Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has risen by 0.05% to 1.0994 |

EUR/CHF and USD/CHF, November 5(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The prospects that the US-China deal could include some rolling back of existing US tariffs helped underpin risk appetites. After new record highs in the US S&P 500 and NASDAQ, Asia Pacific markets marched higher, and the MSCI Asia Pacific reached its highest level since August 2018. A small rate cut by China and catch-up by Tokyo, which was on holiday on Monday, helped extended the regional rally for the 14th session in the past 17. India, on the other hand, was an exception, and its minor loss snapped a seven-day advance. Europe’s Dow Jones Stoxx 600 is little changed but made a marginal new three-year high. US shares are trading with a firmer bias in the European morning. Bond yields continue to back up, with most 2-5 bp higher. Of note, at minus 32 bp, the 10-year German Bund yield is at its highest level in more than three months, and the Italian benchmark is above 1%. China is the main exception. The 10-year bond yield eased five basis points, which reflects the entire magnitude of the 1-year rate cut today. In the foreign exchange market, the major currencies that tend to do better in risk-on environments, like the dollar-bloc and Scandis are leading the way higher today, while the so-called safe havens, such as the yen and Swiss franc are under modest pressure. |

FX Performance, November 5 - Click to enlarge |

Asia PacificChina’s Caixin services PMI was slipped to 51.1 from 51.3, a new eight-month low. The composite edged up to 52.0 from 51.9 due to the unexpected increase in the manufacturing PMI previously report. The PBOC announced a five basis point cut in 1-year MLF to 3.25%. It is the first cut in this facility in three years. Separately, despite setting the dollar’s reference rate a little higher than the models suggested, the upside pressure on the currency remains. The dollar fell through CNY7.0 for the first time since early August. |

China Caixin Services Purchasing Managers Index (PMI), October 2019(see more posts on China Caixin Services PMI, ) Source: investing.com - Click to enlarge |

The Reserve Bank of Australia left rates on hold (cash rate at 75 bp) as widely expected. The RBA confirmed what the market already knew: rates would remain low for an extended period of time. It did underscore the importance of consumer spending, where labor income is the main fuel. Many still look for the RBA to cut rates next year.

India made it official. After dragging its feet and playing obstructionist, India formally dropped out of the region’s China-led trade-bloc (Regional Comprehensive Economic Partnership). It is parallel bloc to the Trans-Pacific Partnership, and the trade agreement does not appear as extensive. Ultimately, India pulled out for similar reasons that the US withdrew from the TPP. It did not fit into the domestic agenda of the government.

The dollar dipped below JPY108 at the end of last week, but recovered yesterday and is extending those upticks today has nearly returned to JPY109, where the 200-day moving average is found (~JPY109.05). Last week’s high was recorded around the FOMC announcement (~JPY109.30). There does not seem to be the near-term optionality around JPY109 that may have helped stymie last week’s assault. The Australian dollar is firm within its recent ranges. A move above $0.6930 targets the $0.6950-$0.6955 area. There are options for A$1.5 bln struck between $0.6900 and $0.6905, which expire today.

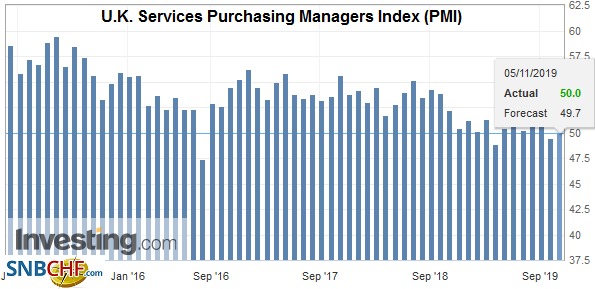

EuropeAhead of tomorrow’s service and composite PMIs for the eurozone, the UK remains the main focus today. Here electioneering and the new speaker are the talking points. The UK reported slightly better than expected service and composite PMIs. Both reached the 50 boom/bust level from 49.5 and 49.3, respectively. |

U.K. Services Purchasing Managers Index (PMI), October 2019(see more posts on U.K. Services PMI, ) Source: investing.com - Click to enlarge |

| Perhaps the less noted development was the continued build in BOE reserves. In October, reserves rose by $2.2 bln. Through the first ten months of the year, UK reserves have risen by an average of $1.53 bln a month. Last year reserves rose by an average that was half as much (~$721 mln). |

