Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

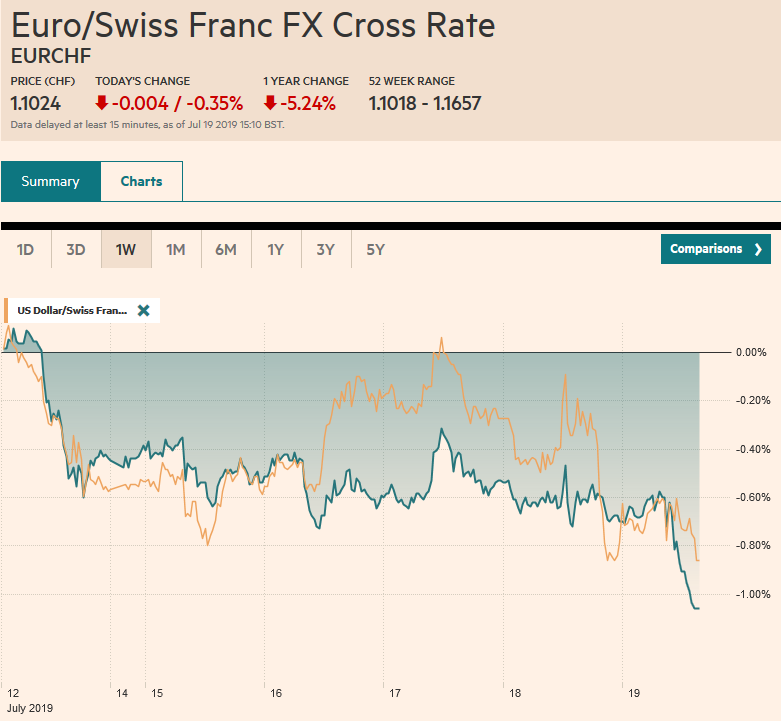

Swiss FrancThe Euro has fallen by 0.35% at 1.1024 |

EUR/CHF and USD/CHF, July 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Comments underscoring the importance of acting preemptively by two Fed officials sent the dollar reeling and helped lift equities after the S&P fell to a two and a half week low. The decline in rates and the US shooting down of an Iranian drone in the Gulf helped spur gold to new six-year highs. There was some attempt to clarify the (NY Fed’s) comments and the dollar has pared yesterday’s losses. However, there has not been a return to the status quo ante. Asia Pacific equities rallied strongly, led the Nikkei’s 2% gain. All the bourses in the region gained by India, which was suffered from continued foreign sales and the Asian Development Bank cutting its growth forecast. Europe’s Dow Jones Stoxx 600 was flat coming into today and the 0.6% gain through late morning turnover offsets the losses over the past two sessions. US shares are also trading firmer. Benchmark 10-year yields are a bit softer, mostly following yesterday’s move in the US. Gold is seeing its two-day, and roughly 2.8% rally retraced a bit, and oil is snapping a four-day and around 8.2% slide. |

