Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Jonathan Watson

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitter

Swiss Franc |

EUR/CHF - Euro Swiss Franc, November 23(see more posts on EUR/CHF, ) |

|

The GBPCHF rate has slipped a little in early morning trading today as investors await the UK budget due today. Amongst the usual leaks and rumours there appears likely to be a budget which will not be overly generous as some expect but will seek to keep the UK economy on a fairly stable course. UK Borrowing and Debt is still a huge issue for financial markets and Hammond will I am sure wish to retain some of the financial credibility that has put the Tories back into Government. One of the members of the Swiss National Bank Governing Board members Fritz Zurbrugg is giving a speech tomorrow but by and large I cannot see any big changes on the horizon from the SNB themselves. With negative interest rates being used to deter investment and keep the economy growing it will be interesting to see how the Industrial Production data fares, also released tomorrow. I expect GBPCHF rates to remain in a fairly tight range between 1.23 and 1.26 as we approach December but there does remain the potential for some outside of expectation shocks. Namely I would not be surprised to see sudden GBP weakness or strength based on the outcome of the latest Supreme court decision in the UK which is linked to the strength and weakness of sterling. |

GBP/CHF - British Pound Swiss Franc, November 23(see more posts on GBP/CHF, ) . - Click to enlarge |

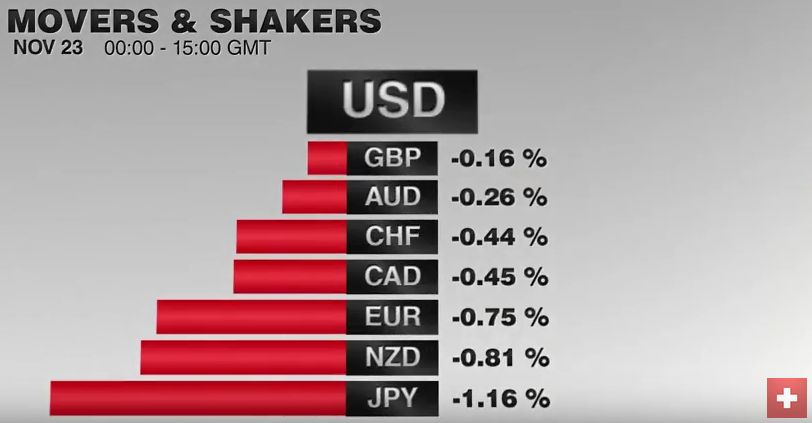

FX RatesThe US dollar is trading inside yesterday’s ranges against the euro and yen. The dollar’s tone matches the consolidation in the debt market ahead of today’s slew of US data and tomorrow’s holiday. Tokyo markets were on holiday. Sterling is trading heavily. Its half-cent loss (0.4%) is the biggest decline among the majors today. In the larger picture, it is within the range set on Monday. Hammond’s Autumn Statement appears to have been largely leaked. |

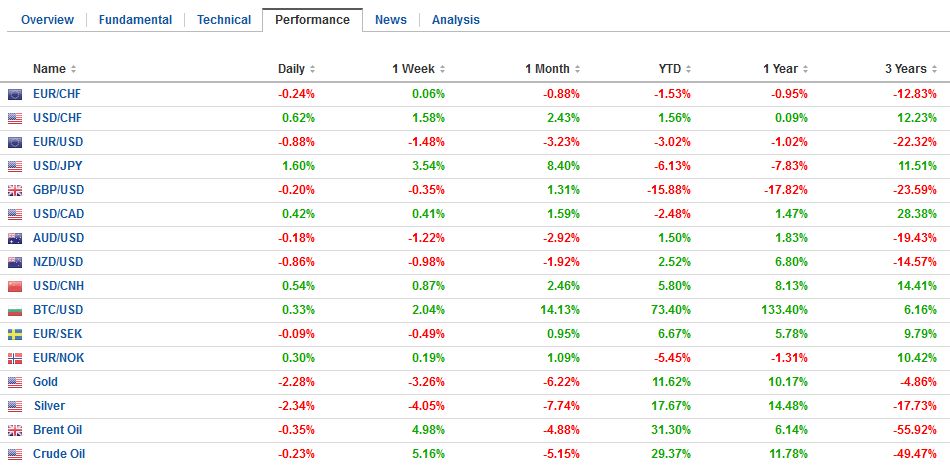

FX Performance, November 23 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| Small spending increases for infrastructure and help for home buyers are expected to be featured. The market appears to feel comfortable with the projected Gilt and bill issuance. The projections for slower economic activity is translated into a larger deficit, and these cyclical expenditures seem to absorb the appetite for May’s wing of the Tory Party. That said, monetary policy, with a cheap lending facility, base rate cut, resumption of QE, and sterling’s decline have already been deployed to support an economy, which continues to perform well. |

