Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has risen by 0.17% to 1.0976 |

EUR/CHF and USD/CHF, May 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

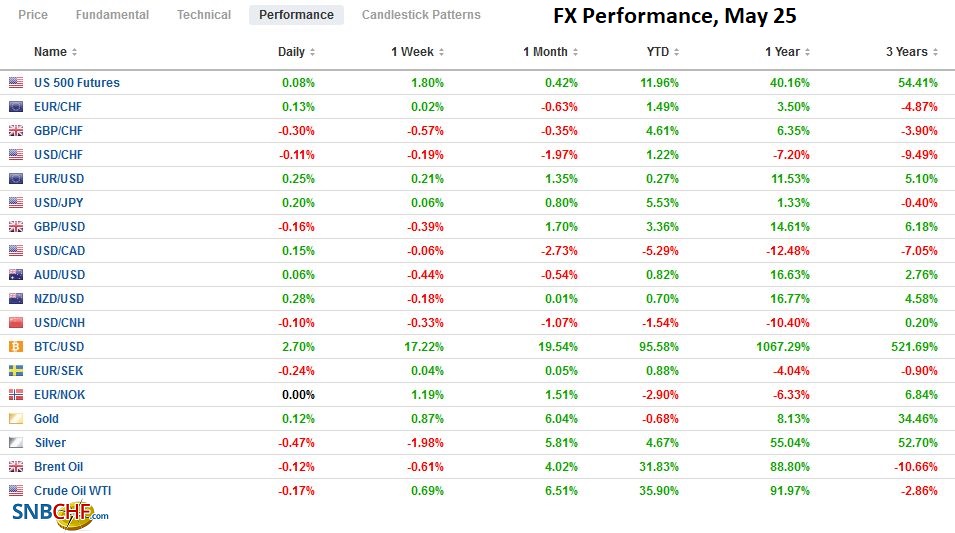

FX RatesOverview: The decline in US 10-year rates to two-week lows below 1.59% is helping rebuild bullish enthusiasm for stocks and weighing on the US dollar. The NASDAQ reached two-week highs yesterday, and almost all the large markets in the Asia Pacific region rose, though India struggled. Europe’s Dow Jones Stoxx 600 is at a new record high, paced by real estate and information technology. US futures are firmer, pointing to a possible gap higher opening. European yields are mostly 2-4 bp lower, and premiums over German are narrowing. The spread between Italy and German 10-year rates has narrowed more than seven basis points from last week’s peak, for example. The dollar is on its back foot. The Swedish krona’s 0.65% gain is leading the move against the dollar. It is at a three-month high versus the greenback, while the euro and Swiss franc are about 0.30% higher. The Canadian dollar and Japanese yen are laggards and little changed. Emerging market currencies are also mostly higher. Hungary, whose central bank is expected to standpat later today, and Turkey, where a central bank’s deputy governor has been dismissed, are struggling. Industrial commodity prices are firm, but July WTI is coming back offered after briefly rising to nearly $66.35. A week ago, it set the contract high a little above $67. Gold remains firm but holding a little below last week’s high, around $1890. |

FX Performance, May 25 - Click to enlarge |

Asia Pacific

The US issued a do-not-travel advisory to Japan, the most serious warning due to the outbreak of the covid infection. The inoculation rate is reportedly around 4%, the least among high-income countries (OECD 37 members). The opening ceremony for the summer Olympics is less than two months away. Initially, the Olympics were expected to draw 600k foreign visitors, not counting the athletes. In March, this was cut to around 78k. The US warning raises new questions. Next month, a decision will be made whether local spectators can attend the events. Meanwhile, there is pressure to extend the formal emergencies in Tokyo and Osaka into next month, and Prime Minister Suga is expected to decide in the coming days.

