Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

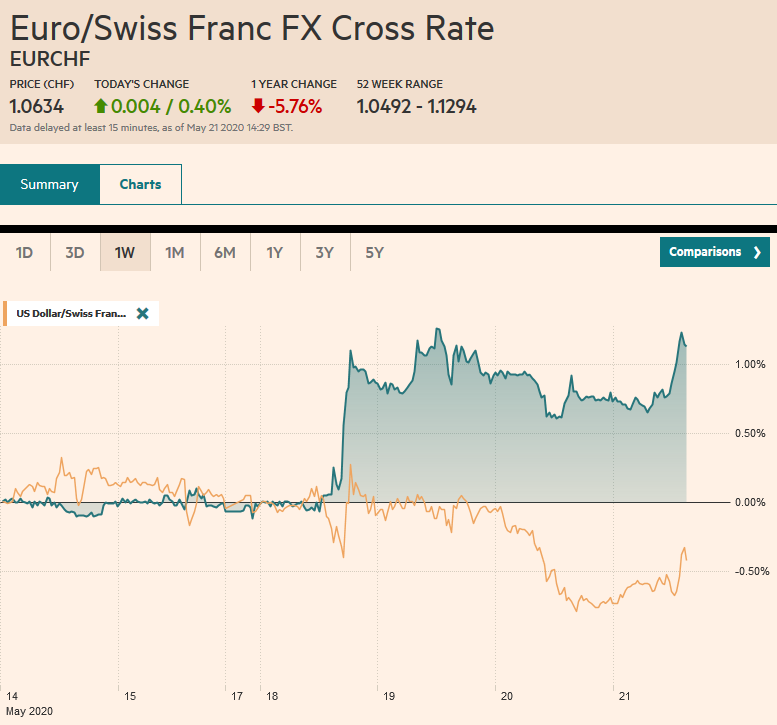

Swiss FrancThe Euro has risen by 0.40% to 1.0634 |

EUR/CHF and USD/CHF, May 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: New two and a half month highs in the S&P 500 yesterday failed to have much sway in the Asia Pacific region and Europe today as US-China tensions escalate and profit-taking set in. Perhaps it is a bit of “buy the rumor sell the fact” type of activity on the back of upticks in the preliminary PMI reading and hesitancy about pushing for what appeared to be breakouts. The MSCI Asia Pacific Index snapped a four-day advance, although India and Taiwanese shares were bought. Europe has been chopping back and forth since surging 4%+ on Monday. It is off almost 0.65% in late morning turnover in Europe. US shares are heavy, and the early call sees the S&P 500 giving back a little more than half of yesterday’s nearly 1.7% gain. Benchmark yields are mixed, and the US 10-year is in its well-worn range around 66 bp. The dollar is higher against all the majors, while the emerging market currencies are mixed. South Africa and Turkey, which are expected to deliver 50 bp rate cuts, are seeing their currencies trade with a heavier bias. Gold is weaker amid some profit-taking after unable to close above $1750 for the past four sessions. Support is seen near $1725. Meanwhile, July WTI is extending its rally for the sixth consecutive session as it pushes above $34 a barrel. It finished last week near $29.50. |