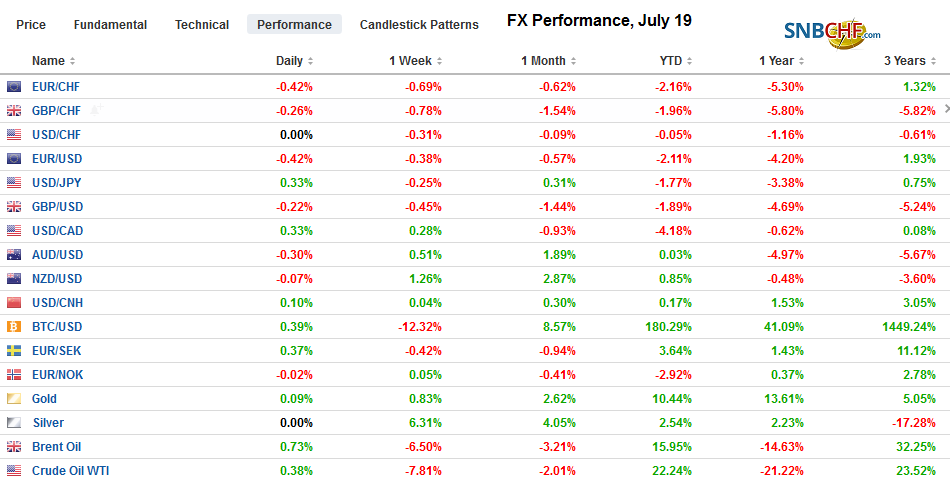

FX Performance, July 19 - Click to enlarge |

Asia PacificJapan’s Finance Minister Aso told the G7 gathering that there was scope for a fiscal response if Japan’s October sales tax weakened the economy. The BOJ has indicated it is prepared to support the economy if necessary. Today’s CPI report, showing measured inflation slipped to a two-year low may add pressure on the BOJ to ease. The headline CPI was unchanged at 0.7%, but the core rate, for which fresh food prices are excluded (and is the targeted rate) eased to a 0.6% year-over-year pace from 0.8% in May. |

Japan National Consumer Price Index (CPI) YoY, June 2019(see more posts on Japan National CPI, ) Source: investing.com - Click to enlarge |

| And even this may overstate the pressure. If energy prices are excluded as well, Japan’s inflation stood at 0.5% last month. Separately, Japan reported that its All-Industries Index rose 0.3% in May, following a revised 0.8% gain in April (from 0.9%). It is the first back-to-back increase in a year. It averaged -0.2% in Q1. |

Japan National Core Consumer Price Index (CPI) YoY, June 2019(see more posts on Japan National Core CPI, ) Source: investing.com - Click to enlarge |

Japanese investors have stepped up their purchases of foreign bonds. The latest Ministry of Finance report shows the buying spree was extended to the seventh consecutive week. Over this run, an average of JPY681 bln of foreign bonds has been bought a week. It is the highest since February and compares with an average of JPY183 bln for 2018.

Little progress appears to have been made between US and Chinese negotiators since the new tariff truce was declared. A couple telephone conversations have not led to setting a date for the next face-to-face meeting. US President Trump has criticized China for not stepping up its agriculture purchases as promised. The US Department of Agriculture reported yesterday that the PRC bought 51, 072 metric tons of sorghum from the US last week, the biggest in three months. China wants to see US licenses granted to allow sales to Huawei. Treasury Secretary Mnuchin tried to separate this from trade, but Trump and China see it differently.

The dollar sunk to nearly JPY107.20 yesterday, a little more than a yen lower from the week’s highs set on July 16. It has stabilized and recovered to JPY107.70. Yesterday’s high was smidgen above JPY108 and the roughly $410 mln option at last week’s close (JPY107.90) that expires today offer the initial cap. The Australian dollar advanced by a little more than 0.9% yesterday, according to Bloomberg, which makes it the largest single-day advance since the end of January. It drew closer to our $0.7100 target earlier today, reaching through $0.7080 today to set a new three-month high before sellers pushed it back toward $0.7055-$0.7060. The Aussie has only fallen in two weeks since the middle of March. The dollar remained in narrow ranges against the Chinese yuan. There was not a single day this past week in which the exchange rate changed by more than a net 0.1%, and in all but one session the rate changed less than 0.05%.

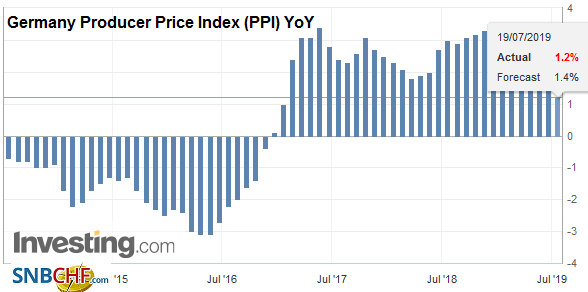

EuropeDespite calls from the IMF and others for Germany to boost spending and investment, Merkel continued today to defend the balanced budget. Even if German’s ordoliberalism does not put much stock in aggregate demand management through fiscal policy and the language sees “guilt” and “debt” to be the same, one might have expected the ability to borrow at negative interest rates would encourage the financing of some long-overdue infrastructure projects if nothing else. |

Germany Producer Price Index (PPI) YoY, June 2019(see more posts on Germany Producer Price Index, ) Source: investing.com - Click to enlarge |

