Keith Weiner

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaFacebookAmazonGoogle +

You Actually Can Eat Gold, But Its Nutritional Value is Dubious“You can’t eat gold.” The enemies of gold often unleash this little zinger, as if it dismisses the idea of owning gold and indeed the whole gold standard. It is a fact, you cannot eat gold. However, it dismisses nothing. This gives us an idea. Let us tie three facts together. One, you can’t eat gold. Two, gold is in backwardation in Switzerland. And three, speculation is a bet on the price action. The fact that gold is inedible is supposed (by the enemies of liberty) to be proof positive that a gold standard wouldn’t work. Of course, there’s always the retort: You can’t eat dollars! |

Over-the-top garnish: Gold leaf-laced donut (reportedly costs $100), gold-laced cakes, sushi roll with gold leaf (according to Japanese lore, eating it is supposed to bring luck), gold-cake eater in Dubai. Nutritional value of the gold leaf is zero, but at least it isn’t toxic. So yes, one can eat gold, but it won’t relieve hunger pangs. We would like to point out here that absolutely no-one is trying to eat bank note-laced cakes. [PT] |

| That may be emotionally satisfying, but there is a deeper issuer that the anti-gold crowd is missing. Yes, money makes terrible food but, also, food makes terrible money. A car makes a lousy airplane. And a shoe makes an awful TV. Cow poop is putrid as food for people, but it works well as fertilizer for plants. Each thing fits a particular purpose.

Why does food make terrible money? One reason is that it’s perishable. No one — other than a refrigerated warehouse — can make a bid on food beyond his own short-term needs. Without this robust bid, food has limited marketability. That is, it has a wide spread between its bid and offer prices. Think of it in human terms, or even personal terms. Suppose you strolling along the sidewalk, and you’re hungry. You see a restaurant sign, “Hamburger + fries + drink $10.” You would pay the offer price. The next restaurant is going out of business, and its sign says, “All inventory must go! 50 hamburgers and 50 pounds of fries for $100!” You would not pay it (unless you were with 49 friends). Why not? It’s because you can’t possibly carry 49 juicy hamburgers and 49lbs of hot, greasy fries with you as you walk! The bid price is zero or nearly zero. So the bid-ask spread on food is quite wide. Other than for eating, a hamburger serves no purpose. And you only need to eat a finite amount (unless you are Hafthor Bjornsson). Any burgers beyond that are of no value to you, because they don’t keep very long. You don’t want to stockpile them. Economists would say that the marginal utility of hamburgers falls rapidly. The first hamburger satiates your hunger. The second fills you up. The third, well, maybe you were really hungry. The fourth doesn’t do anything for you. It’s useless. |

For a few hamburgers more, there is always Icelandic strongman Hafthor Bjornsson. [PT] Photo credit: HBO |

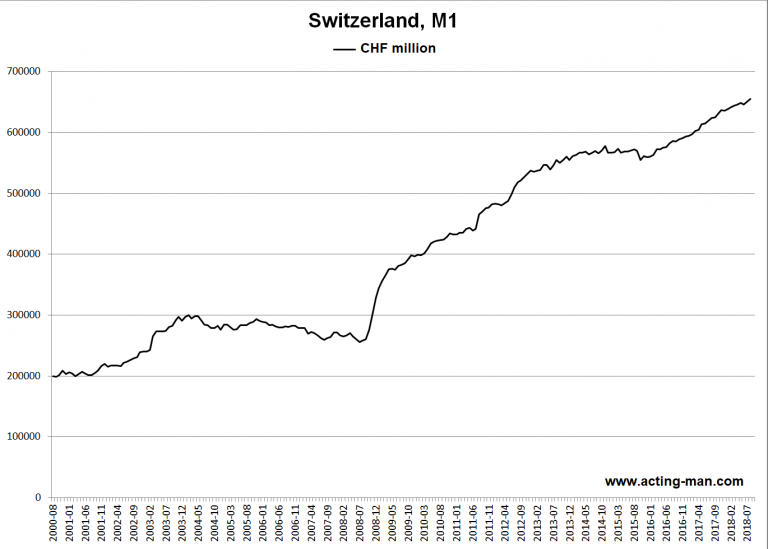

Gold is in Backwardation in SwitzerlandNow we switch to the second topic. Gold is in backwardation in Switzerland. What does that really mean in human terms? It means you can give up your 100oz gold bar for 3 months, get free use of about CHF 120,000 in the meantime, and in the end get your gold bar back. Plus about CHF 400 in profit. No one is taking this deal. Let that sink in. Lots of people have these gold bars. Which they cannot eat, as we have already proven. But they won’t let them go for even three months. The free use of francs and the profit are not attractive. This either means they don’t trust their counterparty to give the gold back, or else that the francs are even more useless than the gold. Given the high price of the franc — just over $1 — we don’t think that the problem is trust of the counterparty. We would say (and have argued these past few weeks) that the problem is that the Swiss National Bank so flooded the market with francs that they’re now useless. So useless, that people will not decarry gold for a profit. So useless that the bid to borrow them — the bid on the interest rate — is negative. |