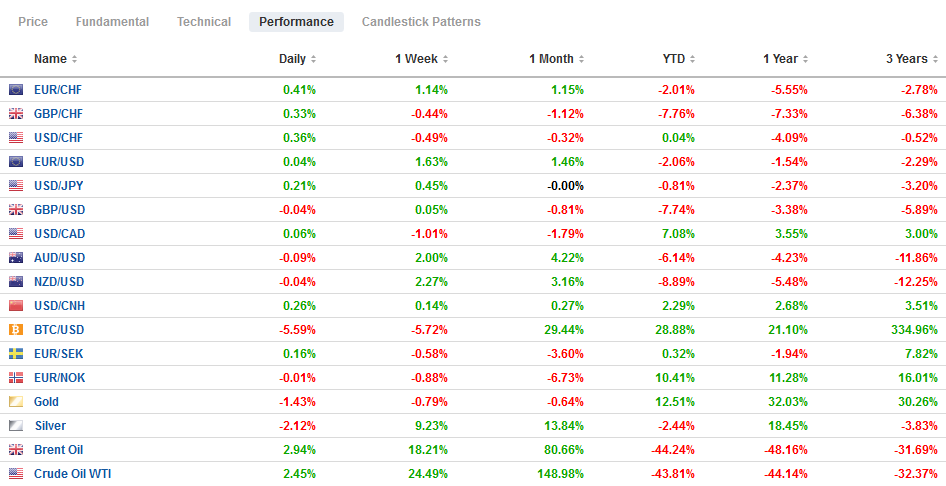

FX Performance, May 21 - Click to enlarge |

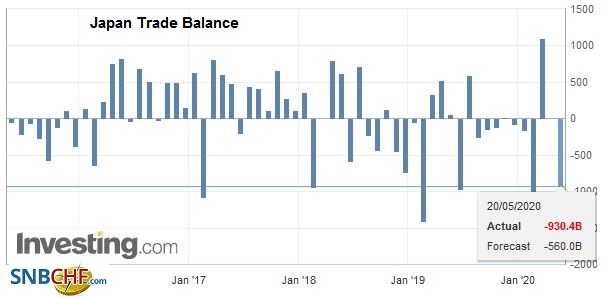

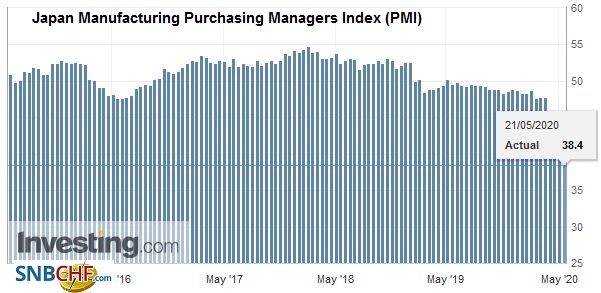

Asia PacificThe Japanese and Australian preliminary PMIs showed a nascent recovery in services while manufacturing remained under pressure. And this seemed to also be picked up by weakness in the latest Japanese and South Korean export figures. |

Japan Trade Balance, April 2020(see more posts on Japan Trade Balance, ) Source: investing.com - Click to enlarge |

| First, the PMIs. In Japan, manufacturing slipped to 38.4 from 41.9, while services rose to 25.3 form 21.5. This translated into a 27.4 composite from 25.8. In Australia, the manufacturing PMI eased to 42.8 from 44.1. Services rose to 25.5 from 19.5. The composite rose to 26.4 from 21.7. |

Japan Manufacturing Purchasing Managers Index (PMI), May 2020(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

Let’s look at the trade figures next. April exports from Japan fell 21.9% year-over-year. This was in line with expectations after an 11.7% decline in March. Imports fell 7%, which was shallower than expected after a 5% decline in March. Japan recorded a JPY930 bln deficit. It is the fifth deficit in the past six months. South Korea’s trade figures have begun improving. In the first 20 days of May, exports fell 20.3%, moderating from a 24.3% decline in April. Exports of semiconductor chips from 13.4%, while autos were off 58.6%, mobile devices fell 11.2%, and oil products were down almost 69%. In terms of destinations, exports to the US were off 27.9% and 18.4% to the EU and down 22.4% to Japan. Exports to China were off only 1.7% from a year ago.

This month’s up trendline for the dollar is seen near JPY107.35 today. It has not been below JPY107.50 today. On the upside, although frayed earlier this week, the JPY108 area still offers resistance and the 200-day moving average is near JPY108.30. The dollar has not been above JPY107.85 today, and there is a roughly $465 mln option at JPY107.69 that expires today. The Australian dollar began the week near $0.6400 and was probing $0.6600 yesterday, the highest since early March. It found initial support today around $0.6550, and there is additional chart support by $0.6525. The PBOC set the dollar’s reference rate a little lower than the bank models suggested, but the greenback edged higher. It continues to trade in a narrow range around CNY7.10, which is the upper end of the broader two-month trading range.

EuropeA similar pattern to Australia and Japan was seen in the preliminary European PMI: namely a better showing and a stronger pick up in services than manufacturing. |

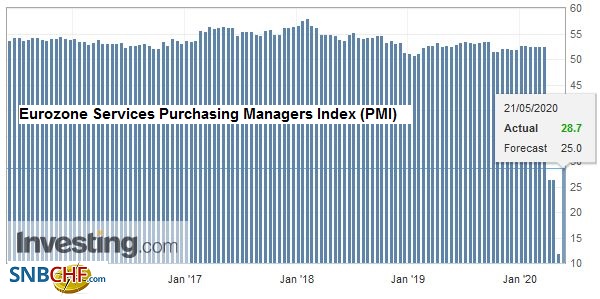

Eurozone Services Purchasing Managers Index (PMI), May 2020(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

| In France, manufacturing rose to 40.3 from 32.5, while the service PMI rose to 29.4 from 10.2. These translate into a 30.5 composite reading compared with 11.1 in April. |

