Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

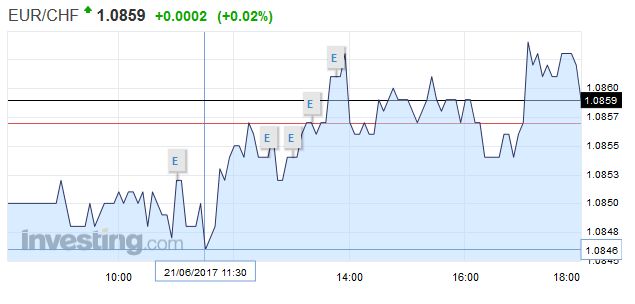

Swiss FrancThe euro is up by 0.02% to 1.0859 CHF. |

EUR/CHF - Euro Swiss Franc, June 21(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe US dollar is narrowly mixed against the major currencies. The drop in oil prices (3.3% this week) is seen as one of the factors that may be underpinning the appetite for fixed income, and this, in turn, is lifting the yen. The greenback had approached JPY112 yesterday, but with the drop in oil prices and yields has seen it retreat toward JPY111.00. Sterling has been unable to recover from BOE Governor Carney’s push back against the MPC hawks. Uncertainty spurred by Brexit, and the squeeze on wages, a key fuel for consumption and growth offsets in what Carney suggested was the transitory effect of the past decline in sterling. Sterling fell below the 100-day moving average yesterday (~$1.2630) for the first time since mid-April. The 200-day moving average is seen closer to $1.2555. The 38.2% of this year’s rally (~$1.2640) had offered support until yesterday and now may serve as resistance. The 50% retracement is seen near $1.2520. The euro is consolidating yesterday’s losses that saw it approach the late May low near $1.1110. This is seen as the lower end of the $1.11-$1.13 range that has confined the single currency for four weeks. With a light new stream, the large options that expire today may be important. At $1.1155, there is nearly 750 mln euro that roll-off, and another 570 mln with a $1.1180 strike. Almost a yard of euros is struck at $1.12. Separately, we note a JPY111.30 strike for a little more than $800 mln also is on the block today. The Australian and Canadian dollars are the weakest of the major currencies today. The RBNZ meeting may deflect the selling pressure against the Kiwi. The Aussie had been in a clear range in recent days (~$0.7570-$0.7635). The range was extended to the downside. Though new buying emerged near $0.7550, it has made little headway. A move above $0.7580 might suggest a false break. |

FX Daily Rates, June 21 - Click to enlarge |

| The Canadian dollar has been chopping broadly sideways after posting smart gains on the back of last week’s hawkish BoC comments. The US dollar has been largely in a CAD1.32-CAD1.33 range. It is testing the upper side of that range today, which also corresponds to a 38.2% retracement of the greenback’s decline from the June 9 higher near CAD1.3540. The 50% retracment is found near CAD!.3350. Tomorrow Canada reports retail sales and then CPI before the weekend. Any disappointment could see the market re-think the likelihood of a hike as early as the July 12 central bank meeting.

Bloomberg is overplayed the news by asserting that it advances President Xi ambition of making the yuan a global currency. Some estimates suggest the 0.5% allocation to A-shares is worth $8-$10 bln inflows. Given the size of the currency market, the average daily yuan flow, it is the minor sum, which also is unlikely to have much impact on the prices of local shares. At the end of the month, the IMF’s COFER report will show the currency allocation of reserves as of the end of Q1. Recall that at the end of 2016, the IMF estimates that the dollar value of the yuan in reserves was a little less than $85 bln. From another perspective, China is already a global currency. It is in the SDR. The yuan’s turnover means that it has surpassed the Mexican peso as the most actively traded emerging market currency.Separately, MSCI postponed decisions on whether to lift Argentina from Frontier to the Emerging Market Index. It appears that the decision will be reconsidered next year. MSCI also postponed a decision for a stand alone Nigeria equity index until November Saudi Arabia was put on a watch list for potential inclusion in the Emerging Market Index. MSCI noted that Saudi Arabia had taken significant strides to improve accessibility. |

FX Performance, June 21 - Click to enlarge |

United StatesAPI reported that US oil stocks were drawn down by 2.72 mln barrels in the weekend ending June 16. This offset the prior week’s unexpected build. The price of oil price to seven-month lows before the industry report amid news that Libyan output reaches a four-year high. The official government estimate will be reported today.

