Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

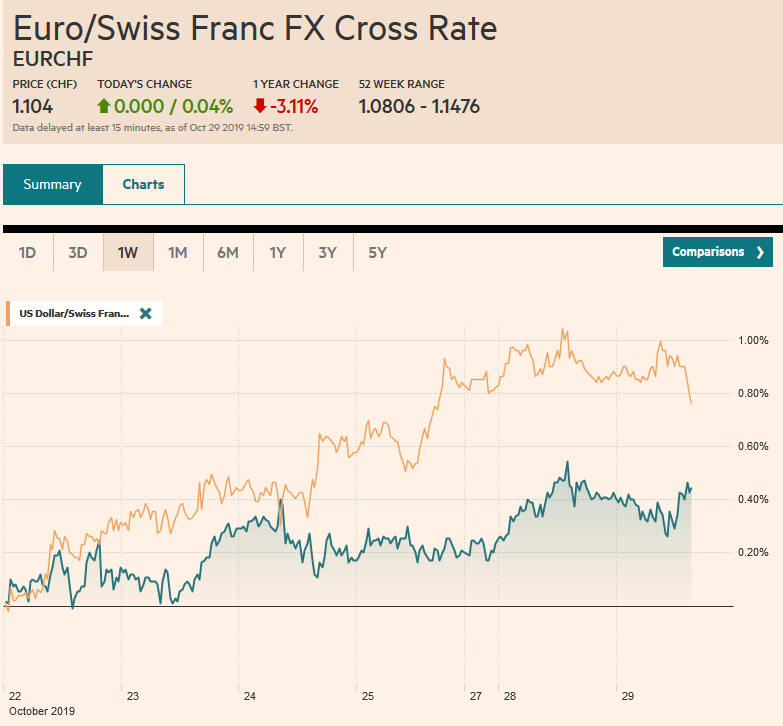

Swiss FrancThe Euro has risen by 0.04% to 1.104 |

EUR/CHF and USD/CHF, October 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The more prominent events this week still lie ahead, and the capital markets are trading accordingly. The rally that lifted the S&P 500 to new record highs yesterday carried over into Asia, where most equity markets rose, though China, Hong Kong, and South Korea were notable exceptions. European shares are struggling in the early going after the Dow Jones Stoxx 600 set new highs for the year yesterday. US equities are trading with a slightly softer bias in Europe. Benchmark 10-year bond yields are consolidating after Asia Pacific bonds played catch-up with the continued backing up in the US benchmark. Still, marginally weaker yields in Europe and the US, suggest consolidation may be in order ahead of the outcome of the FOMC meeting tomorrow. The dollar is firmer against most of the major currencies, and it is back below JPY109, and the euro is back below $1.11, levels that frayed yesterday. Central and Eastern European currencies are the drag among emerging markets, while South Korea and Taiwan are leading the advancers, which include South Africa, China, and Mexico higher. Gold is a little firmer after shedding $12 an ounce yesterday, and oil prices reversed lower yesterday and are experiencing follow-through selling today. |