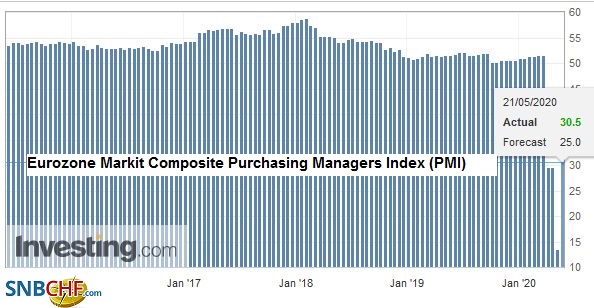

Eurozone Markit Composite Purchasing Managers Index (PMI), May 2020(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

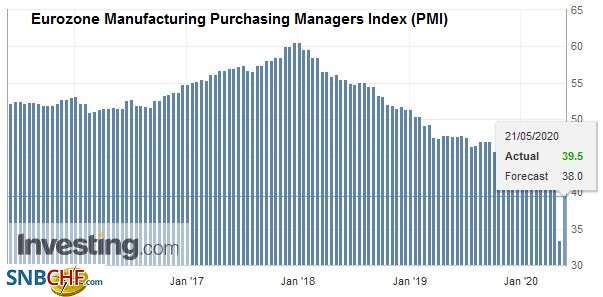

| For the eurozone as a whole, Markit estimates the manufacturing component rose to 39.5 from 33.4, and the services PMI rose to 28.7 from 12.0. The composite sits at 30, up from 13.6. |

Eurozone Manufacturing Purchasing Managers Index (PMI), May 2020(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

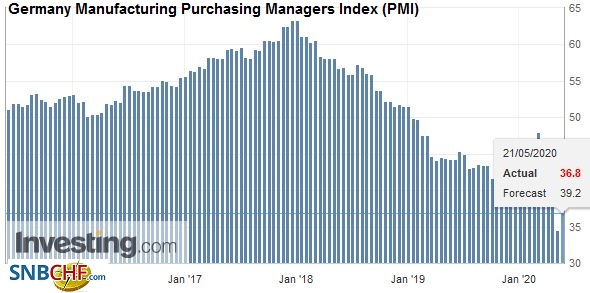

| German manufacturing PMI rose to 36.8 from 34.5, while the service PMI rose to 31.4 from 16.2. The composite was lifted to 31.4 from 17.4. |

Germany Manufacturing Purchasing Managers Index (PMI), May 2020(see more posts on Germany Manufacturing PMI, ) Source: investing.com - Click to enlarge |

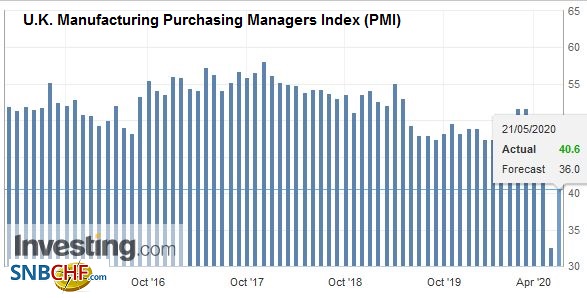

| The UK’s preliminary figures were also consistent with this broad pattern. Manufacturing PMI rose to 40.6 from 32.6, |

U.K. Manufacturing Purchasing Managers Index (PMI), May 2020(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| while the services PMI increased to 27.8 from 13.4. The composite is at 28.9 after a 13.8 reading in April. |

U.K. Services Purchasing Managers Index (PMI), May 2020(see more posts on U.K. Services PMI, ) Source: investing.com - Click to enlarge |

The reports lend credence to the idea that the worst for the regional economy is likely passed. To be clear, a sub-50 reading on the PMI shows contractions continue, but the turning of the “second derivative” is the first sign of the bottom. Moreover, many areas remained shut down in whole or part when the surveys were conducted between May 12 and May 20. This seems to set the stage for stronger readings in June.

After a couple of Bank of England members explicitly said that negative interest rates were among the policies being considered, the new Governor seemed to soften his stance. Bailey acknowledged his position had modified and that there was no need to rule out anything. Shortly before that, the UK auctioned its first note that had a negative yield. It sold GBP3.75 bln of a three-year Gilt with an implied yield of -0.003%. The auction was oversubscribed (2.15x) but by the lowest amount in two months. The Bank of England meets again on June 18. The odds still favor an increase in asset purchases before negative rates come into play. Neither the short-sterling futures strip or the rest of the yield curve (outside the 2-3 year Gilt) are implying negative rates. Sterling has stabilized after falling by about 4.5% against the dollar in the month through the start of the week.

