Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

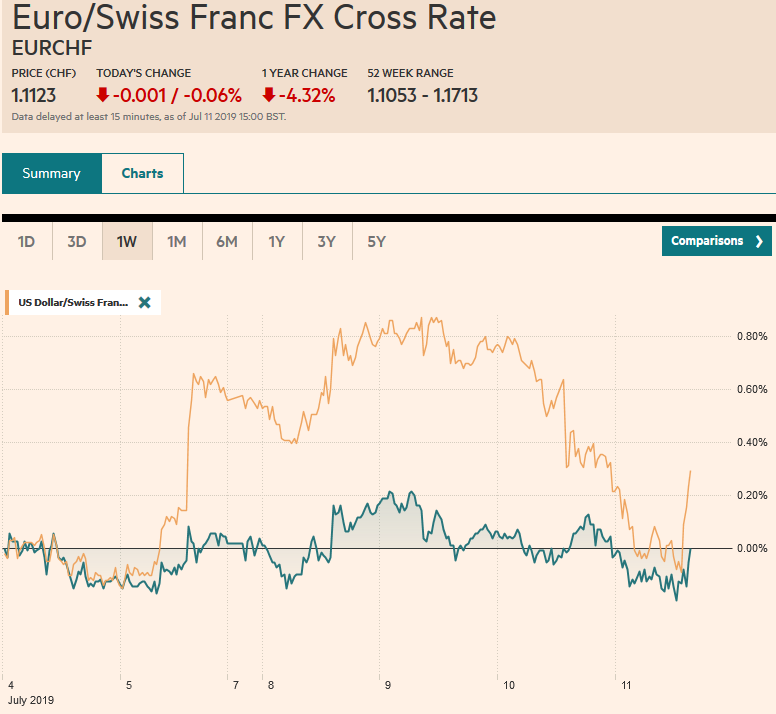

Swiss FrancThe Euro has fallen by 0.06% at 1.1123 |

EUR/CHF and USD/CHF, July 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Fed’s Powell confirmed a Fed rate cut at the end of this month by warning that uncertainties since the June FOMC had “dimmed the outlook” and that muted price pressures may be more persistent. It ignited an equity and bond market rally (bullish steepening) while the dollar was sold. The MSCI Asia Pacific Index rose for the second session, led by gains in South Korea and Hong Kong. Benchmark 10-year yields have slipped lower, with the Asia Pacific and core European yields are 1-2 bp lower. Peripheral European yields are 2-5 bp lower. Chinese markets showed a more muted response. US shares are trading firmer, and the S&P 500 is poised to push above 3000 in early activity. The dollar is broadly lower. Against the majors, yesterday’s losses have been extended by 0.2%-0.4%. Most emerging market currencies are also stronger, with the Turkish lira an exception, finding little traction. |

