Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Ukraine and the Next Wave of Inflation, Part II, Can Russia Enact a Gold Standard?

Ukraine and the Next Wave of Inflation, Part II, Can Russia Enact a Gold Standard?13 Mar 2022

Mapping the Conflict in the Ukraine

Mapping the Conflict in the Ukraine12 Mar 2022

What’s In Your Loan?

What’s In Your Loan?29 Nov 2021

17 Aug 2021

Post-Covid China

Post-Covid China5 Jul 2021

COVID in India

COVID in India26 May 2021

Did You Make Janet Yellen Rich?

Did You Make Janet Yellen Rich?8 Feb 2021

Grantham’s ‘Real McCoy’ Bubble in a World Gone Mad

Grantham’s ‘Real McCoy’ Bubble in a World Gone Mad21 Dec 2020

Janet Yellen: Too Dumb To Stop

Janet Yellen: Too Dumb To Stop10 Dec 2020

What You Will Find When You Follow the Money

What You Will Find When You Follow the Money17 Aug 2020

The Dollar Is Dying

The Dollar Is Dying11 Aug 2020

Silver “Scarcifies” – Precious Metals Supply and Demand

Silver “Scarcifies” – Precious Metals Supply and Demand31 Jul 2020

Game Over Spending

Game Over Spending13 Jul 2020

An Excellent Seasonal Buying Opportunity in Silver Lies Directly Ahead

An Excellent Seasonal Buying Opportunity in Silver Lies Directly Ahead29 Jun 2020

The Decline of the Third World

The Decline of the Third World24 Jun 2020

US Money Supply – The Pandemic Moonshot

US Money Supply – The Pandemic Moonshot16 Jun 2020

In Gold We Trust, 2020 – The Dawning of a Golden Decade

In Gold We Trust, 2020 – The Dawning of a Golden Decade3 Jun 2020

Gold Stocks – A Show of Strength

Gold Stocks – A Show of Strength17 Apr 2020

The Secret to Fun and Easy Stock Market Riches

The Secret to Fun and Easy Stock Market Riches18 Feb 2020

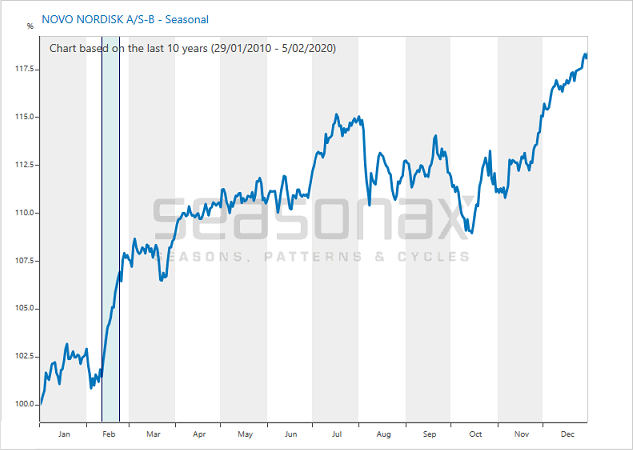

A Pharmaceutical Stock That Is Often Particularly Strong At This Time Of The Year

A Pharmaceutical Stock That Is Often Particularly Strong At This Time Of The Year15 Feb 2020