Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc

|

Click to enlarge. |

FX RatesThe US dollar is trading with a small upside bias in narrow trading ranges. The main news has consisted of PMI reports, while investors continue to digest last week’s developments. In particular the BOJ’s underwhelming response to poor economic data and a missed opportunity to reinforce the fiscal stimulus, and the dismal US GDP. The dollar has been pinned today in the lower end of the 3.6 yen range seen before the weekend. It has held JPY102.00, but the recovery attempt in Tokyo found sellers in front of JPY102.70. The reversal of JGBs has continued. The sell-off since the BOJ’s disappointment has seen the generic 10-year yield rise from almost -30 bp to -12 today. The Nikkei rose (0.4%), while the Topix fell (0.1%). Financials were one of three sectors that rose (1.3%) in the Topix (the other two were telecom and health care). European bourses are mixed, leaving the Dow Jones Stoxx 600 little changed. Of note, the financials are off 0.8% in the immediate post-stress test response, the weakest sector. Within the financials, the banks are down as much as the sector. Monte Paschi is holding on to small gains, while the Italian banking sector is off 2.7%, giving back a chunk of the pre- weekend’s 3.8% gain. La Stampa reports that Renzi wants to hold the constitutional referendum in late-November. Previously it seemed as if it would be held in October. It will be interesting to see if Renzi tries to walk back his promise/threat to resign if the referendum is not accepted. Linking the government’s future to the referendum seems reckless as it turns the plebiscite into a potential political crisis. The euro is trading flat just below the pre-weekend highs near $1.12. The euro found support in the European morning near $1.1160. It feels like bullish consolidation. It may take a break of $1.1140 to shake out some weak longs. |

Click to enlarge. |

ChinaChina’s PMI readings were mixed. The official manufacturing reading slipped to 49.9 from 50, while the Caixin version rose to 50.6 from 48.6 ( a first reading above the 50 boom/bust in 17 months). The official reading, with a focus on large businesses, saw output and new orders slow, while new export orders fell. Caixin showed an increase in output and new orders, while the slump in new export orders slowed. The yuan appreciated against the US dollar for the fifth session, the longest run of the year. The yuan was fixed higher by the most in five weeks. Some are linking the yuan’s stability to several upcoming events, including the World Bank may issue SDR bonds in the coming weeks, the G20 meeting early next month, and the formal inclusion of the yuan in the SDR in a couple of months. On the other hand, today’s gains lack behind the basket that the PBOC ostensibly is tracking. The World Bank SDR bonds is reportedly a small issue (500 mln SDRs) to be issued in China’s interbank market. |

Click to enlarge. Source Investing.com |

EurozoneThe eurozone manufacturing PMI came stood at 52 in July. This is a touch better than the flash reading (51.9) but slower than the 52.8 in June. The improvement seemed to stem from Germany, where the final reading was 53.8 rather than the 53.7 flash and the 54.5 in June, which was a two-year high. France was unchanged from the flash reading for 48.6, compared with 48.3 in June. It is the fifth month below 50. Spain and Italy softened more than expected. |

Click to enlarge. Source Investing.com |

ItalyItaly’s manufacturing PMI eased to 51.2 from 53.5. It is the lowest reading since January 2015. The high for the year was set in April at 53.9. Spain’s manufacturing PMI fell to 51.0 from 52.2. It is the lowest since December 2013. |

Click to enlarge. Source Investing.com |

United KingdomRounding out the large European countries, the UK’s manufacturing PMI was even worse than the flash report indicated. The final reading stands at 48.2 The flash was 49.1. In June the diffusion index stood at 52.4, the highest level since January. New orders fell warning of downside risks. The only positive straw to grasp was export orders which were not as weak as the flash results. The came on the heels of the poor CBI outlook, which is the weakest since the end of 2012, with a net of 3% of firms looking to cut output. Sterling fell a cent from the Asia session high near $1.3275 to the European low near $1.3175. However, the fourth session, sterling is holding above the previous session’s low. A rate cut late this week is largely taken for granted, and other measures (asset purchases and funding-for-lending) are widely anticipated. The September short sterling futures contract implies a one bp higher now (44 bp) compared with the pre-weekend close. Support for sterling is pegged near $1.3150. |

Click to enlarge. Source Investing.com |

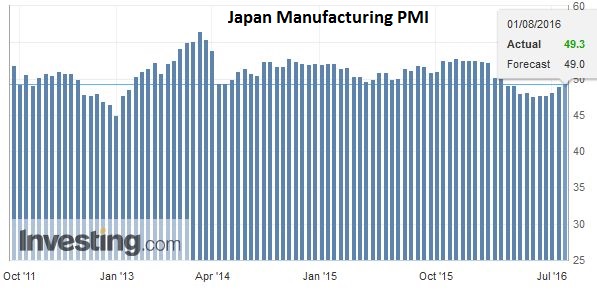

JapanIn Japan, the manufacturing PMI improved to 49.3 from the flash 49.0 reading. It is better than the 48.1 seen in June, but it is the fifth month below 50. The Bank of Japan is the subject of much speculation today. First, a local paper reported that the BOJ might drop its 2% inflation target next month. Second, there is speculation that Kuroda may step down, accepting that his approach has not generated the expected results. |

Click to enlarge. Source Investing.com |

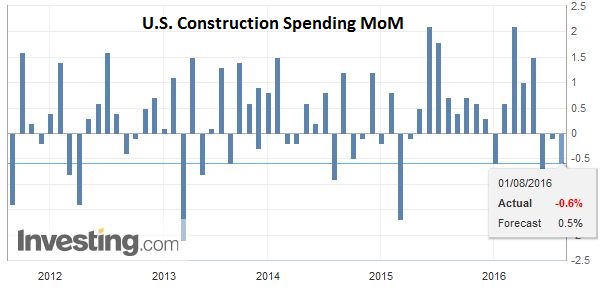

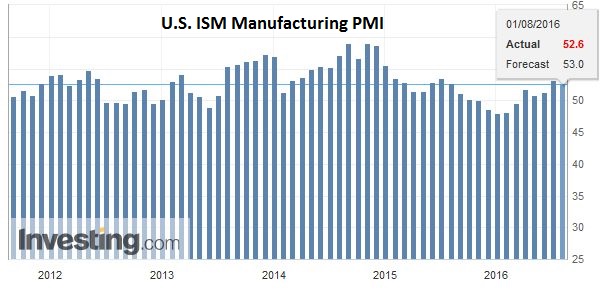

United StatesThe North American session features construction spending (with impact on Q2 GDP revisions) and the ISM manufacturing. |

Click to enlarge. Source Investing.com |

| It is expected to be little changed from June’s 53.2. Markit is expected to confirm its flash reading of 52.9, up from 51.3 in June, and the highest since last October. |

Click to enlarge. Source Investing.com |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Banca Monte dei Paschi,British Pound,China,China Manufacturing PMI,EUR/USD,Eurozone Manufacturing PMI,FX Daily,Italy Manufacturing PMI,Japan Manufacturing PMI,Japanese yen,newslettersent,U.K. Manufacturing PMI,U.S. ISM Manufacturing PMI