Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

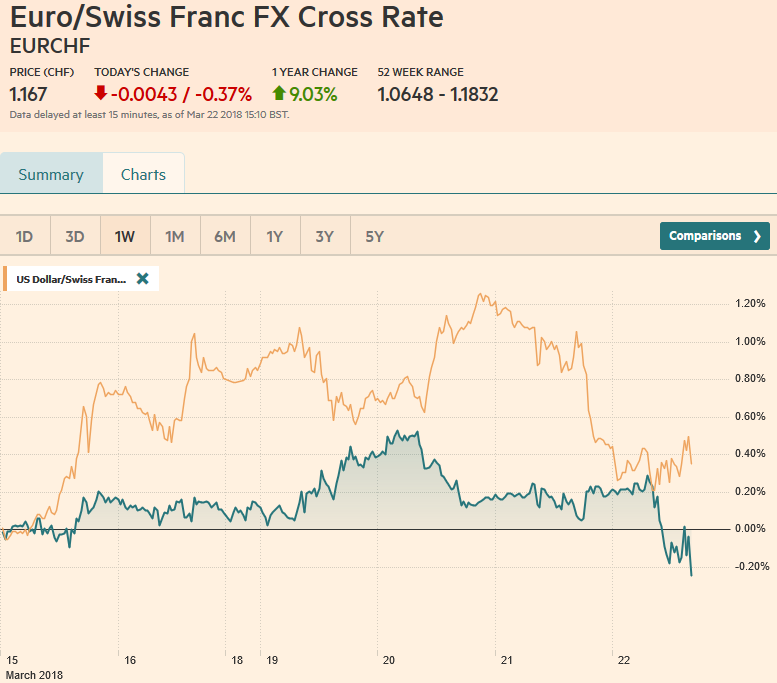

Swiss FrancThe Euro has fallen by 0.37% to 1.167 CHF. |

EUR/CHF and USD/CHF, March 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar has not recovered from the judgment that yesterday’s that Fed was not as hawkish as many had anticipated. There was no indication that officials thought they were behind the curve or prepared to accelerate the pace of hikes. Powell is comfortable with the broad policy framework that has been established but seemed to have little time for the summing up of the individual forecasts (dot plot). There are several reasons why the market is not impressed with the Fed’s hawkishness, but note that from the onset that since at least the past few years, the Fed signaled a more aggressive policy than the market believed likely. As recently as a year ago, Fed officials went on what can be understood as a campaign to convince the market that it would hike rates. |

FX Daily Rates, March 22 - Click to enlarge |

| Contrary to our arguments, many participants expected a clear indication of four hikes this year and the Fed did not deliver that message, though to be sure the door is clearly still open. And four hikes this year is more likely than two Inflation forecasts barely changed, while growth forecasts were ratcheted higher.

The trend or long-term non-inflationary growth remained at 1.8%, which is where the Fed thinks growth will return to when the monetary and fiscal stimulus runs their course. We also found a general recognition that the US is showing increasing signs of late-cycle behavior. Hitting an economy in the advanced stages of a business cycle with a large dose of fiscal stimulus has few precedents. |

