Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

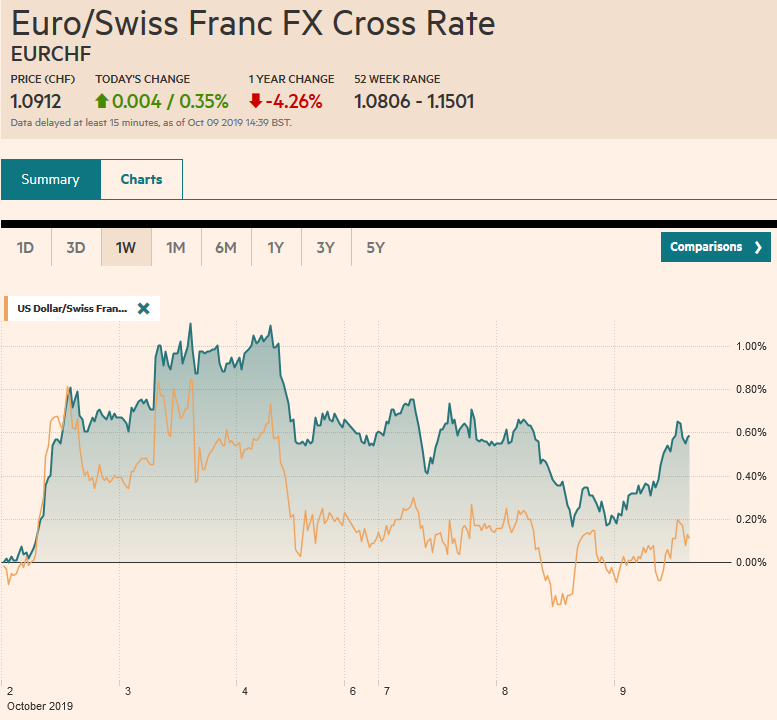

Swiss FrancThe Euro has risen by 0.35% to 1.0912 |

EUR/CHF and USD/CHF, October 9(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

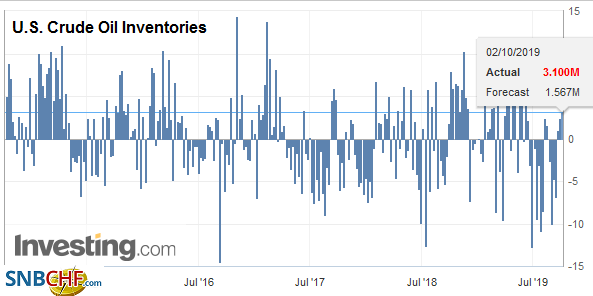

FX RatesOverview: The 1.5% drop in the S&P 500 and the deterioration of US-China relations and the prospects of a no-deal Brexit failed did not carry over much into today’s activity. Asia Pacific equities were mostly a little lower, though China and India bucked the regional trend, while Korea was closed for a national holiday. Taiwan led the losses amid a sell-off in semiconductor stocks. Europe’s Dow Jones Stoxx 600 is little changed as small early losses were reversed. US shares are firmer. The S&P 500 gapped lower yesterday, and that gap (~2925.5-2935.7) is important technically. Benchmark 10-year yields are a 1-2 bp higher, though UK Gilts are under a little more pressure. Separately, for the first time, a Greek bill auction resulted in negative yield. The dollar is softer against most of the major currencies, with the Japanese yen and Swiss franc not participating in the move. Among emerging market currencies, the Turkish lira is trading heaving as the country appears to have begun moving troops into Syria. The Chinese yuan strengthened. Gold is little changed slightly above $1500, while oil is pinned near its trough following news of a larger than expected rise in US oil inventories. |

FX Performance, October 9 - Click to enlarge |

Asia Pacific

On trade issues and national security, the US has opened a new front in its confrontation with China this week–human rights. After sanctioning nearly two dozen entities yesterday, including a couple of important surveillance equipment producers, the US has banned visas for Chinese officials involved with the mistreatment of Muslims in Xinjiang. The US federal government is also reportedly looking at ways to curb US government pension funds from investing in China. One such fund was to allow its investors to have access to international managers that track the MSCI All Countries Index, which includes mainland shares, by the middle of next year. Meanwhile, China has come down hard on the US National Basketball Association and has barred an episode of South Park that is critical of China. Expectations for this week’s meeting continue to degrade, and reports suggest the Chinese negotiating team has cut their visit short by a day.

Although President Trump has expressed little interest in a partial agreement like the one that was struck with Japan, China seems to be more sympathetic. It will do what it has been and what it needs to do, buy animal and plant-based protein (meat and soy), and in exchange, the US does not put any more tariffs on China. Indeed, China has offered to buy $10 bln of US agriculture products. The WTO allows bilateral free trade agreements as long as they are comprehensive. Limited trade agreements could be challenged, though the appellate process at the WTO will be compromised by the US obstructionist tactics that block the appointment of new appellate judges.

The US dollar is trading in a well-worn range against the Japanese yen. It is finding offers near JPY107.30, and bids have been uncovered a little below JPY107.00. Options for $2.5 bln at JPY107 expire today. Resistance may extend toward JPY107.45-JPY107.50. The Australian dollar continues to grind lower with lower highs for the third consecutive session, but when everything is said and done, it is little changed on the week. It finished last week near $0.6740, and it is trading there as this note is being composed. We suspect this flagging could be a favorable chart pattern, but the Aussie needs to find better traction soon and ideally rise above $0.6760.