FX Daily Rates, November 23 (GMT 16:00) . - Click to enlarge |

| After the major US indices set new record highs, Asian markets also advanced. The MSCI Asia-Pacific Index, excluding Japan (holiday), gained 0.6% in its second days of gains. The MSCI Emerging Market equity index is posting small gains for the third session. With today’s gains, it has moved higher in six of the past seven sessions. European investors did not get the memo, and after posting early gains, European equities have gone south. Minor losses are being recorded in late-morning activity, with the financials, information technology and utilities dragging the market lower. |

FX Performance, November 23 . - Click to enlarge |

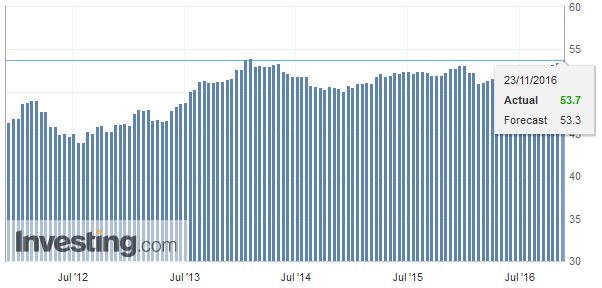

EurozoneThe second development is the flash euro area PMI. The details were favorable. The are mixed economic signals. While the PMI suggests the region will end the year with trend growth or better, officials will still be concerned about the uneven nature of the economic growth and its fragility. Moreover, inflation is seeing little traction. |

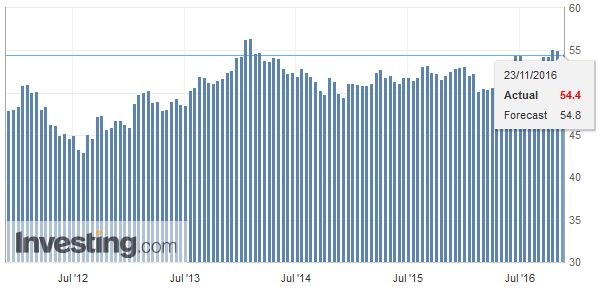

Eurozone Manufacturing PMI, November 2016(see more posts on Eurozone Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

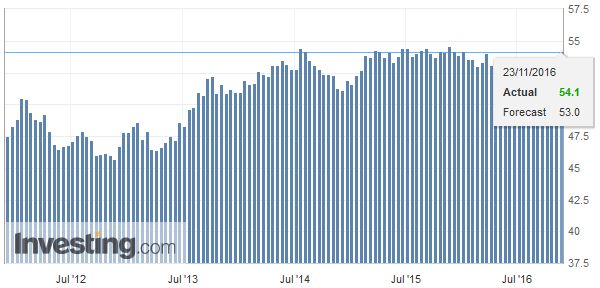

| The composite November reading rose to 54.1 from 53.3. It is a new high for the year. |

Eurozone Markit Composite PMI, November 2016(see more posts on Eurozone Markit Composite PMI, ) . Source: Investing.com - Click to enlarge |

|

Employment, prices, and new orders all rose. The ECB meets on December 8, a few days after the Italian referendum. ItalyThere have been two news developments. The first is an update on Italy’s Renzi’s intentions. The referendum at the end of next week looks likely to fail. There will no more polls. Renzi complicated the situation by threatening to resign if the referendum lost. Although he had backed away from this, his frustration appeared to grow, and he returned to talking about his future. His trump card was to call for early elections. The parliament term ends in 2018. The problem is that electoral reform for the lower house has already been approved, but the referendum could reject reform of the Senate, leaving different electoral laws for the two Chambers. The Deputy Secretary of Renzi’s PD has suggested the election may be brought forward to next summer, though it is not immediately clear if Renzi would stay on until then. Italian assets are mixed. Equities are heavy, and the FTSE Milan is entering the downside gap created by yesterday’s higher opening. Italian bank shares are off almost 3% to the index’s lowest level since early October. It is the seventh decline in the past eight sessions. Italy’s 10-year bond yield has risen six basis points, the most in Europe today, while the two-year yield has risen a couple of basis points, it is up less than Spain’s comparable yield. |

Eurozone Services PMI, November 2016(see more posts on Eurozone Services PMI, ) . Source: Investing.com - Click to enlarge |

GermanyNote that the German two-year yield slipped to new record lows yesterday. This is important. The dollar is not only being underpinned by the changing policy expectations in the US, but the widening of the interest rate differential is a result of both sides moving, diverging. Consider over the past week, the US two-year yield has risen eight basis points, while the Germany two-year yield fell nine basis points. |