FX Performance, March 22 - Click to enlarge |

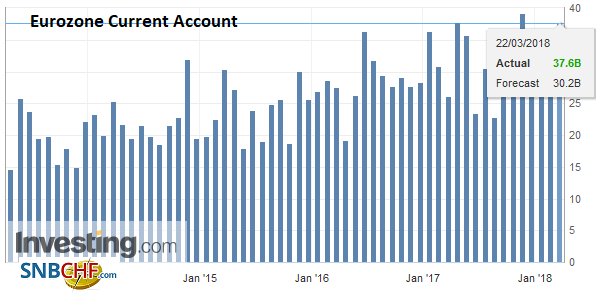

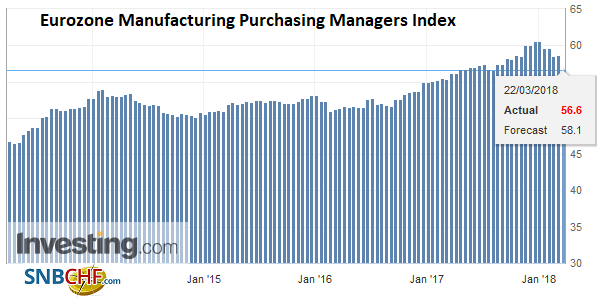

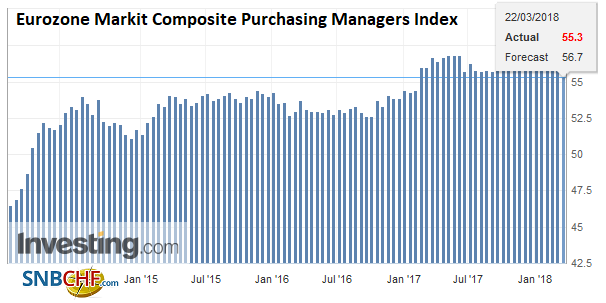

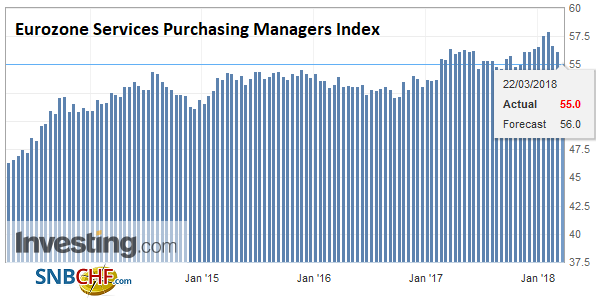

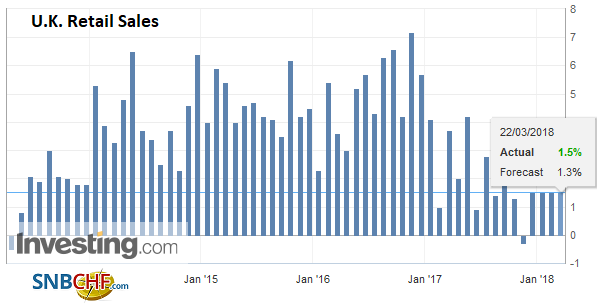

EurozoneThe eurozone sees the flash PMI readings. The surveys and some real sector data point to slowing of the region’s economic momentum, and this includes Germany. This is expected to have carried into today’s reports. The UK sees February retail sales before the BOE meeting. Despite what is expected to be increased consumption compared with January, the year-over-year rate may slow further. The easing of price pressures and firm wages could help fuel consumption in Q2. |

Eurozone Current Account, Apr 2013 - Mar 2018(see more posts on Eurozone Current Account, ) Source: Investing.com - Click to enlarge |

Eurozone Manufacturing Purchasing Managers Index (PMI), Apr 2013 - Mar 2018(see more posts on Eurozone Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

|

Eurozone Markit Composite Purchasing Managers Index (PMI), Apr 2013 - Mar 2018(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

|

Eurozone Services Purchasing Managers Index (PMI), Apr 2013 - Mar 2018(see more posts on Eurozone Services PMI, ) Source: Investing.com - Click to enlarge |

|

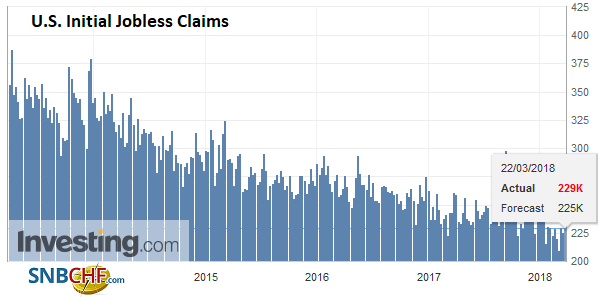

United StatesWhile the US reports some high-frequency data (weekly jobless claims, LEI, flash PMI), investors’ focus is elsewhere. First, with the Fed’s hike behind us, Q1 data has lost some of its interest. The Fed is looking through the softness of consumption and investment. More important will be Q2 data and the Fed is understood to be out of the picture until June. Second, trade moves back to center stage as the US will reportedly announce the actions in retaliation for what it sees as intellectual property rights violations that have been discussed since the Clinton Administration. Tariffs, as well as curbs on investment, and possible action on (student) visa as well have been mentioned. |