Europe

An EU trial balloon a week ago that has a time limit to the Irish backstop is being recycled today. It would allow a reconstituted Northern Ireland assembly to decided after several years whether the backstop is still needed. It is not clear that Ireland has agreed to these terms. Also, note that in the non-binding referendum in 2016, Northern Ireland voted heavily to remain. The DUP from Northern Ireland, which supported the Tory government after it lost its majority, is itself a minority party. Meanwhile, the UK Times reports that another swathe of cabinet resignations are likely shortly.

Ireland, the EU country most vulnerable to Brexit, unveiled next year’s budget. It sets aside 1.2 bln euros to address the disruption. It forecasts 0.7% growth in 2020, which will feel horrible after this year’s 5%+ pace. It anticipates a 0.6% budget deficit after a small surplus this year.

EMU finance ministers are meeting today. Although the meetings rarely are impactful for investors, today’s is a watershed. The last details are expected to be hammered out that will finalize a small budget (~20 bln euros). The broad outlines were agreed in June. The size is smaller than the ambitious proposals but is seen as an important step. The budget will be part of the broader EU budget.

The euro continues to stay within spitting distance of $1.10 while finding bids in the $1.0940-$1.0950 area. The lower end of the range is reinforced today by the expiry of nearly 1.2 bln euro options struck at $1.0955-$1.0960. The 20-day moving average is a little below $1.0990. We look for an initial break higher, but the intraday technicals are already a bit stretched ahead of the US opening. Sterling is little changed and within yesterday’s range (~$1.22-$1.23). Both sides of the range have expiring options: almost GBP600 mln at $1.22 and about GBP525 mln at $1.23.

AmericaIn yesterday’s speech, Fed Chairman Powell indicated that the central bank would soon embark on a program that will permanently add reserves to the banking system. The current refi operations are for a fixed period, mostly overnight. To permanently increase the excess reserves, the Federal Reserve will purchase T-bills, Powell said. There were two other takeaways. First, Powell went to pains to distinguish what the Fed was going to do and quantitative easing, but many will still confuse the two. There are at least several differences. The amounts are considerably smaller. The Fed was buying around $85 bln a month under QE, and under this new “organic expansion,” it might be about $200 bln. Under QE, bonds were bought. Now short-term bills will be bought, which roll-off relatively quicker. We have long argued that the signaling impact of QE was significant but under-appreciated by many observers who tried calculating the price impact from quantities in some kind of mechanical way. The Fed is not signaling its intention to ease credit conditions through these purchases. Not all balance sheet expansion is QE. |

U.S. Crude Oil Inventories, October 2019(see more posts on U.S. Crude Oil Inventories, ) Source: investing.com - Click to enlarge |

Second, Powell seemed to suggest that an announcement will be made shortly before the next FOMC meeting. We had suggested it was important to keep the plumbing issues (repos, organic growth of the balance sheet) from monetary policy proper and thought that it would use the Oct 30 FOMC meeting to make the plumbing announcement, and cut rates at the year-end meeting. By moving up the plumbing announcement, it frees up the October meeting for a monetary policy decision. Between the soft PPI, (the 1.4% headline is the lowest in four years, and the 2% core rate is the lowest in two years), falling equities, and Powell, the odds of an October rate cut rose to almost 85%, according to both the CME and Bloomberg models.

Mexican officials anticipate that US Speaker of the House Pelosi will likely decide by early November whether to bring the new continental trade agreement to a vote. President AMLO can embrace the worker-friendly demand the US is making, though they are reluctant to put it into practice at home. Although overwhelmed by other considerations, like the broad risk-off mood characterized by the equity sell-off, sentiment has begun shifting in favor of US congressional approval. On PredictIt.Org, the odds of it being approved this year rose from about a one-in-three chance to almost a 50/50 proposition.

The US reports the JOLTS data on the labor market, which is not typically a market mover. The highlight will be the FOMC minutes from last month’s meeting. It will be interesting for color after the seeming divergence of views. We suspect opinion among the officials is not as fragmented as the dot plot would imply. The Board of Governors appears united, and several voting regional presidents that will support another rate hike. George and Rosengren, dissenters, are still not prepared to ease policy, but disappointing data could soften their objections and perhaps splinter it. Powell participates in a “Fed listening” event in Kansas today (10:30 am ET). Mexico reports September CPI figures today, and price pressures are expected to have continued to ease. A headline rate of 3.0% would be the lowest in more than two years and set the stage for another rate cut at the next meeting on November 14.

The US dollar’s upside momentum that lifted it above CAD1.33 is fading. A break of CAD1.3270-CAD1.3380 may be necessary to boost confidence that a high is in place (~CAD1.3340). The greenback is in a range of roughly MXN19.50 to MXN19.64 against the peso. As it tested the upside yesterday, and the dollar’s momentum eased, and better risk appetite may exist today, a probe of the downside seems more likely today.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,China,Currency Movement,EUR/CHF,federal-reserve,newsletter,Trade,U.S. Crude Oil Inventories,USD/CHF