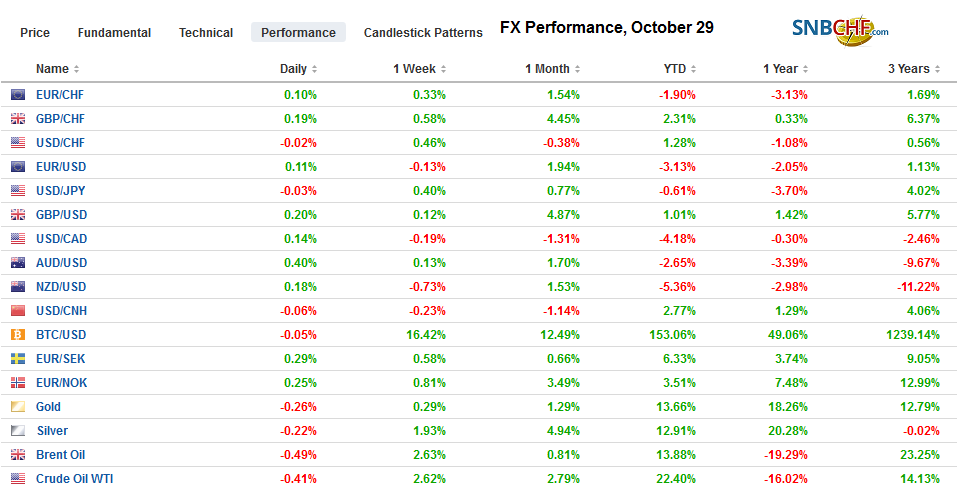

FX Performance, October 29 - Click to enlarge |

Asia Pacific

US-China trade talks continue to be a focus, and both sides are playing up the progress. The real test is a few weeks away. Can an agreement prompt the US to end the threat to slap a new tariff on around $160 bln of consumer goods imports due to take effect in the middle of December? The US canceled the increase in the tariffs on roughly $250 bln of goods from 25% to 30%, but those tariffs remain in place. Many of the concessions China appears to have offered are things that it has already done, such as set-up new courts for prosecution of intellectual property rights violations and commitment not to manipulate the yuan (which it has agreed at the G20), and lifting foreign-ownership caps in the financial sector.

China has sent conflicting signals, and this is seen in the volatility of the equity market. President Xi’s comments about the opportunities offered by the blockchain technology for China sent equities in the space higher, but today officials cautioned against speculation. Separately, China announced it will launch a ~$29 bln state fund to invest in the semiconductor chip industry (from design to manufacturing). This is not surprising and is consistent with the import substitution strategy and the reduction of dependence on the US.

Today’s Tokyo CPI figures, which are often seen as a lead indicator for national figures, disappointed, and the timing, ahead of the BOJ meeting, could not be worse. Headline October prices were unchanged at 0.4% year-over-year. The median forecast in the Bloomberg survey expected a rise to 0.7%, in part because of the sales tax increase (from 8% to 10% on October 1). However, the free education for young children that also took place at the start of the month appears to have blunted the impact of the sale tax on measured inflation. The core measure, which excludes fresh food, was unchanged at 0.5%. Economists expected a small rise here too. Excluding both fresh food and energy, Tokyo CPI rose 0.7% from 0.6%.

The dollar moved above JPY109 yesterday for the first time in almost three months, but, notably, Japanese participants did not extend its gains. The lack of Tokyo participation and $1.6 bln in options struck between JPY109.00-JPY109.10 that expire today may discourage aggressive dollar buying today. Note that the 200-day moving average is just above JPY109 as well, and the dollar has not closed above it in six-months. The base we noted that the Australian dollar carved out near $0.6800 has been a sufficient springboard to send it toward $0.6860 today. Last week’s high was set near $0.6880, and last month’s high was near $0.6900. These levels may stymie stronger gains until at least the FOMC decision tomorrow. The dollar continues to trade quietly in narrow ranges against the Chinese yuan.We note that Hong Kong’s decision to ban activist Joshua Wong from running in next month’s district council election may further antagonize the protest movement.

Europe

The Conservatives have tried to govern the UK as if it still had a majority. While former Prime Minister Cameron stepped down with a majority in Parliament, he ripped the country apart and laid the groundwork for the loss of the majority. He bequeathed two developments that have had a lasting influence. First is Brexit itself. It was supposed to help unite the party, and it did anything but. And despite the fatigue, even if an agreement is struck this year, UK negotiations with the EC on a new trade agreement may be just as contentious as anything we have seen thus far. It is still possible that the UK and EC do not reach an agreement, and the UK leaves with only the WTO rules. In the recent past, this was regarded as a hard exit before Johnson escalated the threat of leaving a divorce agreement. This remains a possibility if the deal Johnson struck enjoys no more success in the House of Commons than May’s version.