U.S. Initial Jobless Claims, Mar 2013 - 2018(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

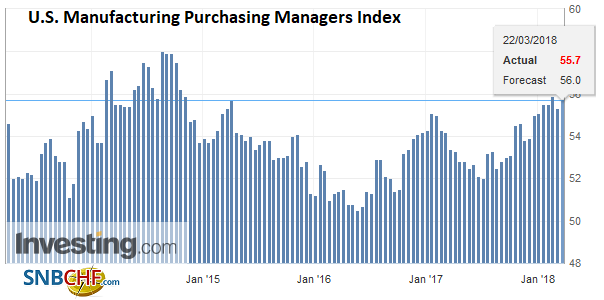

U.S. Manufacturing Purchasing Managers Index (PMI), Apr 2013 - Mar 2018(see more posts on U.S. Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

|

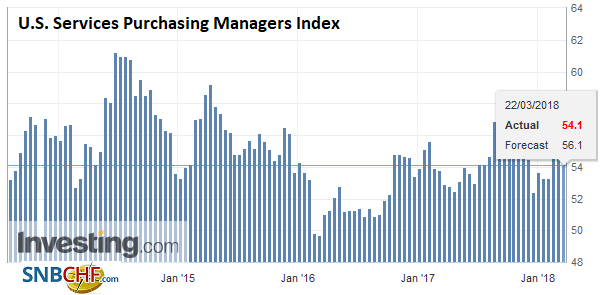

U.S. Services Purchasing Managers Index (PMI), Apr 2013 - Mar 2018(see more posts on U.S. Services PMI, ) Source: Investing.com - Click to enlarge |

|

United Kingdom |

U.K. Retail Sales YoY, Apr 2013 - Mar 2018(see more posts on U.K. Retail Sales, ) Source: Investing.com - Click to enlarge |

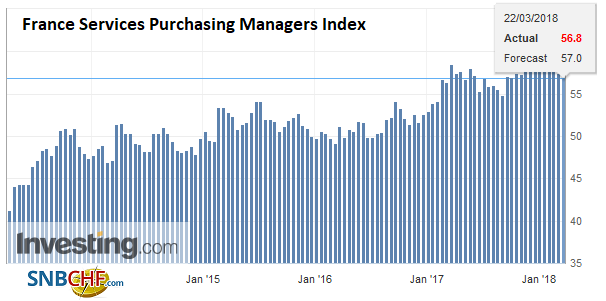

France |

France Services Purchasing Managers Index (PMI), Apr 2013 - Mar 2018(see more posts on France Services PMI, ) Source: Investing.com - Click to enlarge |

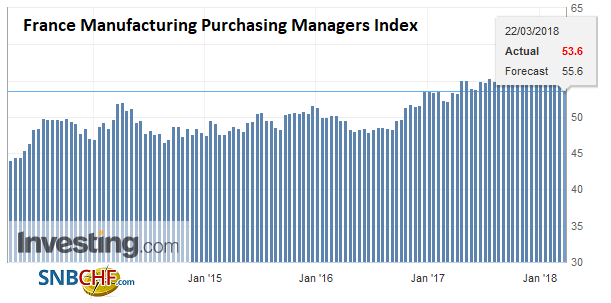

France Manufacturing Purchasing Managers Index (PMI), Apr 2013 - Mar 2018(see more posts on France Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

