Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.11% to 1.054 |

EUR/CHF and USD/CHF, May 04(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The constructive mood among investors in April has given way to new concerns as May gets underway. Japan and China are still on holiday, but most of the other markets in Asia fell, led by 4.5%-5.5% declines in Hong Kong and India, and more than 2% in most other local markets. Australia bucked the trend a gained 1.4% after shedding 5% before the weekend. Europe’s Dow Jones Stoxx 600 is off almost 2.5% in late morning turnover, while US shares are pointing to another gap lower opening in the S&P 500. Outside of Sweden and the UK, European benchmark 10-year yields are firmer, with the peripheral yields 4-6 bp higher. The US 10-year yield softer at 60 bp. The dollar is stronger against nearly all the currencies, with the Japanese yen is the sole major exception. At the same time, the JP Morgan Emerging Market Currency Index is lower for the third consecutive session. Gold is straddling $1700 an ounce, while oil is snapping a three-day advance as is back near $18 after flirting with $20 a barrel at the end of last week. |

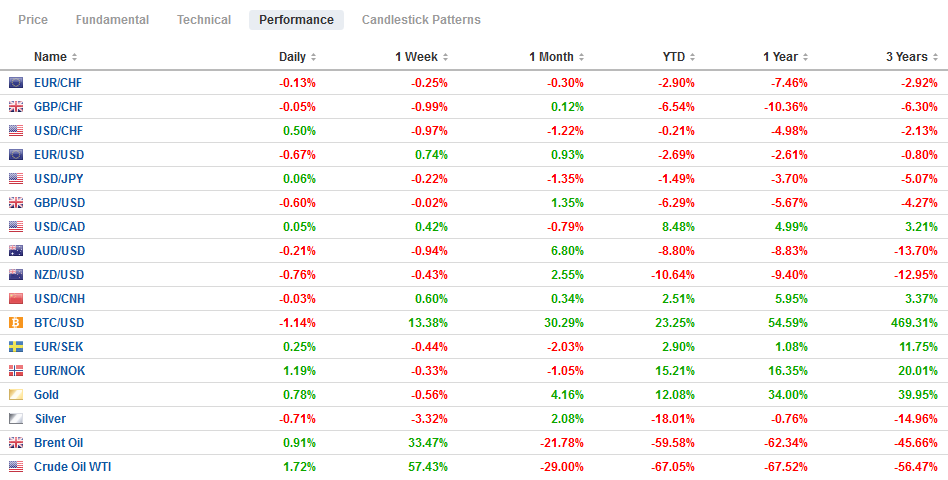

FX Performance, May 4 - Click to enlarge |

Asia Pacific

The US has gone on an offensive against China. The Washington Post reported last week that several options are under consideration, though Kudlow denied that reneging on its debt is not one of them. Ahead of the weekend, explicitly did not rule out new tariffs over the coronavirus, which the US intelligence community, according to the Office of the Director of National Intelligence, concurs with numerous scientists who conclude that Covid-19 was not man-made or genetically-altered. Exactly how people were first exposed to it remains unknown. Meanwhile, Mitt Romney had written a broad critique of China in a recent op-ed piece, and Pete Buttigieg penned a piece claiming Beijing prefers Trump over Biden as a counter to Trump’s claims. There hardening of the US position toward China is bipartisan. Ahead of the weekend, in another exercise of diplomacy via twitter, the US Mission to the UN tweeted that barring Taiwan “from setting foot on the UN grounds is an affront not just to the proud Taiwanese people but to UN principles.” It was re-tweeted by the US Ambassador Craft. The tweet does not necessarily contradict the US one-China policy that has been affirmed several times, but it brought a quick and sharp rebuttal by China’s mission to the UN.

South Korea’s manufacturing PMI fell to 41.6 in April from 44.2 in March. The re-opening of China did not do it much good yet. Separately, it reported its headline CPI fell to 0.1% in April from 1.0% in March, illustrating the powerful deflationary forces that have been unleashed. Taiwan’s manufacturing PMI fell to 42.2 from 50.4.

The Reserve Bank of Australia meets tomorrow, and the cash rate is already near the zero-bound. As markets stabilized, the RBA has scaled back its bond purchases. The RBA has bought about A$50 bln of federal and state government bonds. It is also the first country outside of Japan that has adopted a yield-curve-control strategy and targets the 3-year yield at 0.25 bp, the same as the cash rate. At the end of the week, the central bank will update its economic forecasts.

On April 30, the dollar traded between about JPY106.40 and JPY107.50. This remains the range. The greenback has been unable to resurface above JPY107 today. It has also held above the pre-weekend low of about JPY106.60. The Australian dollar peaked on April 30, near $0.6570. It is down for the third session and tested the $0.6375 support area. The session high was seen in late Asia around $0.6425. However, this seems to have provided a new selling opportunity. A convincing break of support could target the $0.6250 area. The dollar surged to CNH7.1560 against the offshore yuan, its highest level since mid-March. However, it staged a downside reversal and fell to CNH7.1245 in early Europe. It was near CNH7.0820 when the mainland markets closed for the extended holiday.

