Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

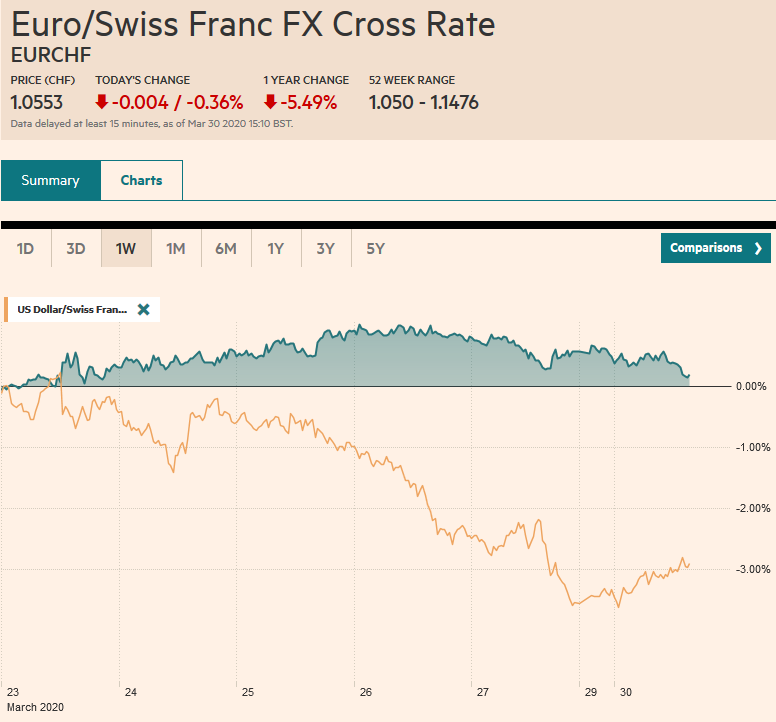

Swiss FrancThe Euro has fallen by 0.36% to 1.0553 |

EUR/CHF and USD/CHF, March 30(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

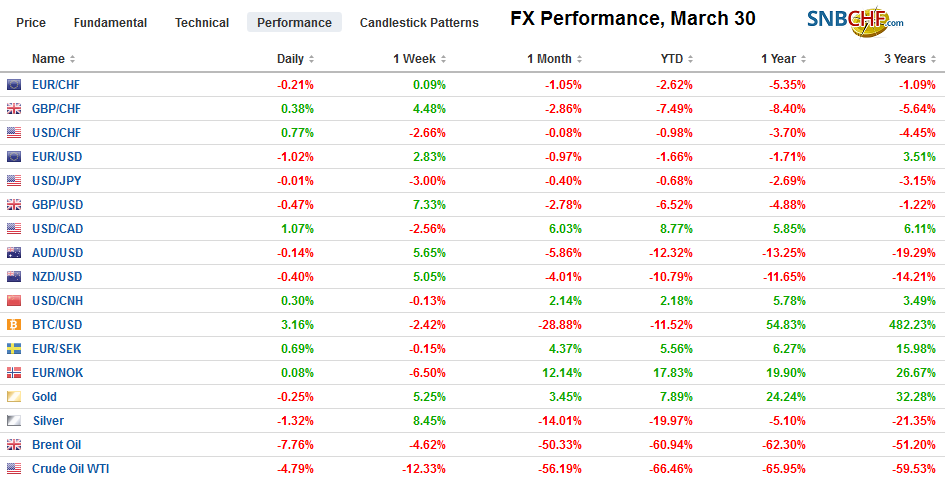

FX RatesOverview: Risk appetites remain in check as the spread of the coronavirus is leading to more and longer shutdowns. Asia Pacific equities fell with Australia, the notable exception. Its benchmark rallied a record 7%, encouraged by additional stimulus measures. Led by financials, following new that the ECB is requesting banks hold off dividend payments until October (which frees up an estimated 30 bln euros), real estate, and consumer discretionary sectors, the Dow Jones Stoxx 600 is off by a little more than 0.5% in late morning turnover. US shares are flat to slightly higher. Benchmark 10-year yields are mostly lower, led here too by Australia’s 14 bp decline (to about 75 bp). The UK Gilt market shows little response to the pre-weekend downgrade, and the 10-year yield is off eight basis points, the most in Europe. Core European yields are 3-6 bp lower, while Italy’s 10-year yield is about nine basis points higher. The US benchmark yield is off four basis points near 0.63%. The dollar is firm against most major currencies, but the Japanese yen, and most emerging market currencies, but a small handful of Asian currencies, including the Chinese yuan. The South African rand is off a little more than 1%, and the 10-year yield is up about 12 bp (~11.70%) following the pre-weekend downgrade by Moody’s to below investment grade. Now all three of the major rating agencies have taken away its investment-grade status. Gold is softer alongside equities, while May WTI briefly dipped below $20 a barrel. |

FX Performance, March 30 - Click to enlarge |

Asia Pacific

Japan is putting together extra budget days after the budget for the new fiscal year, starting April 1, was approved. The news measures are expected by the middle of next week. It will be funded by as much as JPY16 trillion in new debt, on top of the JPY129 trillion in the FY20 budget. The new bond issuance will be across the maturities, except for the 40-year bond and inflation-protected securities.

