inside day, but seems pinned near yesterday’s lows near $1.2375. The week’s low was set on Monday near $1.2335. The dollar has also been confined to yesterday’s range against the yen. It finished last week below JPY105 and dipped a bit lower at the start of this week, but has remained above that support since Monday’s recovery.

The dollar-bloc currencies are softer. The Australian dollar is slipping lower and near $0.7655, it has made new lows for the year. Some observers are linking the pressure on the Aussie to the LIBOR pressure. The US dollar bounced higher after approaching support near CAD1.28 yesterday. It is now near CAD1.29. We peg resistance in front of CAD1.2930, and a break could see a quick test on CAD1.30.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,France Consumer Confidence,Germany GfK Consumer Climate,Libor,newslettersent,SPY,Switzerland ZEW Expectations,U.S. Crude Oil Inventories,U.S. Gross Domestic Product,USD/CHF