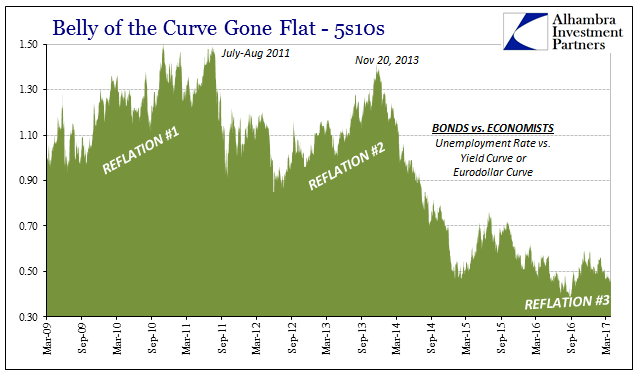

Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Die besten Möglichkeiten, in Deutschland Geld zu überweisen

Die besten Möglichkeiten, in Deutschland Geld zu überweisen9 Jan 2024

Two In-Depth Interviews

Two In-Depth Interviews12 Aug 2018

Jim Rogers – Making China Great Again! (Video)

Jim Rogers – Making China Great Again! (Video)12 Aug 2018

An Inquiry into Austrian Investing: Profits, Protection and Pitfalls

An Inquiry into Austrian Investing: Profits, Protection and Pitfalls11 Aug 2018

Jim Rogers and the World’s New Reserve Currency11 Aug 2018

The Yin and Yang of the US-China Relationship

The Yin and Yang of the US-China Relationship11 Aug 2018

FX Daily, August 10: The Dollar Muscles Higher as Turkey Melts Down

FX Daily, August 10: The Dollar Muscles Higher as Turkey Melts Down10 Aug 2018

The Swiss National Bank Now Owns $87.5 Billion In US Stocks After Q2 Tech Buying Spree

The Swiss National Bank Now Owns $87.5 Billion In US Stocks After Q2 Tech Buying Spree10 Aug 2018

The Stock Market is Stretched to Double Tech-Bubble Extremes

The Stock Market is Stretched to Double Tech-Bubble Extremes10 Aug 2018

Traffic jams cost Swiss more than just time

Traffic jams cost Swiss more than just time10 Aug 2018

What Chinese Trade Shows Us About SHIBOR

What Chinese Trade Shows Us About SHIBOR10 Aug 2018

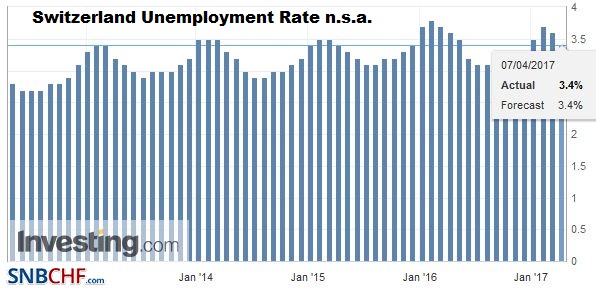

Switzerland Unemployment in July 2018: Unchanged at 2.4percent, seasonally adjusted unchanged at 2.6percent

Switzerland Unemployment in July 2018: Unchanged at 2.4percent, seasonally adjusted unchanged at 2.6percent9 Aug 2018

FX Daily, August 09: Sterling Remains Under Pressure, while the Greenback Firms Broadly

FX Daily, August 09: Sterling Remains Under Pressure, while the Greenback Firms Broadly9 Aug 2018

US-Japan Trade Talks

US-Japan Trade Talks9 Aug 2018

Swiss Trade Unions to Boycott Talks on EU Labour Negotiations

Swiss Trade Unions to Boycott Talks on EU Labour Negotiations9 Aug 2018

The Fantasy of “Balanced Returns” Funding Retirement

The Fantasy of “Balanced Returns” Funding Retirement9 Aug 2018

FX Daily, August 08: Sterling Can’t Get Out of Its Own Way, While Dollar and Yen Catch a Bid

FX Daily, August 08: Sterling Can’t Get Out of Its Own Way, While Dollar and Yen Catch a Bid8 Aug 2018

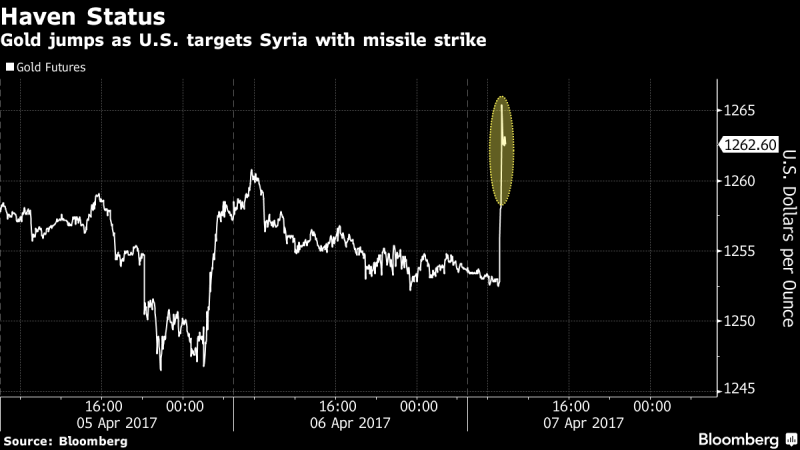

Gold—Even at its Lowest Levels in 2018—is Behaving Just as Prescribed

Gold—Even at its Lowest Levels in 2018—is Behaving Just as Prescribed8 Aug 2018

Some Initial Consequences of Trade Tensions

Some Initial Consequences of Trade Tensions8 Aug 2018

Global Asset Allocation Update – (VIDEO)

Global Asset Allocation Update – (VIDEO)8 Aug 2018