Switzerland: Narrow monetary aggregate M1 since August of 2000. Switzerland: Narrow monetary aggregate M1 since August of 2000. The printing presses have been busy at the SNB. [PT] - Click to enlarge |

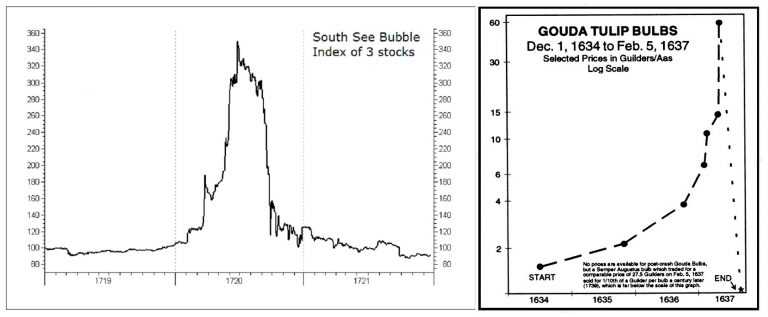

Speculative Assets Are UselessSwitching topics again, let’s return to something we have often criticized: buying stocks or bitcoin with the hope that the price will rise. Why will it rise? Because the next guy will come along and bid higher. Why will he do that? Because he expects the yet another buyer to bid even more. And so on? No. There is an end to this cycle. Inevitably, the supply of buyers is depleted. And then what happens is silver in the spring of 2011. Or stocks in 2008. Or tulips in 1637. Why are there no more buyers? To answer, let’s tie all three of these seemingly isolated facts together. People are buying something, not for any use they can make of it, but solely to front-run that next buyer. He also has no use for it, but merely buys to unload to the next buyer in the chain. They’re all buying something they can’t use, in the hopes of selling it, but no one is asking if anyone has any use for it! This is why mainstream investors do not buy gold. We, the gold community, must change our message if we want to reach them. “Gold’s going to $10,000” is not reaching them. At best, mainstream investors think “maybe”. Or else they think, “You have predicted 93 of the past 0 gold spikes to $10,000.” If the only purpose of a thing is to sell it for a higher price, then that thing has no purpose. This could almost be a corollary to Mises’ Regression Theorem. Anyways, gold (unlike francs nowadays, or tulips back in the 17th century) does have a productive purpose. We spill a lot of words talking about borrowing, lending, interest, debt, extinguishing debt, and servicing debt. We dismiss the definition of money commonly held to be the “medium of exchange” as wrong. We believe that it smuggles in the premise that the government can change economic law merely by enacting legislative law. It is more important to look at whether a thing can extinguish debt than whether it trades for hamburgers. Why is money not defined in terms of purchasing power, but as the most marketable good? Why is it important to compare the hamburger, whose marginal utility falls to zero, the franc, whose marginal utility is now apparently negative, with gold whose marginal utility is a flat-line or nearly so? |

Famous speculative bubbles of the past Famous speculative bubbles of the past – the early 18th century South Seas bubble in England (left) and the 17th century Dutch Tulipomania (right) - Click to enlarge |

Money is Gold, Gold is MoneyThe hamburger is food because it provided nutrition. Gold is money because it has the narrowest bid-ask spread of any commodity. It has the highest stocks to flows, which shows that its marginal utility declines so little — that after thousands of years of accumulation, we’re still mining more. It is the most marketable commodity, because it has a use to billions of people. That use is final payment. Even if most people, most of the time, are happy to be creditors, some people some of the time want to be finally paid. Gold, the extinguisher of debt, is final payment. There is never any question about the value of something that has constant or nearly constant marginal utility, because it is final payment demanded by billions of people. Note: we are not saying payment as in exchange for goods. We are saying payment as in what a creditor demands in satisfaction of the debt. Money is a capital asset. It is not necessarily the hot potato that people receive as wages, and rapidly turn around to pay for goods. Consider the case that China sells consumer goods to America to obtain dollars, just in time to pay Venezuela for oil. And they, in turn, pay them out in wages, machine parts, and welfare largesse. For this scenario, any old medium of exchange will do. The dollar works fine, and the parties involved would not agree if you denied it. But money is the thing which is valued specifically to hold, and for the sake of holding it. Unlike the dollar, which can clear trade as a medium of exchange but is not good for saving—gold is good for saving. Unlike bitcoin, which people speculate will have greater purchasing power. They plan merely to exchange bitcoin for a greater quantity of consumer goods tomorrow. If something is just a token held to trade for consumer goods, it is not a capital asset. It is just deferred consumption, just a deferred consumer good. Keynes taught that consumption makes the economy go. We suppose that, to Keynes, if an asset goes up and people can sell it to consume more, this is a good thing. Anyway, Keynes was utterly wrong. This is a frivolous error. One cannot consume something that has not been produced. Production must precede consumption. For hundreds of thousands of years, humans lived at the level of subsistence. They could only produce whatever could be done with their own hands, and at best simple hand tools. They did not accumulate capital. Capital accumulation and investment make the economy go. Keynes misses this fact, along with all who love the (seemingly) endless rise in asset prices driven by the (pathologically) falling interest rate. They think that it’s possible to consume without producing, by just betting on rising prices. They don’t know that they are just eating the seed corn. So long as one man has a surplus of hamburgers and another has a surplus of gasoline, they will want to trade. So long as men want to trade, there will be some kind of medium of exchange. But that medium of exchange is not necessarily money. That medium can convey value, but not store nor measure it. JP Morgan said it best, in his testimony before Congress. “Money is gold, and nothing else.” |