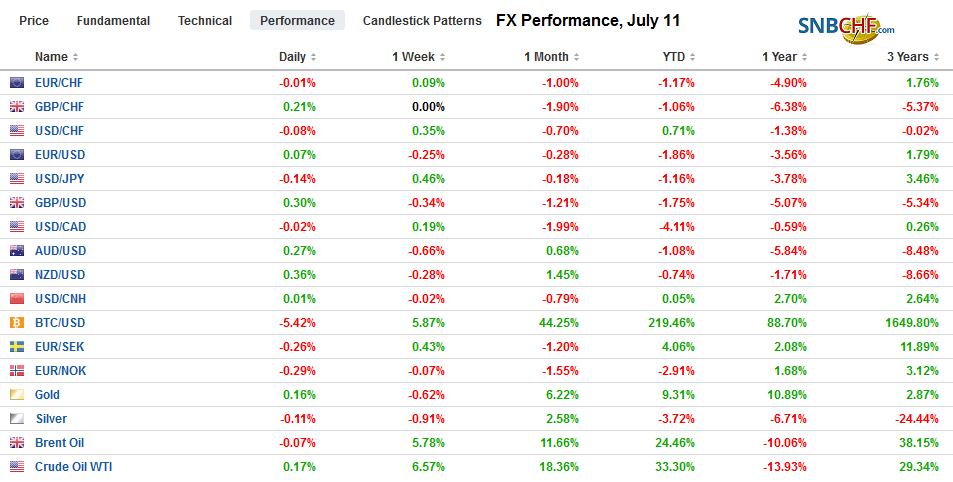

FX Performance, July 11 - Click to enlarge |

Asia Pacific

Japan’s tertiary industries index was weaker than expected in May, falling 0.2%. It leaves the country’s household consumption as one of the few bright spots, and this could be partly bringing forward purchases ahead of the sales tax hike in three months. While unemployment remains low and jobs ample, wage growth remains poor, and this also warns of the risks to consumption. The sharp drop in machinery orders is seen to presage a weakness in capital expenditures. The BOJ, which meets the day before the Fed at the end of the month, is seen to be willing to extend forward guidance. With soft price pressures, including yesterday’s reported decline in producer prices, the BOJ will struggle to steepen the yield curve, which was the intent of the recent adjustment of its bond purchases. Given the yen’s rise, the equity market gains (0.4%-0.5%) were striking. Separately, Japanese and Korean officials are due to meet tomorrow. Talks are a necessary pre-condition to resolving the dispute.

Australia reported a slight decline in inflation expectations (July 3.2% vs. June 3.3%). It is the lowest since late 2016. Loans for housing fell for the third consecutive month, though the 0.1% decline was much less than expected (~-1.0%). Loans have fallen by an average of 0.9% through May compared with an average decline of 0.6% in the first five months of 2018. After cutting the cash rate June and July, the RBA is not expected to refrain from cutting rates again until Q4.

Yesterday, the US dollar came within 1/100 of a yen of JPY109, a key chart point, and in Asia today it pushed through JPY108 (low ~JPY107.85). It has been in a narrow range in the European morning, a little above JPY108.00. Large option expiries may give a sense of the near-term range. On the wide, there are around $2.1 bln in expiring options struck between JPY107.65 and JPY107.80. There are also about $2 bln in expiring options between JPY108.30 and JPY108.50. There is a more modest amount (~$665 mln) at JPY108. The Australian dollar has recovered smartly from testing $0.6900 yesterday to now looking poised to challenge $0.7000. Last week’s high was near $0.7050, and a trendline from April’s high comes in near $0.7035 tomorrow. China’s yuan edged higher to a new eight-day high, but it is simply back to where it was at the end of June.

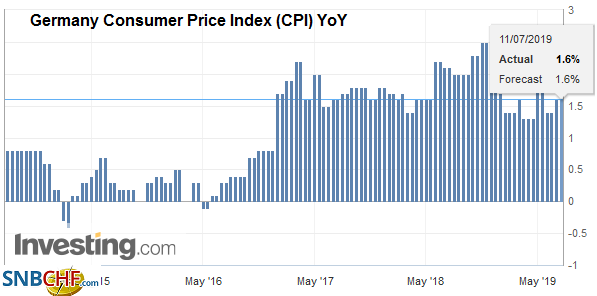

EuropeThe dovishness of the Federal Reserve coupled with signals from officials, has spurred speculation that the ECB could deliver a rate cut at its meeting on July 25. The OIS market appears to be pricing in around a one-in-three chance up from a one-in-four chance yesterday. Lane, the ECB’s chief economist, indicated a preference to act sooner rather than later and emphasized the benefits of being proactive. Coeure, the head of market operations, opined that easier policy was needed more than ever. News that Germany’s June CPI estimate was revised to 0.3% from 0.1% (lifting the year-over-year rate to 1.5% from 1.3%) does not stand in the way of ECB actions. |

Germany Consumer Price Index (CPI) YoY, June 2019(see more posts on Germany Consumer Price Index, ) Source: investing.com - Click to enlarge |

We have been concerned that a new tariff truce between the US and China would free up bandwidth for the Trump Administration to turn to Europe as its next trade focus. France’s plan to tax large digital service firms may provide fresh fodder for the already simmering tensions. The US has launched a Section 301 investigation, which is the same tool that was used to levy a tariff on Chinese goods for intellectual property right violations on grounds that US interests are being harmed. Separately, despite Trump encouraging the UK to leave the EU and offering a free-trade agreement, negotiations have reportedly (Telegraph) have stalled. Although staffing and communication issues are blamed by the report, the ultimate problem maybe national interests. Common ground has yet to be found, for example, in finance and agriculture.