The Shanghai Composite jumped 2.4% today, the most since last October to reach a three-month high. A record amount of A-shares was bought through the HK links (CNY21.7 bln or ~$3.4 bln). Efforts to rein in commodity prices were cited as a factor that boosted confidence. Financials did particularly well. The offshore yuan (CNH) was particularly strong, and the dollar is trading below CNH6.40 for the first time in three years. The onshore yuan held up a little better. The greenback held above CNY6.40 but still made a marginal new three-year low. There was talk that state-own banks were dollar buyers late in the session after selling earlier in the session. Some observers link the dollar buying to “stealth” intervention, but of course, they also operate for their own accounts, and taking some profits with yuan at three-year highs could be good trading and rebalancing after the surge of inflows. Note that exporters often convert their proceeds toward the end of the month.

The US is confined to a narrow 30-pip range against the Japanese yen. It found support near last week’s low that was just above JPY108.55, and the greenback was offered near JPY108.85. Only a move above JPY109.05 or below JPY108.35 is of note. The Australian dollar also appears to be going nowhere quickly. It is in about a 15-tick range on either side of $0.7760. The Aussie has not settled off the $0.7700-handle for two weeks. The PBOC set the dollar’s reference rate at CNY6.4283, which was a bit stronger than the bank models Bloomberg survey projected (CNY6.4263). Tomorrow’s fix will be closely scrutinized for policy signals.

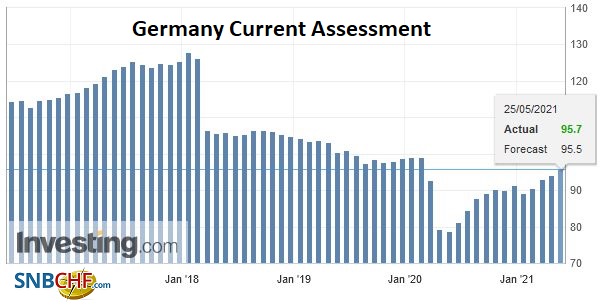

GermanyAlthough political uncertainty ahead of the September elections has been heightened by the tightening of the polls, economic confidence is strong. The May IFO survey results were better than expected, encouraged by the accelerated vaccination effort that has seen about 40% of adults now have at least one shot. As a result, the current assessment rose to 95.7 from a revised 94.2 in April (initially 94.1). |

Germany Current Assessment, May 2021(see more posts on Germany Current Assessment, ) Source: Investing.com - Click to enlarge |

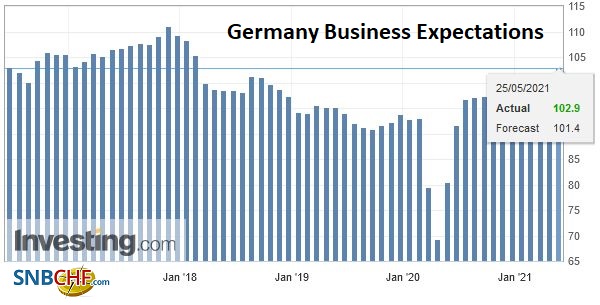

| Expectations, which stalled in April (falling to 99.2 from 100.4 in March), jumped to 102.9 in May. |

Germany Business Expectations, May 2021(see more posts on Germany Business Expectations, ) Source: Investing.com - Click to enlarge |

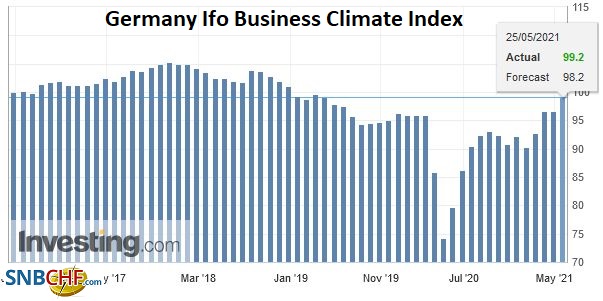

| That lifted the overall view of the business climate to 99.2 from 96.6 (initially 96.8). It is the highest since May 2019. |

Germany Ifo Business Climate Index, May 2021(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

