Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

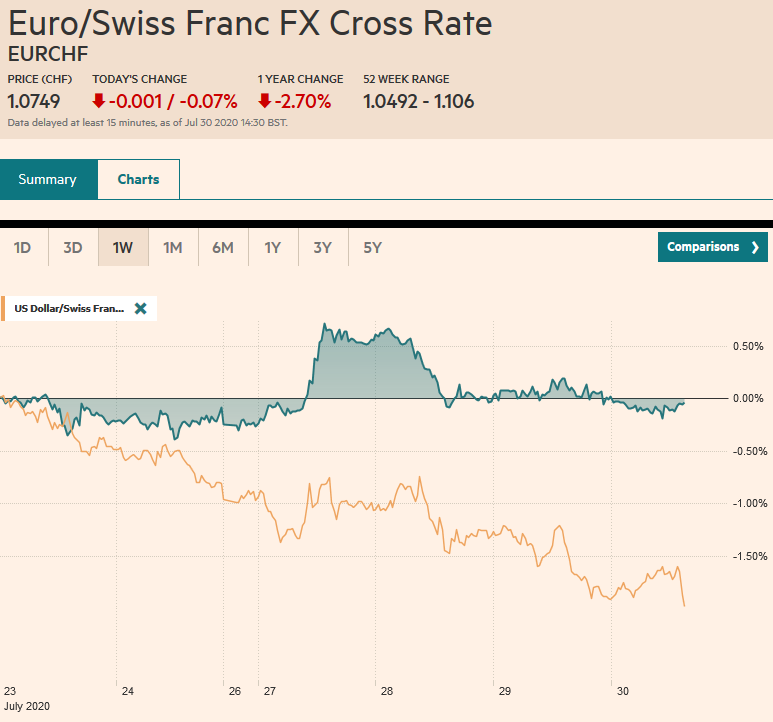

Swiss FrancThe Euro has fallen by 0.07% to 1.0749 |

EUR/CHF and USD/CHF, July 30(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A wave of profit-taking is seen through most of the capital markets today, with the exception of the bond market, where yields continue to trend lower. The US 10-year is now yielding 55 bp, a new low since early March, and the five-year yield set a new record low near 23 bp. European yields are 2-4 bp lower. After pushing above key levels around the Fed meeting yesterday, the euro and sterling have fallen to profit-taking and spurring a broader dollar bounce. The Scandis and dollar-bloc currencies are off 0.5%-1.0%, leading the move today, while the European complex and yen are off 0.15%-0.5%. The liquid and accessible emerging market currencies, like the South African rand, Russian rouble, Mexican peso, are off 1.0%-1.5% and leading the way lower. Gold, too, is lower amid modest profit-taking, but so far, yesterday’s low near $1941 is intact. September WTI is 1% lower and holding a little above this week’s low near $40.50. Outside of Taiwan, Korea, and Australia, equities in the Asia Pacific region and Europe are lower. It is the first back-to-back decline in the MSCI Asia Pacific Index this month, while the Dow Jones Stoxx 600 is lower for the third time this week and the fourth in the past five sessions. US shares are weaker, and the early call is for a nearly 1% drop in the S&P 500. Note that Alphabet, Apple, Facebook, and Amazon, whose officials testified in the House of Representatives yesterday, report earnings later today. |