|

U.S. Crude Oil Inventories, May 2017(see more posts on U.S. Crude Oil Inventories, ) Source: Investing.com - Click to enlarge |

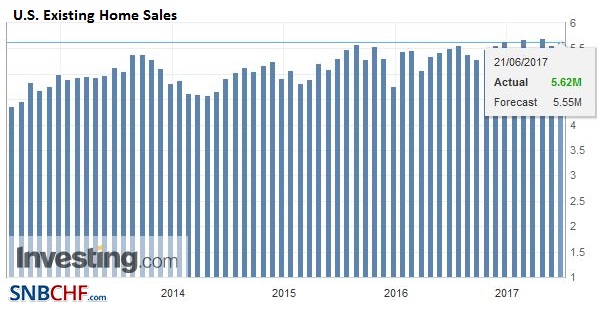

| The US session features existing home sales. A small decline is expected. It would be the first back-to-back decline since Oct-Nov 2015. Since October 2106, the monthly report has alternated between increases and declines. No Fed officials are on tap, though three more speak before the weekend. Lastly, we note that the Republicans won the two special elections to place Congressmen who have joined Trump’s cabinet. Although the Democrat efforts made for tight contests, and despite the low support rating for the President, the outcome is likely to bolster the legislative agenda. |

U.S. Existing Home Sales, May 2017(see more posts on U.S. Existing Home Sales, ) Source: Investing.com - Click to enlarge |

There are three other supply-side stories that weigh on sentiment. First, the increase in gasoline inventories (highest since mid-March) at a time that seasonal factors point to low levels warns that part of the surplus oil is being moved upstream.

Second, while the rig count has risen for 22 weeks, a record–pace ramp up, reports suggest that last month 125 more wells were drilled than opened. These wells (DUCs, as in drilled but uncompleted) would generate nearly 100k bpd. All told, there are nearly 6000 DUCs, the most in three years.

Third, and under-appreciated, technological progress continues to improve efficiencies, and drive costs down. Some fields in the Permian Basin reportedly can produce a barrel of shale oil for $35. Of course, this is not the US average production price, but it illustrates what is possible and the challenge OPEC faces trying to create an artificial scarcity. At the end of the day, the competitive pressures that drive technological advances may be a more powerful force that collusion among primarily Middle East oil producers who often have conflicting national interests.

United Kingdom

Prime Minister May’s Queen Speech, which opens up a two-year parliamentary session followed the question time. It is rather aggressive to open the parliamentary session without securing the agreement with the DUP, even support as a minority government. The UK faces several economic and social challenges, but the self-chosen exit from the EU may prove so distracting and yet demanding of resources and attention, that little else gets done.

China

It took a few years, but MSCI finally agreed that China had taken sufficient measures to begin including the mainland’s A-shares its Emerging Market equity index. It will take place in two steps next year, in May and August. In weighting terms, the A-shares will account for 0.5% of the Emerging Market equity index. MSCI met China halfway, so to speak. China has made several reforms to meet MSCI requirement. MSCI scaled back its proposal and won support by some of the largest asset managers in the world.

It is an important first step. Over time, this allocation islikely to increase, though at some point it could come at the expense of the other Chinese shares are already included, like H-shares and ADRs. At the sametime, the impact should not be exaggerated. The allocation is small enough; some fund managers may choose to ignore it for the time being, of buying a proxy in the H-shares, which have outperformed the A-shares by more than 10 percentage points so far this year.

Chinese shares did edge higher, with the Shanghai Composite gaining 0.5% and the Shenzhen Composite rising 0.4%. Hong Kong’s Hang Seng and an index of China’s H-shares were lower. It is not clear how much of the gain in China’s shares can be attributed to the MSCI decision. The PBOC is continuing to inject liquidity into the banking system, apparently to relieve quarter end pressures and that Shanghai Interbank Offered Rate eased for the fifth day. Nigerian shares are a little heavy (-0.2%). Saudi Arabia’s Tadawul index rallied 4%, recouping this year’s losses. It is also difficult to ascertain the impact of the MSCI decision and news of that Deputy Crown Prince Mohammed bid Salman (MBS) has been officially named as heir to the throne.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,FX Daily,newslettersent,OIL,U.S. Crude Oil Inventories,U.S. Existing Home Sales