Pater Tenebrarum

My articles My siteAbout meMy videosMy books

Follow on:TwitterSeeking AlphaFacebook

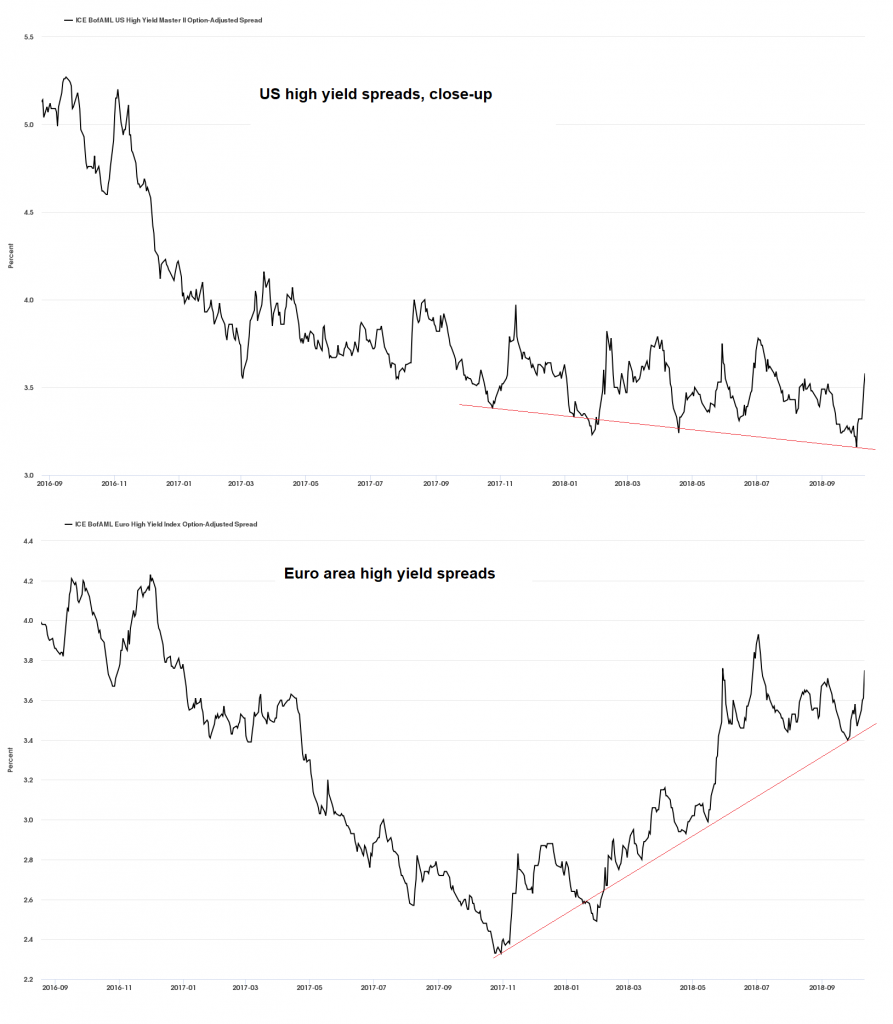

Fibonacci RetracementsFollowing the recent market swoon, we were interested to see how far the rebound would go. Fibonacci retracement levels are a tried and true technical tool for estimating likely targets – and they can actually provide information beyond that as well. Here is the S&P 500 Index with the most important Fibonacci retracement levels of the recent decline shown: So far, the SPX has made it back to the 61.8% retracement level intraday, and has weakened a tad again since then. This is not yet conclusive evidence that this level will contain the rebound, but it is worth noting that the RSI made it back to just below 50 as well (the 40-50 area in the RSI is often an important demarcation in both bullish and bearish market phases). On the other hand, the decline has injected somewhat greater caution than was detectable previously (e.g. the VIX remains around the 20 level). That may help support a larger rebound; note also that the 200-dma serves as support, so an argument could be made that the decline was merely one of the periodic tests of this moving average. One should watch what happens if lower Fibo retracement levels, i.e., the 50% and 38% retracement are approached from above. According to Canadian technical analyst Ross Clark, statistics suggest that the 38% level must hold to maintain a positive bias. If it breaks, a retest of the lows becomes the minimum expectation. |

S&P 500 Large Cap Index, Feb 2017 - 2018(see more posts on S&P 500 Large Cap Index, ) - Click to enlarge |

A New Acronym to Remember – DARTWe mentioned that we would occasionally talk about rarely discussed indicators and familiarize readers with new acronyms, and here is one of them. Some of our readers may have seen this chart already, as it is slightly dated by now (it was first published by sentimentrader on January 18, prior to the market swoon). The acronym in question is DART, which stands for “daily average revenue trades” at two major discount brokerages, E-Trade and TD Ameritrade. Here is the chart: The “DART” index of retail trader activity at two of the largest discount brokers as of January 18. We include this slightly dated chart because it shows how intense emotions were near the recent top. Such data are important in determining the potential importance of a market peak. In conjunction with all the other sentiment and positioning data we recently discussed, it suggests that it won’t be easy to overcome the January 2018 peak. If this peak cannot be overcome in a fairly short period of time, there will be only one way for the market to go, and that will no longer be up. |

Trading Activity and Retail Focused Brokerages is Skyrocketing, 2003 - 2017 - Click to enlarge |

The importance of this burst of optimism near the top may be mitigated by a commensurate, rapid surge in fear upon a renewed decline. Whether that actually happens remains to be seen. Keep in mind that the most important fundamental pillar supporting the rally – namely true money supply growth – has withered away dramatically since November 2016 and has reached levels historically associated with important tops (broad money supply TMS-2 at less than 3% y/y).

Neither the market’s overall technical underpinnings nor fundamental economic data are sending anything worse than a somewhat mixed message at present – i.e., they are not providing unequivocal warning signs. But we are in a unique situation after the “QE” era, and the importance of data points such as the DART index or the DSI (the daily sentiment index of futures traders, which at the peak became an exact mirror image of the situation in March 2009, with the percentage of bulls and bears switching places to 97% bulls and 3% bears) is enhanced due to the weakness in money supply growth.

Full story here Are you the author?Tags: newslettersent,S&P 500 Large Cap Index,The Stock Market