The PBOC injected CNY50 bln (~$7 bln) into the banking system via what it calls seven-day reverse repos (which is an injection of cash for securities that will be unwound in seven days) at 20 bp lower rate to 2.2%. Many observers see this as a prelude to a substantial cut in the benchmark one-year Loan Prime Rate (set via a survey of banks on the 20th of every month). The PBOC defied expectations and left the LPR unchanged ten days ago. Separately, the PBOC continued to set the dollar’s reference rate weaker than the bank models suggest. Today’s reference rate was set at CNY7.0447, while the median bank model (according to Bloomberg) was CNY7.0522.

Singapore eased monetary policy, as it does through its exchange rate guidance. Earlier today, the Monetary Authority of Singapore lowered the midpoint of its currency band and brought the slope to zero. The clear implication is that MAS is accepting a weaker currency. The move was not unexpected following last week’s news that the economy contracted more than 10% quarter-over-quarter in Q1, and the government unveiled a second stimulus package (SGD48 bln or ~$33.5 bln).

The dollar eased to around JPY107.10 in the Asian session after finishing last week just below JPY108.00. The JPY107.70 area corresponded to a (38.2%) retracement of the rally from the March 9 low near JPY101.20 to the recent high of about JPY111.70. The next retracement (50%) is found near JPY106.45. The session high was set in early Europe around JPY108.25. Resistance is seen by JPY109.00. The Australian dollar is trading in the upper end of its pre-weekend range and has not been bid through $0.6200, where the 20-day moving average is found. In both Asia and early Europe, support near $0.6115 held.

Europe

Reports suggest that 14 of the 19 eurozone members endorse a common intergovernmental bond to finance expenditures linked to the coronavirus. This is an issue that will not be decided by a majority or a qualified majority. It a decision that requires unanimity, and it will not be forthcoming. Many of the same people, institutions, and countries that sought a joint bond in the sovereign debt crisis a decade ago are pushing for it again, but the creditors remain unconvinced. The European Stabilization Mechanism (ESM) and the European Investment Bank (EIB) issue bonds for which there is a shared responsibility. It is not clear what specific problem a new joint bond would address besides being seized upon as an opportunity to advance the federalist agenda. A compelling case would have to entail a demonstration, not merely an assertion that monetary union itself is at risk and that a joint bond is the only solution. It still seems to be a “nice-to-have” rather than a “must-have.”

Fitch cut the UK’s sovereign rating before the weekend to AA- with a negative outlook. It cited the deterioration in the UK’s finances, as the budget deficit looks three-times larger than it did a month ago. Fitch also cited uncertainty over the post-Brexit trade arrangement It seems increasingly likely that the negotiations of this new arrangement, which already had seemed rushed prior to the virus outbreak, will have to be extended beyond year-end. Although Fitch was is now the lowest of the three major rating agencies (S&P AA+ and Moody’s Aa2 is the equivalent of AA), the markets did not seem to respond much.

The euro initially extended last week’s gains, rising to almost $1.1165 before grinding lower to about $1.1060, its 20-day moving average, where it languishes in the European morning. An option, set to expire today, for roughly 830 mln euro is struck there ($1.1063) too. Below there, nearby support is seen around $1.1040. Sterling is also confined to a relatively narrow range in the upper end of the range seen before the weekend. The high, just above $1.2465, was set in early Asia, while the low, a little below $1.2320, was just before European markets opened. The 20-day moving average is found near $1.2335. The next support area is seen a cent lower.

America

Just like the debate about a common bond in Europe is reiterating a debate from a decade ago, in the US debate about the extensive encroachment of the Federal Reserve into the capital markets and implications of a large deficit on prices are being recycled. In addition to the sectors the Fed supported in 2008-2009, it has added local government debt and corporate debt, and soon, small and medium-sized businesses. The purists bemoan the sanctity of markets is being violated, but the assistance is not permanent even though it is open-ended. A smooth transmission of the Fed’s monetary policy is the goal, and if the markets cannot or will not do it, officials step into the breach. When the emergency is over, the Fed will withdraw again. It seems unnecessarily alarmist to claim permanent damage is being inflicted.

At the same time, some observers see news of the $2.2 trillion stimulus bill and worry that it will buy a whole lot of inflation. This, too, seems misplaced, like it was in 2008 and 2009. One cannot simply deduce inflation from the size of the fiscal position. Powerful deflationary forces have been unleashed. Capital and labor are being unemployed. The output gap, however measured, is widening. The price of oil has collapsed by roughly 75% since the start of this year, around 50% this month alone. This is not the stuff that generates an increase in the price level. The money that will be received by middle and lower-income households likely will be used service debts and replenish savings. Meanwhile, the ink on the bills is hardly dry, and plans for another package are being discussed that would strengthen workplace protections and provide more funds to the states.

The drop in oil prices and the risk-off mood sees the Canadian dollar pare last week’s gains. The Loonie has finished firmly even after the Bank of Canada signaled a 50 bp rate cut (to bring its overnight target to the zero-bound, 25 bp, and announced a formal asset purchase plan). Its four-day advance is being snapped today. Thus far, the US dollar is trading within the pre-weekend range of roughly CAD1.3920 and CAD1.4155. It looks poised to test the upper end of that range in North America today. The US dollar traded higher after reaching MXN22.85 last Friday and settled a little above MN23.34. It reached almost MXN23.77 today. The MXN23.84 area corresponds to a (38.2%) retracement objective of last week’s pullback. The next retracement (50%) is near MXN24.15.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Currency Movement,EMU,EUR/CHF,newsletter,Singapore,South Africa,USD/CHF