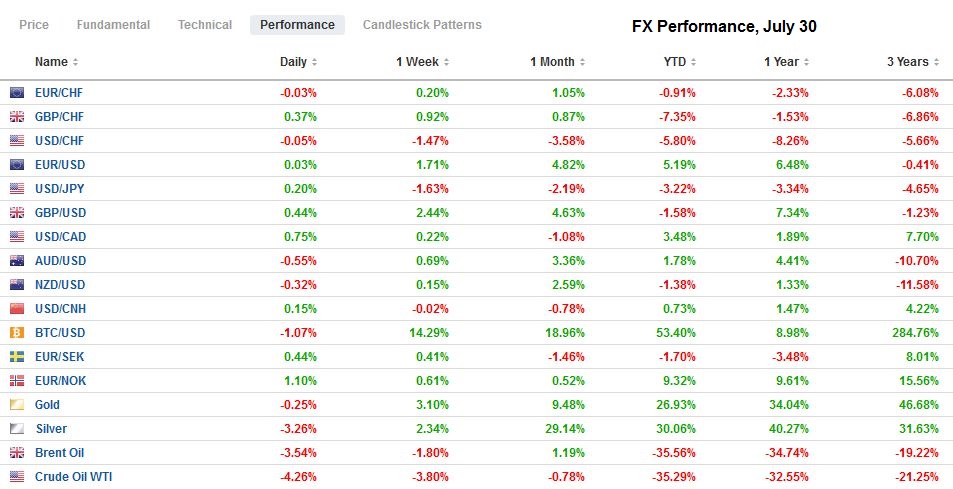

FX Performance, July 30 - Click to enlarge |

Asia Pacific

Japan reported a surge in retail sales in June, the first full month after the state of emergency ended. The 13% jump in retail sales was well above the median forecast in the Bloomberg survey for an 8% rise. The May series was revised to show a 1.9% gain instead of 2.1%. Nevertheless, the year-over-year rate stands at -1.2%. In May, it was 12.3% lower. Tomorrow Japan reports June employment data, and the unemployment rate is expected to creep up to 3.1% from 2.9%. June industrial production is also on tap, and the first rise since January is expected (~1% after falling nearly 9% in May). That would still leave industrial output off by almost a fifth from a year ago.

Australia’s economic data was worse than expected. June building approvals were off 4.9% compared with expectations for a less than a 3% decline. February is the only month in the first half that saw an increase. Separately, Australia’s Q2 terms of trade deteriorated as the export price index fell 2.4%, which was more than expected, and import prices fell by 1.9% compared with an expected decline of 3%. Separately, Bloomberg reported that the government’s projection of $55 a ton for iron ore, its largest export, was around half the prevailing price, which gives upside potential to tax revenue and nominal GDP is prices stay near current levels.

The dollar is snapping a five-day fall against the Japanese yen. It reached almost JPY104.75 yesterday and reached a high near JPY105.30 in Asia. The intraday technicals suggest a push a little higher in North America is likely, and the JPY105.50 offers nearby resistance. There is an option for about $650 mln at JPY105 that will be cut today. The Australian dollar stalled a few hundredths of a cent below $0.7200 yesterday, and profit-taking took it to around $0.7130 to end a four-day advance. The low for the week, set Monday, was a little below $0.7090. The Aussie could be among the first of the majors to stabilize, and a move above $0.7160 would do just that. The PBOC set the dollar’s reference rate a little weaker than the models suggests, but the greenback edged higher for the third consecutive session. Meanwhile, the Hong Kong Monetary Authority was forced to buy US dollars to defend its band. Separately, Hong Kong authorities have made the first arrests under the new controversial security law.

Europe

Germany reported that the world’s fourth-largest economy contracted by 10.1% in Q2, a full percentage point more than economists projected. The details will not be published for a couple of weeks. Its temporary cut in the value-added tax this month appears to be weighing on the state’s CPI reports. The national harmonized figure, due out later today, is expected to show the year-over-year rate may fall from 0.8% to 0.3%. The eurozone’s Q2 GDP and July CPI estimate will be published tomorrow.

The eurozone reported that the bloc’s unemployment rate rose to 7.8% in June. This was a little higher than expected, but the real surprise was the upward revision in May to 7.7% from 7.4%. More currently, Germany reported its July unemployment rate was unchanged at 6.4% as the unemployment queues unexpectedly fell by 18k. Economists had forecast another increase after the 69k increase (initially 68k) in June.

Italy’s narrowly approved the government’s 25 bln euro increase in expenditures, mostly aimed at businesses and local and regional governments. This will lift the deficit by almost 12% this year, from around 10.4% agreed in April. The ECB’s efforts through its own bond-buying and by providing cheap funding to encourage others to do the same have underpinned Italian debt and peripheral European debt more broadly. The 10-year yield today is at a marginal new four-month low. The two-year yield has been below zero for around 10 days.