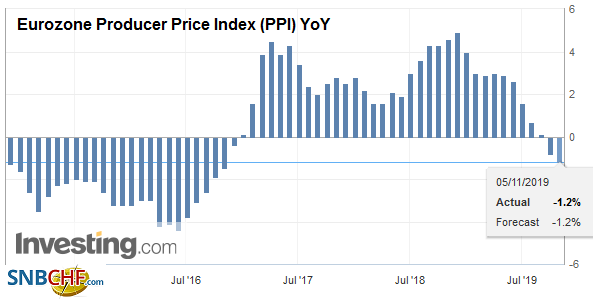

Eurozone Producer Price Index (PPI) YoY, September 2019(see more posts on Eurozone Producer Price Index, ) Source: investing.com - Click to enlarge |

The minutes from Sweden’s Riksbank meeting late last month was slightly more dovish than the initial statement suggested. The minutes acknowledged that the economic and inflation outlook lacked clarity. It still suggested it would hike rates to zero in December. However, it seemed to imply there is no commitment after that. No country that has adopted negative interest rates has been able to emerge so far. Meanwhile, the Swedish economy is weakening. The October composite PMI fell to 48.6, a new six-year low. Separately, industrial orders fell in September by 0.2% and have not risen since May.

After reversing lower yesterday, the euro’s losses were extended a little through $1.1115 in early Asia and recovered toward $1.1140 by the start of the European session. Important resistance is seen in the $1.1175-$1.1180 area, and if it cannot be surmounted shortly, building corrective pressures will express themselves. A break of the 20-day moving average, just below $1.1100, would be the first indication. Sterling has mostly been confined to a quarter of a cent below $1.29. There are chunky options fro GBP1.75 bln between $1.2890 and $1.2900 that expire today. There is another option for about GBP750 mln at $1.2950 that will also be cut today.

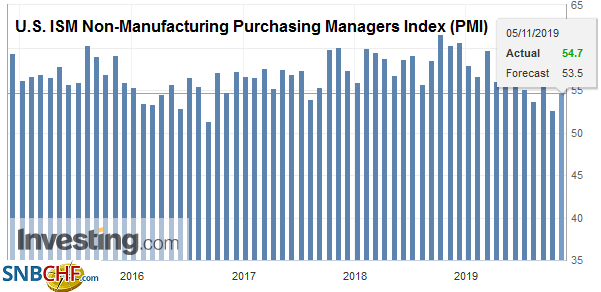

AmericaReports indicate that phase 1 of the US-China trade, which the Trump Administration had previously announced was in the bag, has a new wrinkle. China is demanding that the US lift the tariffs (15%) imposed on September 1 on $112 bln of Chinese goods, which included a range of consumer goods (e.g., clothing, appliances, flatscreen monitors). Recall that the tariffs were announced over the objections of some of Trump’s advisers. The press reports suggest the issue is in Trump’s hand. Although the administration is fond of claiming that China wants a deal more than the US, Trump has seemed increasingly eager, and some gesture appears likely. Since the recent FOMC meeting signaled a pause after the three rate cuts, the market has been trying to determine where the bar is for further action. The answer was provided by San Francisco Fed President Daly yesterday and seemed to be echoed by other officials. Simply stated, there were have to be a material change in the outlook. The outlook does not change “materially” by any single piece of high-frequency data. It will take several months. Still, Daly hinted at one area that will be monitored closely, noting that inflation expectations are drifting lower. Today, Barkin, Kaplan, and Kashkari speak. None are voting members of the FOMC this year. |

U.S. Trade Balance, September 2019(see more posts on U.S. Trade Balance, ) Source: investing.com - Click to enlarge |

| The US reports the September trade balance and the October JOLTS and service/non-manufacturing PMI/ISM. The data poses minor headline risks. Canada also reports September trade figures, and here, non-oil exports are an important metric. The key report for Canada is the employment report at the end of the week. The most important report of the week for Mexico will be the October CPI on Thursday. It is expected to be unchanged at 3.0%. The central bank meets next week and is likely to pause before cutting rates again in December. |

U.S. ISM Non-Manufacturing Purchasing Managers Index (PMI), October 2019(see more posts on U.S. ISM Non-Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The softer neutral stance of the Bank of Canada last week lifted the greenback from around CAD1.3050 to around CAD1.3200. In subsequent trading, the US dollar has given back half of its gains. As the North American session is about to begin, the US dollar is overextended on the intraday charts. Support is seen near CAD1.3100. The risk for a bounce back into the CAD1.3130-CAD1.3140 area. For the fifth session, the dollar is chopping in a now well-worn range against the Mexican peso (~MXN19.05-MXN19.25). We continue to think it is more likely a base than a top.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,China Caixin Services PMI,Currency Movement,EUR/CHF,Eurozone Producer Price Index,FX Daily,India,newsletter,Sweden,U.K. Services PMI,U.S. ISM Non-Manufacturing PMI,U.S. Trade Balance,USD/CHF