Banks took about 850 mln euros from the ECB’s first Pandemic Emergency Long-Term Refinance Operation. These loans were for minus 25 bp. It was disappointingly light and will likely fan speculation of easier terms perhaps as early as the June 4 ECB meeting. In terms of these long-term loans, the one to watch is the June 18 offering, which will be the first that could be at a minus 100 bp yield if specific lending criteria are met. Moreover, other such loans will be rolled into this more attractive option. It could be a trillion euro.

The euro was stopped 1/100 of a penny shy of the $1.10 level yesterday and is consolidating lower today. It spent little time above $1.0980 in Asia and eased to about $1.0950. Support is seen in the $1.0920-$1.0940 band. A break below $1.09 would disappoint the bulls. Sterling tested a three-day low near $1.2185 today, which is about the middle of this week’s range. The high for the week was set on Tuesday, 4/100 of a cent below $1.23. The price action of both the euro and sterling is a timely reminder of the psychological significance of round numbers, and stops should be placed accordingly. Sterling rebounded toward $1.2240 in the European morning but appears set to run out of steam near there.

America

The US has stepped up its pressure on China. The rhetoric over the virus, Taiwan, the kidnapping of Panchen Lama (1995), and China’s military and economic policies has escalated in recent days. But it is not all about rhetoric. The US Senate passed a bipartisan bill yesterday that requires Chinese companies listed in the US to affirm that they are not under the control of the government. This could impact large Chinese companies, like Alibaba and Baidu, both of whom sold off late yesterday in response to the bill. A separate bill that authorizes the President to levy sanctions on individuals for the mistreat of minorities in China is also progressing through the legislative process. Soon, the US Treasury report on the currency market is expected, and more importantly, the US State Department has to affirm that Hong Kong remains autonomous, or the SAR will lose its special trade privileges with the US.

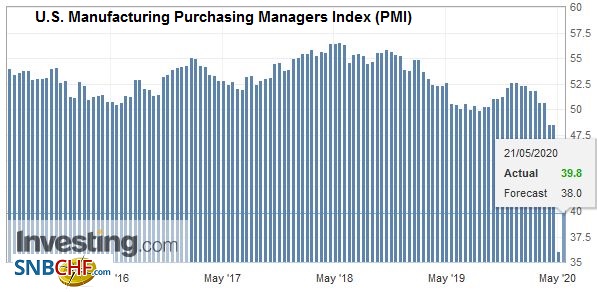

| The US reports the weekly jobless claims, which are expected to have remained elevated at or over 2 mln. The Philadelphia Fed survey for May (expected rise to around -40 from -56.6) and the preliminary PMI (both manufacturing and services are expected to increase and lift the composite from the 27.0 reading in April) are the highlights. The April index of Leading Economic Indicators and existing home sales are overshadowed by May data. Canada and Mexico have light calendars today, but both report March retail sales tomorrow. |

U.S. Manufacturing Purchasing Managers Index (PMI), May 2020(see more posts on U.S. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The US sold 20-year bonds for the first time since 1986 yesterday. It paid 1.22% to borrow $20 bln. The bid-cover was 2.53, and indirect bidders, which include foreign central banks and some asset managers, took almost 61%. There is not much available in that duration area, and what there is the Federal Reserve appears to have bought nearly to their 70% individual issue cap. Separately, the FOMC minutes from last month’s meeting were published, and little new ground was unearthed. There seemed to be an agreement that if things got worse, apparently from their base case for a recovery in H2, more fiscal stimulus was needed, and there was more that the Fed could do. Yield curve control remains a possibility. No official discussion of negative interest rates was recorded. The possibility of tweaking interest on reserves, which some, including myself, played up, seems less likely now. The Fed reported that there was little concern that the fed funds rate would fall below target.

The US dollar is trading within yesterday’s range against the Canadian dollar, which was inside Tuesday’s range. The CAD1.3900-CAD1.3950 range so far today is likely to be extended, and the intraday technical readings suggest higher. The recent price action reinforced the lower end of the six-week range near CAD1.3850. A move above CAD1.4000-CAD1.4020 is needed to lift the greenback’s tone. The US dollar finished last week a little above CAD1.4100. The greenback fell 1.8% against the Mexican peso yesterday, the third consecutive decline, and the most in roughly three weeks. It found support just above MXN23.00, the dollar’s lowest level since late March. A push above MXN23.30 now would suggest a near-term low is in place with the next resistance near MXN23.50.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,Cold War,EUR/CHF,Eurozone Manufacturing PMI,Eurozone Markit Composite PMI,Eurozone Services PMI,federal-reserve,Germany Manufacturing PMI,Japan Manufacturing PMI,Japan Trade Balance,negative rates,newsletter,Trade,U.K. Manufacturing PMI,U.K. Services PMI,U.S. Manufacturing PMI,USD/CHF