- Swiss Franc is vulnerable as inflation data continues to undershoot official forecasts.

- The SNB expected inflation to average 1.9% in 2024 in its December forecast, but it currently sits at 1.2%.

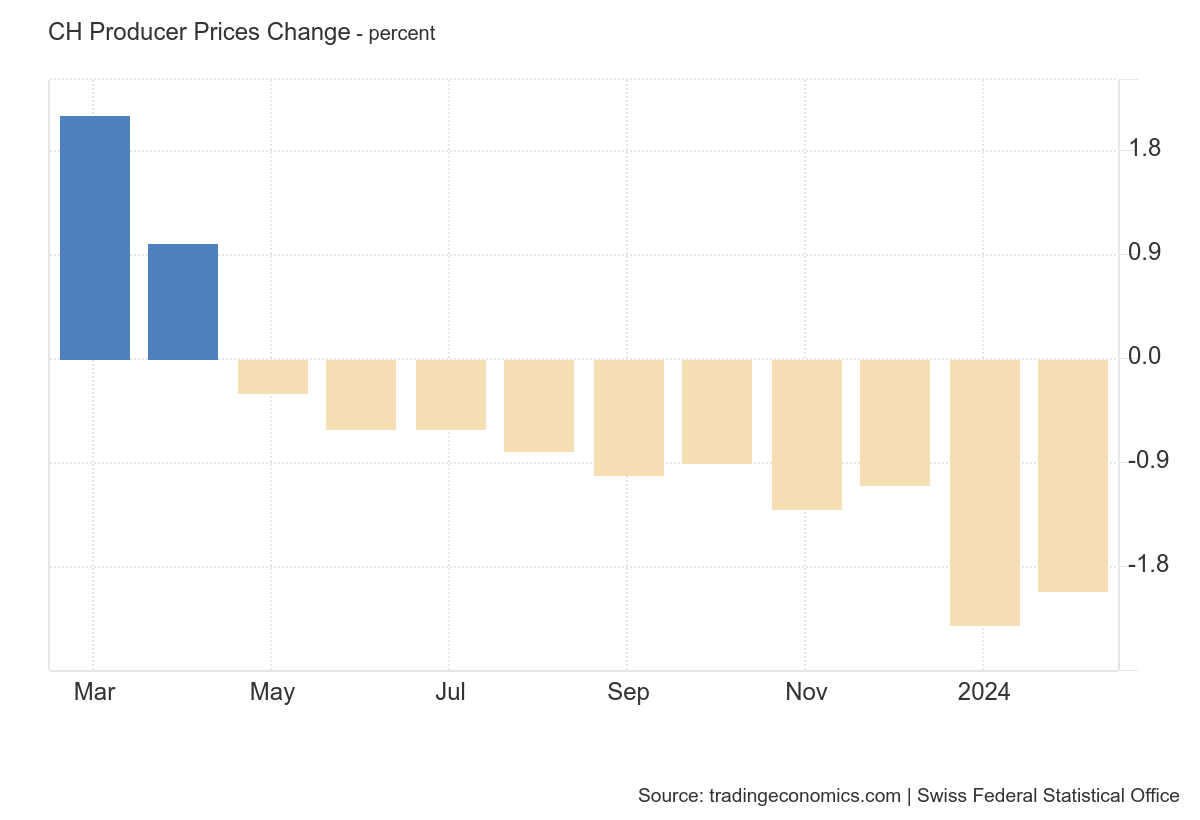

- The latest Producer and Import Prices showed the tenth month of deflation in a row.

The Swiss Franc (CHF) trades flat at the end of the trading week – off by barely a few hundredths of a percent in its most traded pairs. The overal fundamental outlook is not particulay favourable for CHF given Swiss inflation continues to decline and diverge from official estimates. This suggests the Swiss National Bank may need to ease policy, a generally negative factor for the currency as it attracts lower inflows of foreign capital.

In its latest macroeconomic data release, Swiss Producer and Import Prices continued their deflationary trend in February, registering deflation for the tenth consecutive month at minus 2.0% (from negative 2.3% in January), according to data from the Federal Statistical Office.

Swiss Franc at risk as inflation remains below SNB forecast

The Swiss Franc could be vulnerable to weakening further as inflation in Switzerland looks increasingly likely to undercut official forecasts.

In its latest batch of data, Swiss headline inflation rose 1.2% YoY in February, down from 1.3% in January, and increased 0.6%, up from 0.2% in January, on a month-on-month basis.

The data shows that inflation is undercutting the Swiss National Bank’s (SNB) own forecasts, which at its December policy meeting expressed the view that inflation would start rising from the 1.4% registered in November.

“However, inflation is likely to increase again somewhat in the coming months due to higher electricity prices and rents, as well as the rise in VAT.” The SNB said in its December policy statement.

The SNB implemented a rate hike of 0.25% in June 2023, raising rates from 1.50% to 1.75% to combat the threat of higher inflation. However, given the opposite has happened and inflation has actually come down quicker than expected, there is now a risk it could cut interest rates, which would be negative for the Swiss Franc, since lower rates attract less inflows of foreign capital.

The possibility of a change in policy is increased by the fact that inflation is running well below the SNB’s 1.9% forecast for 2024. Although there is only two months of data so far, it will have to rise substantially to meet the bank’s forecast before the end of the year. The SNB’s next policy meeting is on March 21.

SNB’s Jordan thinks Swiss Franc is too expensive

The Chairman of the SNB Thomas Jordan has expressed concerns about the Swiss Franc's excessive strength, particularly its impact on Swiss businesses, especially exporters. These concerns are reflected in data from Switzerland's Foreign Exchange Reserves (CHFER), which show a recovery in Forex reserves in 2024, indicating that the SNB may be selling Swiss Francs to bring the exchange rate down.

Technical Analysis: Swiss Franc oscillates in short-term range versus USD

The USD/CHF, which measures the number of Swiss Francs that one US Dollar can buy, has been oscillating within a relatively tight range between roughly 0.8900 and 0.8740 since the middle of February.

The pair is overall in short-term uptrend with the expectation that it will eventually breakout from the current range and start moving higher. However, resistance from a long-term trendline and the 50-week Simple Moving Average (SMA) present considerable obstacles to a prolongation of the trend.

US Dollar versus Swiss Franc: 4-hour chart

For more upside to be confirmed, a decisive break above the range highs at 0.8900 would be required. Such a move would probably then extend to an initial target at 0.8992, the 0.618 Fibonacci ratio of the height of the range extrapolated higher, followed by 0.9052, the full height extrapolated higher.

A decisive break below the range low at 0.8729, however, could indicate a short-term trend reversal and the start of a deeper slide lower. The first target for the move lower would be the 0.618 extrapolation of the height of the range at 0.8632, followed by the full extrapolation at 0.8577, which is also close to the 0.8551 January 31 lows, another key support level to the downside.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Tags: Featured,newsletter