|

Japan |

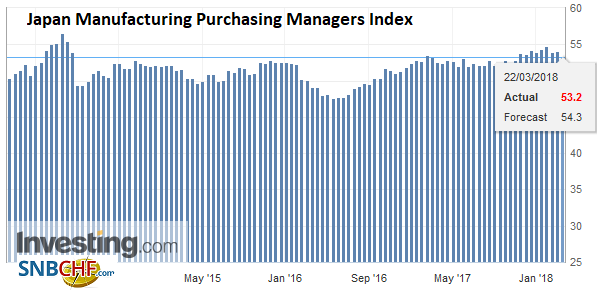

Japan Manufacturing Purchasing Managers Index (PMI), Mar 2013 - 2018(see more posts on Japan Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

With businesses having more spare capacity than past cycles and experiencing low rates for a long-term, tax cuts may not be the boon to investment that many expect. Similarly, with debt and credit tensions rising, American households may not simply consume their tax cuts. Reducing debt and boosting savings could deflect some of the post-tax income away from consumption.

Powell seemed uncomfortable when asked about the yield curve. While the literature may be mixed, many economists and investors put much significance on inverted coupon curve signaling an economic contraction. Between the rate hikes, the shrinking of the balance sheet, the elevated LIBOR, the risk of a policy mistake seems elevated.

The Hong Kong Monetary Authority signaled a 25 bp increase to 2%. Hong Kong is awash with liquidity and the 25 bp rate hike after the December Fed hike did not prompt the large banks to raise lending rates. So far they prime rates remain steady. The liquidity in the domestic market coupled with the increase in LIBOR, which is resulting in a growing divergence with HIBOR, has kept the Hong Kong dollar trading heavily relative to peg. Although there is some speculation that the peg may be abandoned, we think it is arguably more a political question than an economic question. Given the importance of stability, we see no case for abandoning the peg and expect the HKMA to defend the band.

There is not only continuity despite the change at the Fed’s helm, but the same can be said of the PBOC. The new head, previously a deputy Yi Gang, followed his predecessor’s practice. Following the Fed rate hike, the PBOC increased the rate on its open market operations (seven-day reverse repo) by five basis points (2.55%), just like it did after last December’s hike.

The Reserve Bank of New Zealand met, and as widely expected stood pat. Moreover, it signaled not intention to hike rates anytime soon. The Bank of England meets shortly, and while it too will likely keep rates steady, Carney is unlikely to say anything to dissuade the market of its inclination that rates will be hiked in May. One or two dissents from the majority decision to wait a bit longer before hiking will likely help drive home the message of a hawkish hold.

The Australian dollar is the only one of the majors that can’t quite get a leg up on the greenback today. Yesterday’s recovery off the fresh lows for the year was impressive and the consolidation today should not be surprising. However, it is being linked to jobs report that showed the unemployment rate unexpected ticking up. We do not read much into it. The participation rate rose and the increase in full-time jobs more than offset the decline in January.

The MSCI Asia Pacific Index snapped a four-day decline with today’s 0.3% increase. The gains, however, were narrowly based on Japan, Korea, Malaysia and Thailand.

We suggest that a trade war requires a substantial second or retaliatory strike. We think China will take a page from the European playbook and make some modest, largely symbolic protest, with the bulk of the strategy aimed at strengthening the very multilateral trading system that the US seems to be defecting from by appealing to the World Trade Organization.

Also, China seems well prepared to make small concessions to the US that it was likely prepared to make at any opportunity. Moreover, there are actions that serve China’s government’s purposes as well, including reducing some tariff schedules, and protecting intellectual property rights better as it gets its own and growing patent portfolio.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: $AUD,$EUR,$JPY,China,EUR/CHF,Eurozone Current Account,Eurozone Manufacturing PMI,Eurozone Markit Composite PMI,Eurozone Services PMI,France Manufacturing PMI,France Services PMI,HKMA,Japan Manufacturing PMI,newslettersent,U.K. Retail Sales,U.S. Initial Jobless Claims,U.S. Manufacturing PMI,U.S. Services PMI,USD/CHF