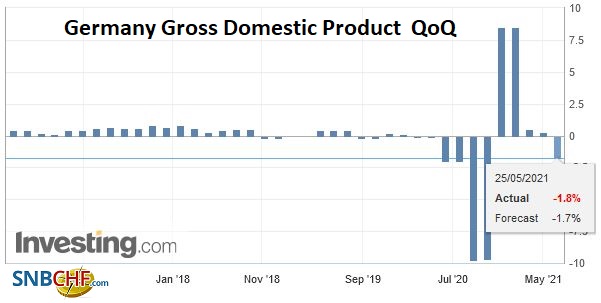

| The fact that Q1 GDP was revised to show a contraction of 1.8% instead of -1.7% had little impact. |

Germany Gross Domestic Product (GDP) QoQ, Q1 2021(see more posts on Germany Gross Domestic Product, ) Source: Inesting.com - Click to enlarge |

The EU’s confrontation with its neighbors is running at a high level. It is preparing more sanctions against Belarus. Brussels is also pushing back against the UK’s demands that the withdrawal agreement is renegotiated. It continues to have regrets about the Northern Ireland protocol. The EU is also at odds with Switzerland. A pandemic seems to be an awful time to do it, but the EU will go forward with downgrading Swiss medical technology exports to the EU. Starting next month, Swiss medical firms cannot export into the EU duty-free. Instead, such firms need to be represented within the EU and meeting product-labeling requirements.

The euro is trading above last week’s high (~$1.2245) and, for the first time in four months, has not traded below $1.2200. The next hurdle is seen near $1.2275, where an option for about 980 mln euros will expire today. The intraday momentum indicators are stretched. Initial support is seen in the $1.2220-$1.2230 area.

Sterling is firm, and although it has traded above $1.42, there has not been much follow-through buying, and it has held below the pre-weekend high (~$1.4235). It has retreated in the European morning and could return to the $1.4150-$1.4160 support area.

America

The Federal Reserve bought $2 bln of Treasury Inflation-Protected Securities yesterday and insists on using it as a clean signal of the market expectations. Today, housing price data and new home sales will be reported. It makes one wonder why the Fed is still buying $40 bln a month in agency mortgage-backed securities. Case-Shiller house price index of 20 cities is expected to continue to accelerate over 12% in March, the fastest in seven years. New home sales may have pulled back in April after a nearly 21% jump in March. Constraints in supply are an important factor. The median forecast in Bloomberg’s survey calls for a 950k seasonally-adjusted annual pace. A 13-year high was set in January 2020 at an almost 775k pace. It has not been below an 840k rate since May 2020.

Mexico reported its biweekly inflation read yesterday. It eased to 5.80% from 6.12% but was higher than expected, and the core rate was rose by 0.33% on the month, twice the median forecast in Bloomberg’s survey. It confirms, though, what was already known. Banixco easing cycle has ended. Today’s focus turns to the trade balance, where March’s $3 bln deficit was a surprise. Economists forecast another deficit in April but a fifth of the March shortfall. A caveat is in order. There seems to be a strong seasonal pattern of deterioration in April from March (16 of the past 20 years, the April shortfall was larger than March).

Brazil reports the IPCA inflation, and prices continue to surge. It is expected to rise to 7.38% from 6.17% in April. There is some base-effect, but prices in the January-April period have risen at an annualized rate of more than 11%. The central bank has already indicated it will follow up the two 75 bp rate hikes (lifting the Selic rate to 3.50%) with a third one when it meets next on June 16. The Selic rate was at 4.40% at the end of 2019.

The US dollar remains trapped in its trough against the Canadian dollar. It remains just inside the pre-weekend range of roughly CAD1.2025 and CAD1.2095. A four-year low was set on May 18, a little below CAD1.2015. A convincing break of CAD1.2000 would have significant technical implications. Last week’s high near CAD1.2145 seems like a distant memory. The greenback held below MXN20.00 yesterday, and follow-through selling today pushed it below MXN19.82. Last week’s low, which is the next target, was around MXN19.72.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brazil,China,Currency Movement,EUR/CHF,Featured,Germany,Japan,Mexico,newsletter,USD/CHF