Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

EUR/CHF - Euro Swiss Franc, December 06(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe foreign exchange market is quiet. Ranges are narrow, with the US dollar mostly consolidating against the major currencies. Given the push lower yesterday, the shallowness of its recovery warns of the greenback’s downside correction after strong gains last month may not be complete. The news stream lends itself to consolidation. The immediate angst over Italy has calmed. Many new reports insist on calling the defeat of the referendum as a victory for anti-establishment forces. We demur, and note that the opposition, nearly 60%, was only partly explained by the populist-nationalist forces, but the opposition to it was obviously widespread including in area in which the 5-Star Movement is not particularly strong. |

FX Performance, December 06 2016 Movers and Shakers Source: Dukascopy - Click to enlarge |

| The Reserve Bank of Australia left policy on hold, with the cash rate at 1.5%. This was widely expected. While the economy has slowed, the headwinds may be abating soon, and the central bank remains concerned that lower rates will fuel household borrowing and real estate investing. First thing tomorrow in Australian, Q3 GDP will be reported. It is expected to contract by 0.1% and bring the year-over-year rate to 2.2% from 3.3%. However, the mining adjustment appears to be in the late stages, and the rise of metal prices and the apparent stabilization of China are positives. |

FX Daily Rates, December 06 - Click to enlarge |

| The Australian dollar rally ran out of steam yesterday near $0.7500, the same place it was stopped last week. A break of $0.7420 now would undermine the near-term technical outlook. The Canadian dollar was little changed after a wide range of prices yesterday. Canada reports the October merchandise trade balance (expected to be less than half of September’s C$4.1 bln shortfall) and the Ivey PMI (where a small gain from October’s 59.7 reading is expected).

The euro has been confined to about 15 ticks on either side of $1.0750. For the first time since November 10, the five-day average is moving above the 20-day average. The short-term market still seems short euros, and there may be some pressure to adjust ahead of the ECB meeting on ideas that it has already large been discounted that it will extend its asset purchases and tweak other programs for technical and operational purposes. Sterling has extended yesterday’s gains to $1.2775. It is the fourth session of higher highs to reach two-month highs. Initial support now is pegged near $1.2720. The dollar stalled in front of the recent high against the yen near JPY114.80. If US rates are the driver, then it is noteworthy that US yields are coming in softer, and Japanese yields firmed. Initial support is near JPY113.50 and then JPY113.00. |

FX Performance, December 06 - Click to enlarge |

EurozoneMoreover, as it turns out, Renzi will stay on until at least the passage of the 2017 budget, which could happen toward the end of the week. It is possible that after the Italian President looks around for the best person to head up the government, Renzi is it. One indication that this will not happen is if Renzi also resigns as head of the PD. At the same time, it looks like investors are coming around to a less apocalyptic understanding of Italian developments. To wit: bank shares have recouped yesterday’s loss and are up about 2.6% near midday in Milan after falling 2.2% yesterday. Italian sovereign bond has also recovered. Yesterday the 10-day yield rose eight bp. Today it is off six bp. What this means is that over the past week, the benchmark 10-year yield is down almost three bp, while Spain’s is off two bp and Germany is up 12 bp. A similar story is evident in the equity market. Italian equities underperformed yesterday but are leading the way higher today with a 1.4% gain. Over the past week, the FTSE-MIB is up 4.4%, the most among not just major European markets but the G7 as well by a couple of magnitudes. Monte Paschi successfully swapped about 20% of its subordinated notes for equity. The next step is to secure new capital by anchor investors, like Qatar. After that is the challenge of raising capital by issuing more stock. There is some risk that even if it can do this, which is not sure thing (which is also why there is still talk of precautionary state aid), it may satiate the market for this type of risk asset even though other large Italian banks are also looking to raise capital. There is also some talk that the bank may move away from its non-performing loan disposal, which might not sit well with potential investors. |

Eurozone Gross Domestic Product (GDP) YoY, November 2016(see more posts on Eurozone Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

GermanyGerman news offered a pleasant surprise. Factory orders surged 4.9% in October. It is the largest increase in more than two years. The market was expected a little more than one-tenth of the actual increase. Also, the September decline was halved to -0.3% from -0.6%. The gains were broad based and lent support to the Bundesbank’s optimism that growth will accelerate substantially in Q4. Orders for investment goods rose 7.2%. Export orders rose 3.9%, and this likely means that business investment increased in some of Germany’s largest trading partners (US? China?). Domestic orders rose 6.3%. With consumer goods up to a modest 0.5%, it may not auger well for strong consumption-led growth. Consistent with the theme, Markit reported that the retail PMI fell to 49.6 in November from 51.0 in October. It is the third consecutive decline and the lowest reading since January. |

Germany Factory Orders, November 2016(see more posts on Germany Factory Orders, ) Source: destatis.de - Click to enlarge |

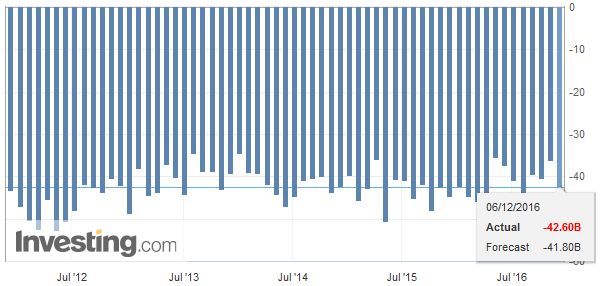

United StatesThe US economic schedule picks up today. The October trade balance and factory orders (including durable goods) will inform forecasts for Q4 GDP, for which tracking models are converging a little below 3%. Also, the upwardly revised Q3 GDP points to upward revisions in US productivity and downside pressure on unit labor costs. That said, the data are unlikely to change investor views for next week’s FOMC meeting. |

U.S. Trade Balance, November 2016(see more posts on U.S. Trade Balance, ) Source: Investing.com - Click to enlarge |

Switzerland |

Switzerland Consumer Price Index, November 2016(see more posts on Switzerland Consumer Price Index, ) Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,$JPY,EUR/CHF,Eurozone Gross Domestic Product,FX Daily,Germany Factory Orders,Italy,newslettersent,U.S. Trade Balance