Second, Cameron checked the power to call snap elections away from the government. This is why Johnson’s attempt to call an election has been repeatedly frustrated. It requires a 2/3 majority, which he does not command. Later today, he will try a different approach to force an election. He will seek a bill that simply changes the scheduled election date to December 12. Such a bill requires a simple majority to pass. Sound’s simple, huh? The rub is that the bill can be amended with conditions that would not be acceptable to Johnson. Johnson potentially may attract support from the Lib Dems and Scottish Nationalist parties. However, seemingly violating previous promises to the Northern Irish and seeking an unreasonable long suspension of Parliament have undermined even a modicum of trust. The Lib Dems and SNP could come around if Johnson were to provide “cast-iron assurances” that he won’t reintroduce the EU Withdrawal Act Bill when the election bill is going through or before Parliament is dissolved.

The euro poked above $1.11 yesterday and tried again today before being turned back. We have suggested that last week’s losses were part of a correction that is still unfolding after a strong performance earlier this month. Recall that it began the month dipping below $1.09 for the first time in more than a year. Last week’s low was a little below $1.1075, and our first target zone is $1.1030-$1.1150. For its part, sterling has been unable to distance itself from $1.28. A break would target the $1.27 area, which corresponds to a retracement objective of the rally from $1.22 on October 10 and the 200-day moving average. The euro is trying to build a base against sterling near GBP0.8600. The GBP0.8700 area is the next target, but there is a large option (2.6 bln euro) that expires on Thursday that could frustrate gains.

America

The Federal Reserve’s two-day meeting begins today. The framing of the issue as a mid-course correction implied three rate cuts because that is how that term was used in the past. Officials have had plenty of opportunities to push against market expectations but have not done so. The real debate about this FOMC meeting is not about a cut or not, but the forward guidance. They want to say the midcourse correction is over, after all, many, including Powell, say the economy is in a good place. Perhaps it is because the economic data are understood as snapshots rather than a streaming video. The latter would show the US economy is losing momentum. The pace of growth is slowing, and the quality is deteriorating. Less than 48-hours after the FOMC’s decision, the October jobs report will likely show employment growth has slowed further, even when adjusted for the distortion caused by the GM strike. Some observers think that the Fed will signal in some fashion that unless the economy deteriorates further, it is on hold having completed the midcourse correction. The problem is that the economy ended Q3 with little traction, and the economy looks poised to slow further in Q4. We had penciled in 1% growth the current quarter, and the NY Fed’s GDPNowcast estimates it a 0.9%.

The economic calendar is light today. The US reports house prices, pending home sales, and the Conference Board’s measure of consumer confidence. These reports typically do not move the capital markets. Many observers have noted that the decline in interest rates has seen better traction in the housing market, but lower rates do not appear to have carried over to other sectors often thought to be sensitive to interest rates, like business investment or auto sales. Revolving credit has risen, which has helped underpin consumption, but delinquency rates on credit cards reportedly are increasing too. The economic calendar picks up tomorrow. In addition to the FOMC conclusion, the Bank of Canada meets and Mexico, like the US, reports Q3 GDP.

The US dollar is stuck in a narrow range against the Canadian dollar. The downside momentum that saw it fall from near CAD1.3350 in the ten days of the month to CAD1.3050 has stalled. A move above CAD1.3100-CAD1.3110 would confirm a near-term bottom is in place. The technical indicators look poised to turn higher and caution against extending short US dollar positions (or long Canadian dollar positions) until the likely correction unfolds. The US dollar did recover after dipping a little below MXN19.02 yesterday. In thin trading in Asia and early Europe, the greenback has held below MXN19.13. We continue to see potential toward MXN19.20 initially. Today is the third session that the Dollar Index is testing resistance a little below 98.00. A break targets 98.20 next, which corresponds to a (50% ) retracement of the decline since October 8 (~99.25) and the 20-day moving average. Above there lies 98.45 (61.8%) retracement, which we expect to be tested in the next day or two, before peaking with the employment report ahead of the weekend.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,China,Currency Movement,EUR/CHF,FX Daily,newsletter,USD/CHF