EuropeThe EMU flash manufacturing PMI was revised lower to 33.4 from 33.6. It was at 44.5 in March. The revisions stem from weaker Italian and Spanish reports. Italy fell to 31.1 from 40.3, while Spain’s manufacturing PMI fell to 30.8 from 45.7. |

Eurozone Manufacturing Purchasing Managers Index (PMI), April 2020(see more posts on Eurozone Manufacturing Purchasing Managers Index, ) Source: investing.com - Click to enlarge |

| Germany’s final reading ticked up to 34.5 from 34.4 and France flash reading was left unchanged at 31.5 |

Germany Manufacturing Purchasing Managers Index (PMI), April 2020 Source: investing.com - Click to enlarge |

Tomorrow, the German High Court will issue its final verdict on the ECB’s Public Sector Purchase Progam (PSPP). Previously, it asked the EU Court of Justice to rule if QE violated the prohibition against monetary financing of debt or if the purchase outside monetary policy. On both questions, the Court of Justice ruled in the ECB’s favor. The German High Court could still put limits on the Bundesbank’s participation or raise new questions that would invite challenges to the Bundesbank’s participation in the Pandemic Emergency Purchase Progam, which does not adhere to the capital key. Any ruling that is not a reaffirmation of the Court of Justice would likely spur euro selling.

The UK talks with the EU on a new trade relationship are fraught with difficulties. If some meaningful progress is not made by the end of next month, UK Prime Minister Johnson has threatened to abandon the talks altogether. Separately, discussions between the UK and the US on a trade agreement begin this week. Although US President Trump encouraged the UK to leave the EU and promised a quick trade agreement, this is where the rubber meets the road of America First. In trade disputes with the EU, the US has not made special allowances for the UK.

The euro briefly traded above $1.10 before the weekend but has been unable to retest it today. Instead, it has been sold through low near $1.0935. There is an option for one billion euros that expires today at $1.0955, and that area may cap in early North American turnover. Initial support now is seen near $1.0915 and then $1.0880. Another expiring option (~725 mln euros) at $1.0870, but it seems unlikely to come into play. Sterling reached a high last week of about $1.2645. It reached $1.2415 in the European morning. A break of $1.2400 could spur another leg lower.

America

The US reports March factory orders and the final durable goods orders report. Outside of the headline risk, the data is unlikely to have much impact. With last week’s release of Q1 GDP (-4.8% annualized rate), the data from the first part of the year has lost its attraction. The highlight of the week is the jobs data, which are expected to show a loss of more than 21 mln jobs and a jump in the unemployment rate from 4.4% to possibly as high as 16.5%. Meanwhile, the Federal Reserve has announced that it would further taper the Treasury buying to $8 bln a day (down from $10 bln a day last week). The refunding announcement in the middle of the week is expected to see an increase in the size of the offering as well as the re-introduction of a 20-year issue. Another spending bill is being negotiated. Trump is pushing for a payroll saving tax cut, and the head of the Senate was some business protection against lawsuits as they re-open, while the House is seeking around $1 trillion for aid for states and local governments.

Prime Minister Trudeau announced former deputy governor Tiff Mackem was going to return to the central bank to succeed Polz, whose term ends early next month. Mackem was there during the Great Financial Crisis, and some suggest this tipped the scales in his favor over Wilkins, a current deputy. Many accounts attributed the selling pressure on the Canadian dollar ahead of the weekend to comments by Mackem that negative interest rate was among the unorthodox options. Still, he immediately indicated that is was not deployed because of the disruptive effects, and showed he was not in favor of adding another disruption to the mix. While it is possible that some algos or computerized selling was triggered by the mere mention of “negative rates,” we suspect the unwinding of risk appetites (sell-off in stocks) was a more important driver.

OPEC+ output cuts went into effect at the end of last week, but there were some signs that several producers had already begun cutting back, including Saudi Arabia. In the US, the three large exploration/production corporations (Exxon, Mobil, and Chevron) will have announced plans to cut 660k barrels a day by the end of June. Nearly a third of North Dakota’s output has been shuttered, and production in the US has already fallen about a million barrels a day since mid-March. The US oil rig counted peak in mid-March at 683. The 14% (53 rigs) decline last week brings the total down to 325 rigs, and this week it is likely to fall through the 2016 low of 316. The Kansas Federal Reserve estimates that 40% of the US oil and natural gas producers will face insolvency if WTI remains below $30 a barrel. The first futures contract that is trading above $30 is March 2021. Moody’s assigned Saudi Arabia a negative outlook to its A1 (A+) rating ahead of the weekend. Moody’s rating is still ahead of Fitch (A)and S&P (A-). Saudi Arabia drew down about 5% of its reserves in March and Moody’s projects a 12% fiscal deficit this year from 4.5% in 2019. The Saudi stock market fell nearly 7.5% on Sunday and is up about 1.3% today.

The Canadian dollar is under pressure for the third consecutive session. It made a marginal new high for the month on April 30 but has sold off as the risk-appetites have shifted. The US dollar bottomed last week near CAD1.3850 and tested CAD1.4150 today. It found support near CAD1.4100 in the European morning, but the intraday technicals warn that another run at the highs is likely in North America today. There is not much chart resistance ahead of the CAD1.4260 area. Mexico reports its April PMI, and there is little doubt the direction of the data and economy. Worker remittances are an important source of hard currency revenues. In March 2019, it was a little less than $3 bln. In March 2020, it is projected to have fallen toward $2.27 bln. In January and February, it was still above the year-ago comparisons. The risk-off move has lifted the greenback toward MXN24.89. It has traded a handful of times above MXN25.00 in March and April but has not yet secured a solid foothold above it, but that is the direction we think things are moving.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Canada,China,Currency Movement,EUR/CHF,Eurozone Manufacturing Purchasing Managers Index,Germany,newsletter,RBA,U.K.,USD/CHF