The euro, which dipped below $1.12 earlier in the week, extended its rally to $1.1280 in Asia before moving sideways in the European morning. This meets the (38.2%) retracement of the loss since last month’s high (~$1.1410). The next retracement (50%) is found a little above $1.1300. The euro has not closed above its 20-day moving average (~$1.1285) since the end of June. Above there, the 200-day moving average is found now around $1.1325. Initial support is seen near $1.1250. Sterling is firm (~$1.2530) and showed little reaction to the news that it successfully rebuffed Iranian effort to seize a UK oil tanker in the Gulf as retaliation for the seizure of one of its ships. Sterling fell to new lows for the year on Tuesday and recovered yesterday and extended those gains today, but it is understood as a reflection of the dollar’s weakness. Sterling is headed for its 10th consecutive weekly loss against the euro, which appears to a record-run, though the euro has not yet convincingly pushed through GBP0.9000, and the year’s high was set in early January above GBP0.9100.

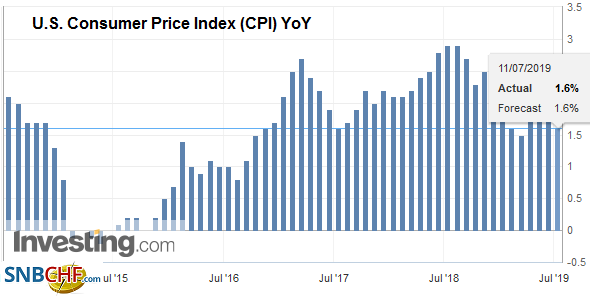

AmericaPowell’s testimony effectively unwound the interest rate adjustment spurred by last week’s jobs report. Indeed the Fed Chair encouraged such a move by explicitly noting that the employment report, which many had put an emphasis on, did not change the central bank’s policy outlook. The fed funds futures market returned to pricing in around a 1-in-4 chance of a 50 bp move this month from practically nothing. The implied yield of the January 2020 contract fell nine basis points to 1.685%. It was 1.645% the day before the employment report and bottomed near 1.55% on the last day of Spring. The June CPI report today will confirm the softness of price pressures. The headline may be flat, which would pull the year-over-year rate to 1.6% from 1.8%. The core rate may tick up by 0.2%, but this will only be enough to keep the year-over-year rate steady at 2.0%. And softness will encourage the market to extend yesterday’s moves further. |

U.S. Consumer Price Index (CPI) YoY, June 2019(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

Like the Fed, the Bank of Canada emphasized the trade tensions and called them the biggest risk facing the Canadian economy. While acknowledging growth in Q2 was likely stronger than previously projected (now 1.3% vs.1.0%), temporary factors, such as rebound from the unseasonably cold winter and the surge in oil output may have been responsible. The central bank recognized that the housing market was stabilizing nationally and that consumption was fueled by the healthy labor market.

Our heuristic device of three drivers of the Canadian dollar: two-year rate differential, oil and S&P 500 (as a proxy for risk) all aligned for a stronger Canadian dollar. The US premium over Canada has narrowed has been halved over the past month to about 25 bp. Recall it hit a high of this year in March around 85 bp. Oil prices soared after the US confirmed a large drop in oil inventories. It was the fourth consecutive weekly drop, during which time the drawdown has been around 26 mln barrels. Also, an approaching storm in the Gulf of Mexico has shut down around a third of the region’s oil production and a fifth of the gas output. WTI for August delivery is at its highest level in nearly two months. The S&P 500 briefly poked above 3000 for the first time before settling a little below. The NASDAQ also rallied strongly and closed at a record high.

The US dollar is just above the lows for the year against the Canadian dollar. Before Powell’s testimony yesterday (round two today), the US dollar was in the upper end of its recent range, and the divergence of central bank signals has sent the greenback to the lower end. The CAD1.30 seems more of a psychological level than an important technical level. The next important chart area is closer to CAD1.2850-CAD1.2900. The Mexican peso is at its best level since the unexpected resignation of the finance minister at the start of the week. In fact, with today’s US dollar slippage to around MXN19.10, the greenback has given back around half of those gains. The next target is closer to MXN19.00-MXN19.05. It was trading closer to MXN18,90 when the news first broke. Lastly, Brazil’s lower house approved the basic text of pension reform by a wide margin, boosting optimism among investors that this key reform, which has been derailed in the past, can actually be implemented. The dollar fell to four-month lows against the Brazilian real yesterday (~BRL3.75). The central bank meets at the end of July and expectations for a rate cut may increase. The Selic Rate has been at 6.5% since March 2018.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CAD,Brazil,ECB,EUR/CHF,Germany Consumer Price Index,newsletter,OIL,U.S. Consumer Price Index,USD/CHF