The euro was sold from a little above $1.18 to about $1.1730. It is trading inside yesterday’s range when it reached a low near $1.1715. As we have noted, the euro’s highs have frequently been made in the US during this part of the rally, and intraday technical indicators suggest it will likely trade higher today. Sterling, in fact, turned higher for the day in the European morning and is extending its rally into a tenth consecutive session. It is trying to establish a foothold above $1.30.

America

The FOMC’s statement offered little new. Rates will remain low, and policy accommodative for some time, and the central bank is prepared to do more if necessary. It stated what will seem obvious to many, and that is that the path of the economy is significantly dependent on the course of the virus. After extended its asset-buying facilities earlier in the week, at yesterday’s FOMC meeting, the swap lines and repo facility with foreign central banks was extended until the end of March 2021. It is more for assurances because as market conditions have normalized, the swaps lines usage has diminished, and it does not look like the repo facility was used in the first place. Yet there is no reason to market’s backstop. There was a hint that more action will be forthcoming in September when the Fed meets again. The Fed says it is prepared to do more, that the virus is on the increase and that it will determine the course of the economy. It seems to simply follow that it will take additional measures. Moreover, Powell indicated that the policy review was nearly done. That would also dovetail nicely with fresh action.

The US reports its first estimate for Q2 GDP, and even though it is subject to statistically significant revisions, its the first release that captures the attention. It is arguably more an issue of curiosity than a source for new investment insight. In some important ways, it is old news. The second quarter is in the rearview mirror, and no doubt it was bad, and exactly how bad it may not matter so much. The Marketwatch and Bloomberg surveys found a median forecast of 34.6% and 34.5% contraction, respectively. The Atlanta and St. Loius Fed GDP trackers are not far from that. That makes the NY Fed’s tracker at -14.3% so eye-catching. Also, underscoring the dated nature of the GDP report, the NY Fed’s “nowcast” model puts the current quarter’s growth at 13.3%, and private-sector forecasts are mostly higher than that. That said, we wonder if a second consecutive increase in weekly initial jobless claims may be more important for the immediate market reaction. It would dovetail with our idea that the dollar bounce is unlikely to be sustained.

Mexico’s economy was in poor shape before the pandemic. Its economy contracted from April through December 2019. The economy shrank by 1.2% in Q1 2020, and output is expected to have fallen by another 16.7% in Q2, according to the median forecast in the Bloomberg survey. That would mean that Mexican output as fallen by a fifth year-over-year. Most manufacturing workers are regarded by government as essential, coupled with re-opening of US auto production, and new domestic content rules under the NAFTA2.0 agreement, Mexican auto output ramped up in June. However, the IMEF surveys for June showed both the manufacturing and non-manufacturing sectors were still contracting. Banxico meets on August 13, with inflation running around 3.5%, the overnight cash target at 5.0%, and stable, having recouped around half of its earlier losses, there is scope for a rate cut.

Oil prices did not react much to news of a much larger expected drawdown in US oil inventories. The 10.6 mln barrel draw was around six times more than the median forecast in the Bloomberg survey, and the largest so far this year. The US stock now stands at around 526 mln barrels, which is about 17% above the five-year average. The reason for the drawdown is also important. It is not because output slowed; it remained stead near 11.1 mln barrels a day. Instead, demand from refiners that jumped their capacity utilization rose by 1.6 percentage points to about 79.5%. However, this may not be sustainable as there are already concerns about a glut in gasoline and distillates.

The US dollar held above the CAD1.3315 June low after several attempts to punch through it. The bounce lifted the greenback to around CAD1.3425. The week’s high so far is just a bit above around CAD1.3425. However, the intraday technical indicators suggest the path of least resistance now is back down for the US dollar. A move back to the CAD1.3360 area seems reasonable in North America today. The US dollar closed below MXN22.00 in the first three sessions this week but maybe challenged to do so again today. The greenback rose to almost MXN22.25 in the European morning, stopping shy of the week’s high set Monday near MXN22.3265. The intraday technicals favor a dollar pullback. Initial support may be seen a little above MXN22.00.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Currency Movement,Featured,federal-reserve,Italy,Mexico,newsletter