Germany Manufacturing PMI, November 2016(see more posts on Germany Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

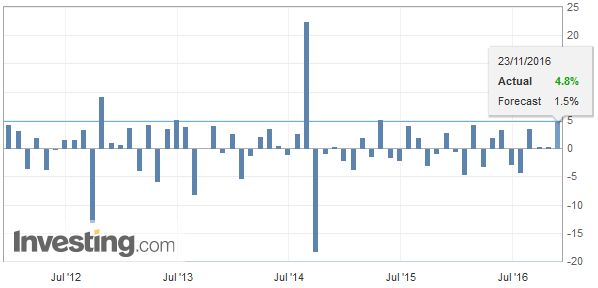

United StatesThere are several US economic reports: durable goods orders, weekly jobless claims, new home sales, Markit flash manufacturing PMI, and the University of Michigan consumer confidence (and inflation expectations survey). Barring significant surprises, the data is unlikely to have more than a headline effect. The market is convinced that the Fed is poised to hike rates in the middle of next month. Expectations for Q4 GDP have also been lifted lately. The NY Fed’s GDP tracker rose 0.8 percentage points over the past week or so to sit at 2.4%. The Atlanta Fed who will update its model today was at 3.6% last week. |

U.S. Durable Goods Orders MoM, October 2016(see more posts on U.S. Durable Goods Orders, ) . Source: Investing.com - Click to enlarge |

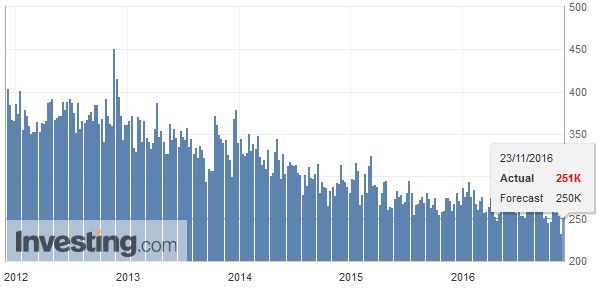

U.S. Initial Jobless Claims |

U.S. Initial Jobless Claims, October 2016(see more posts on U.S. Initial Jobless Claims, ) . Source: Investing.com - Click to enlarge |

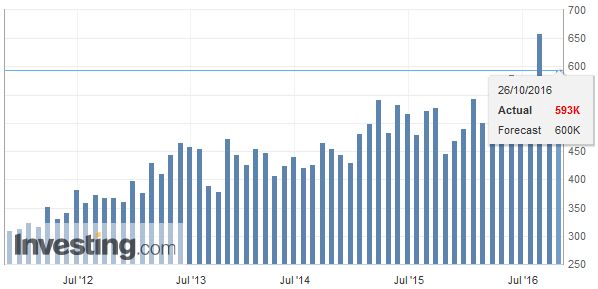

U.S. New Home Sales |

U.S. New Home Sales, October 2016(see more posts on U.S. New Home Sales, ) . Source: Investing.com - Click to enlarge |

A common retort to our bullish dollar outlook is that the market has “priced it in,” usually referring to either a Fed hike or more stimulus fiscal policy. While next month’s rate hike does, in fact, seem to be discounted, investors remain less sanguine about next year. The December 2017 Fed funds futures contract implies a yield of 97 bp. That would seem to imply that one hike next year is fully discounted (that would give a mid-point of 87.5 bp. The market appears to have gone a long way toward pricing in a second hike but is not fully there.

The FOMC minutes from the meeting earlier this month will be released later this afternoon.Participation will lighten up by then, and the minutes are unlikely to tell investors anything that they did not already know. Most participants anticipate a hike shortly.

Lastly, we note that the January light sweet crude oil futures are edging higher for the fifth session.While ideas that an agreement will be struck has been fanned by numerous press report, we continue to have nagging doubts. Yesterday we noted that many of the biggest cheerleaders are coming from places like Iran and Iraq that seek exemption from any agreement. Today we note that proposals presented at yesterday’s technical meeting called for those two countries to participate in cuts. Meanwhile, to prepare for a freeze in output, some producers, like Russia have boosted production. That said technical considerations are still favorable for higher prices.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,EUR/CHF,Eurozone Manufacturing PMI,Eurozone Markit Composite PMI,Eurozone Services PMI,FX Daily,gbp-chf,Germany Manufacturing PMI,Italy,newslettersent,SPY,U.S. Durable Goods Orders,U.S. Initial Jobless Claims,U.S. New Home Sales