Italian politics are at a potential inflection point. Here is the issue in a nutshell. League leader and Deputy Prime Minister Salvini have seen some bad press lately. A close ally has been seen talking with Russians about providing funds. Russia has reportedly funded the several right-populist or nationalist parties in Europe, ostensibly to foster divisions. There was a dispute over why he did not back Von Der Leyen as EC President. The League has polled well, but its performance in the European Parliament election was not nearly as strong as many anticipated. Salvini has been flirting with snap elections, but as President Mattarella warned him, he is running out of time. He has until July 20 if he wants a snap election in the fall. Salvini denies, but that is the way the game is played. We think the first step if Salvini pulls out of the coalition is not necessarily new elections. Instead, the President would see if a Parliament majority can be cobbled together without the League, such as the 5 Star and the center-left PD. Despite their denials (see rules of the game), they both may find it preferable than going to the polls now.

The proximity to Johnson becoming the next Tory leader and Prime Minister is sparking talk of resignations before dismissals among several cabinet officials. Justice Minister Gauke has stepped down. Parliament has passed legislative obstacles in the way of the next Prime Minister dissolving it to pursue a no-deal Brexit. If the measures are effective, they take away one of Johnson’s negotiating ploys. If the measures are ineffective, then a constitutional crisis (without a constitution) may ensue. Sterling is firming against the euro for the third consecutive session today, the longest streak in two months. It is not yet sufficient to avoid extending its weekly losing streak to a new record of 11 weeks.

The euro tested the lower end of its range (~$1.12) and recovered to the top end of its recent range ($1.1280) yesterday. It is returned to the middle of the range as yesterday’s gains are pared. Within the range, initial support extends toward $1.1230. Three-month implied volatility, a benchmark, has quietly extended its advance for a seventh consecutive session. During this run, it has risen from near 4.95% to 5.25%. It finished last month near 5.65%. Sterling traded to almost $1.2560 yesterday. It had traded near $1.2380 the day before, which was new lows for the year. It has pulled back to nearly $1.25, where a GBP220 mln option is set to expire today. Sterling closed last week near $1.2520.

America

NY Fed Williams and Fed Governor Clarida spoke of the importance of swift preemptive action, and this swung sentiment sharply in favor of a cut in rates at the end of July. The CME’s model shows the probability doubling to nearly 70% and has now pulled back to about 50%. It is as if the market currently thinks likely 75 bp cuts in H2 frontloaded. Minneapolis Fed’s Kashkari (non-voter) seemed isolated a couple of weeks ago with his call for a 50 bp cut. At the time, St. Loius Fed’s Bullard, who dissented at the June meeting in favor of an immediate cut, seemed to distance himself from such a large move. He speaks later today and may reiterate this view. We suspect the market is confusing timing with magnitude. Williams and Clarida are Vice-Chairs of the FOMC and Federal Reserve Board, respectively. Their audience may have been some of their colleagues, some of whom do not appreciate the urgency. Williams and Clarida simply may have wanted to boost the chances of a unanimous decision to cut.

The US economic calendar features the Fed’s Bullard and Rosengren and the University of Michigan’s preliminary July report. The 5-10 year inflation outlook, which the Fed has cited, was at cyclical lows of 2.3% in June. It has not been above 2.6% for more than three years. A new low could reignite the bond market rally. Canada reports May retail sales. A stronger showing after a 0.1% increase in April is expected. Retail sales soared in February and March (1.0% and 1.3% respectively) after falling in the previous three months.

The US dollar made a new marginal low for the year against the Canadian dollar near CAD1.3015 in Asia but has come back a bit better bid. The intraday technicals and the $515 mln option that expires today warns of potential resistance near CAD1.3050. The greenback finished a little below CAD1.3030 last week and a close above there would break a four-week slide. The dollar dipped below MXN18.93 earlier today, which is the lowest it has been since the unexpected resignation of the finance minister on July 9. Still, it is practically flat on the week. Initial resistance ahead of the weekend is seen in the MXN19.05-MXN19.10 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Currency Movements,EUR/CHF,Federal Reserve,FX Daily,Germany Producer Price Index,Italy,Japan,Japan National Core CPI,Japan National CPI,newsletter,USD/CHF