He be our witness: Gold bug of yore, James Pierce-eye Morgan the Grim, in his own terrifying splendor. [PT] |

Precious Metals Supply and DemandNot Like 2008The price of gold went up $14 last week, but the price of silver fell 3 cents. The fundamentals are firming up a bit, more in gold than in silver, while the S&P index has fallen 125 points — over 4% — in a week. So far, this seems to be playing out as we said it could. The stock market has been on a steady escalator trip upwards since Obama took office. By contrast, the prices of the metals have been down and sideways since 2011. So if there is a rising crisis due to rising rates, falling currencies, debtor defaults and all the rest of the syndrome, then the precious metals would not necessarily behave as they did in 2008. Recall that by the crisis, the metals had been in a bull market for seven years. Now they have been in a bear market for that same length of time. |

S&P 500 Large Cap Index vs. Gold(see more posts on S&P 500 Large Cap Index, ) Moving in opposite directions: SPX vs. gold [PT] - Click to enlarge |

Fundamental DevelopmentsWe will look at the supply and demand fundamentals of both metals. But, first, here is the chart of the prices of gold and silver. |

Gold and Silver Price(see more posts on gold price, silver price, ) - Click to enlarge |

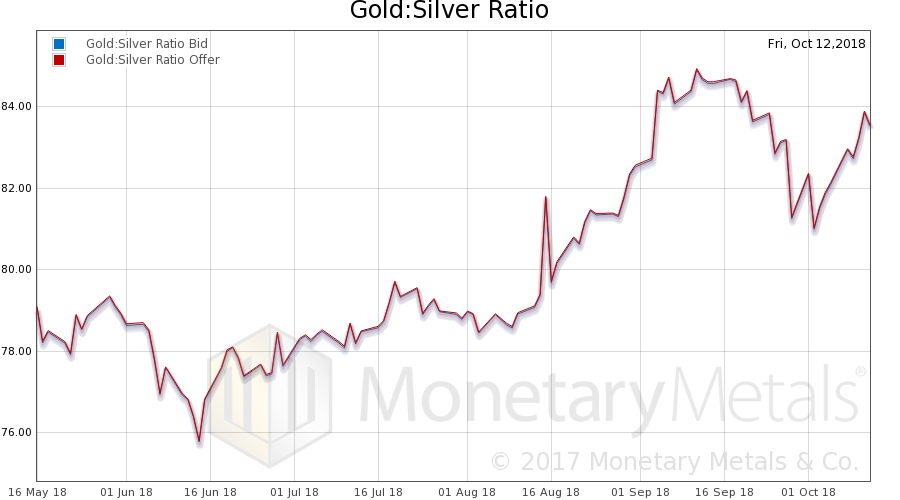

Gold:Silver RatioNext, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio). It rose this week. |

Gold:Silver Ratio(see more posts on gold silver ratio, ) - Click to enlarge |

Gold Basis and Gold Co-basisHere is the gold graph showing gold basis, co-basis and the price of the dollar in terms of gold price. The price of the dollar dropped a bit, again this week. We don’t say this merely to be pedantic. If one thinks that gold goes up and down, and that the very measure of altitude is the dollar, then one cannot understand what is really going on. One should see a week like this one as a drop in the value of the dollar, not a rise in gold. With that drop in the dollar, we have an increase in the scarcity of gold. One commentator on Twitter this week wondered why they didn’t issue more shares of GLD as the price rose. The answer is that the price rise was not centered in GLD, but in metal. The Monetary Metals Gold Fundamental Price turned around, rising from $1,272 to $1,299. |

Gold Basis and Gold Co-basis(see more posts on dollar price, gold basis, Gold co-basis, ) - Click to enlarge |

Silver Basis and Silver Co-basisNow let’s look at silver. In silver, of course the metal became scarcer. Of course, because its price fell. That is, we are not looking for where the buying was focused. We are looking for where the selling was focused. As is the typical pattern, speculators were selling futures. The Monetary Metals Silver Fundamental Price also rose a few pennies, from $15.27 to $15.31. |

Silver Basis and Silver Co-basis(see more posts on dollar price, silver basis, Silver co-basis, ) - Click to enlarge |

Charts and data by: acting-man, SNB, Larry Neal, EWI, StockCharts, Monetary Metals

Chart and image captions by PT

Full story here Are you the author?Tags: Chart Update,newsletter,Precious Metals,S&P 500 Large Cap Index