Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Household wealth in 2025

Household wealth in 202528 Apr 2026

16 Apr 2026

15 Apr 2026

21 Jan 2026

31 Jul 2025

SNB Brings Back Zero Percent Interest Rates

SNB Brings Back Zero Percent Interest Rates26 Jun 2025

25 Jun 2025

25 Jun 2025

24 Jun 2025

20 Jun 2025

20 Jun 2025

20 Jun 2025

20 Jun 2025

19 Jun 2025

19 Jun 2025

19 Jun 2025

19 Jun 2025

Was kann die Schweizerische Nationalbank tatsächlich bewirken?

Was kann die Schweizerische Nationalbank tatsächlich bewirken?12 Jun 2025

Swiss National Bank Trials Blockchain to Modernise MDB Financial Processes

Swiss National Bank Trials Blockchain to Modernise MDB Financial Processes24 Apr 2025

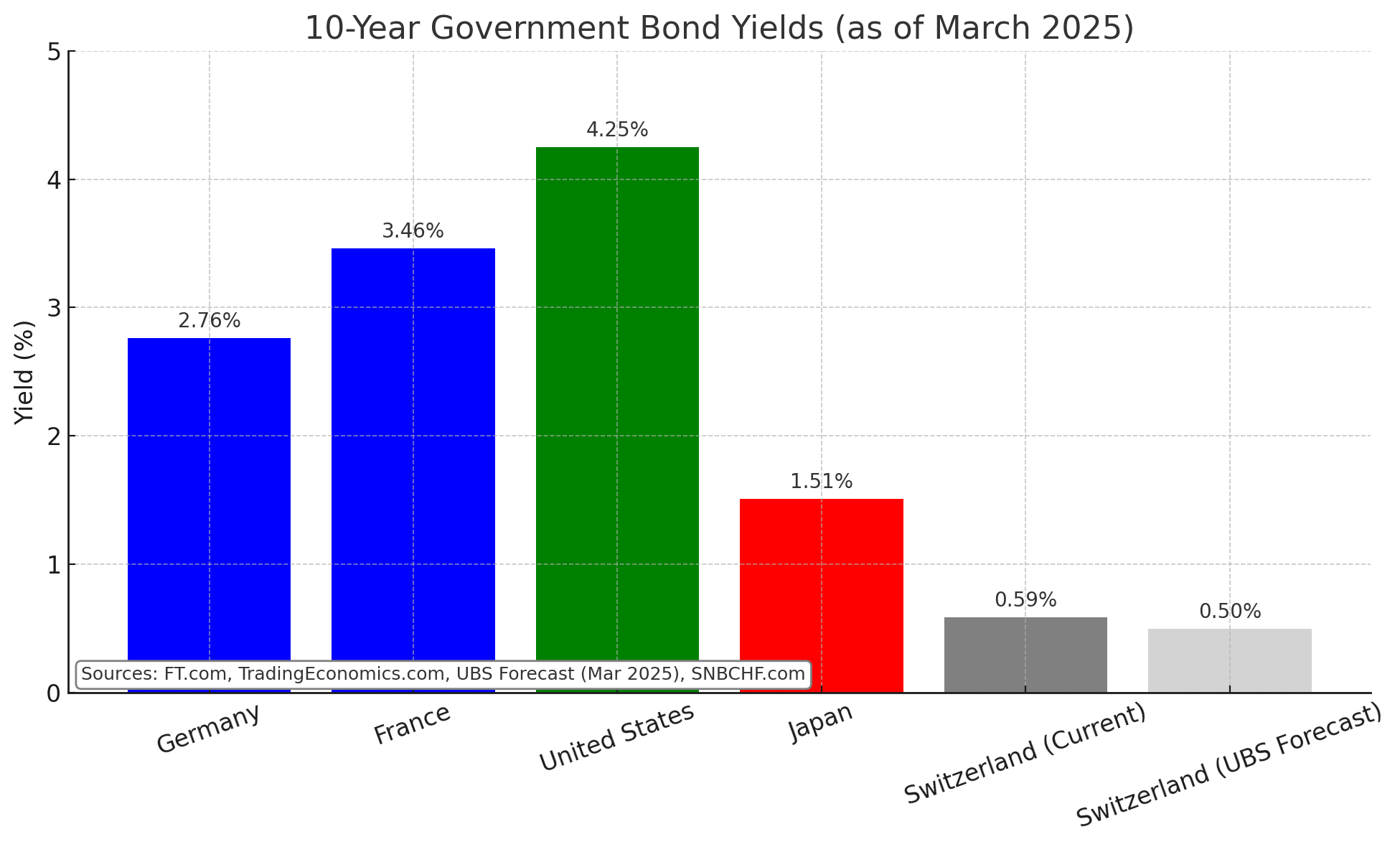

SNB Monetary Assessment March 2025

SNB Monetary Assessment March 202523 Mar 2025