Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

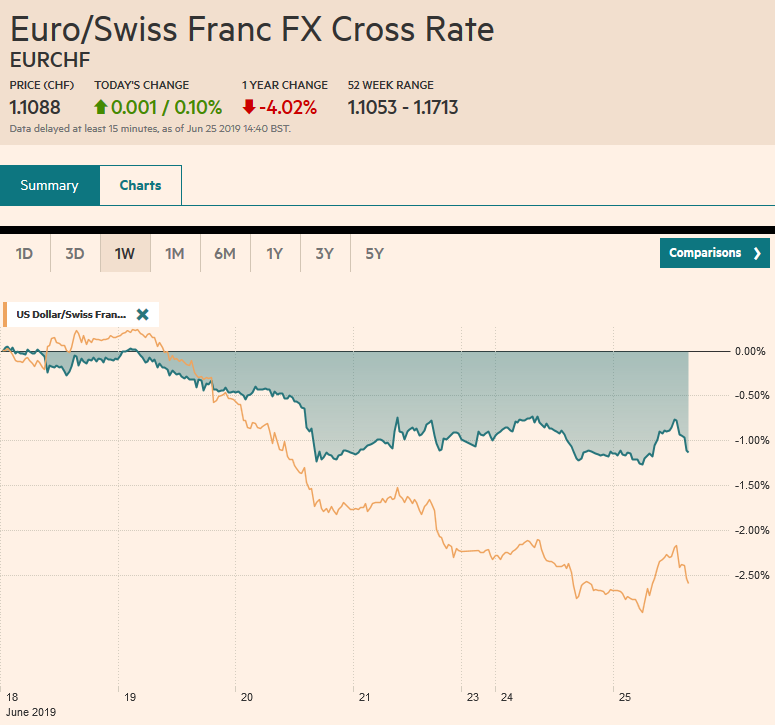

Swiss FrancThe Euro has risen by 0.10% at 1.1088 |

EUR/CHF and USD/CHF, June 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: It is far from clear that the US sanctions against nine Iranian officials, with the foreign minister to be added later brings negotiations any closer. At the same time, US officials trying to keep expectations low for the weekend meeting between Trump and Xi. The heightened political anxiety will have to make room for Fed Chairman Powell’s talk in NY. The market is confident of at least a 25 bp cut at the next FOMC meeting at the end of July. Stocks are pulling back today. Most of the major markets in Asia Pacific fell, with India a notable exception. Europe’s Dow Jones Stoxx 600 is off for a third session, its longest losing streak in three months, and is approaching this month’s uptrend line. US shares are also trading with a downside bias. After last week’s run-up, some backing and filling ought not surprise. Most benchmark 10-year yields are a little softer, with the US flirting with 2% and Germany at minus 30 bp. Italian and Greek bonds are underperforming, and yields are slightly firmer. The dollar is narrowly mixed. Despite the heightened tensions, it is ironic that the yen is up about 0.2% (~JPY107.15), while the Swiss franc is the weakest of the majors, off around a third of a percent (~CHF0.9755). Emerging market currencies are also mixed. Oil trading heavier, while gold is extending its run into a sixth session, over which time it has rallied about 7%. |

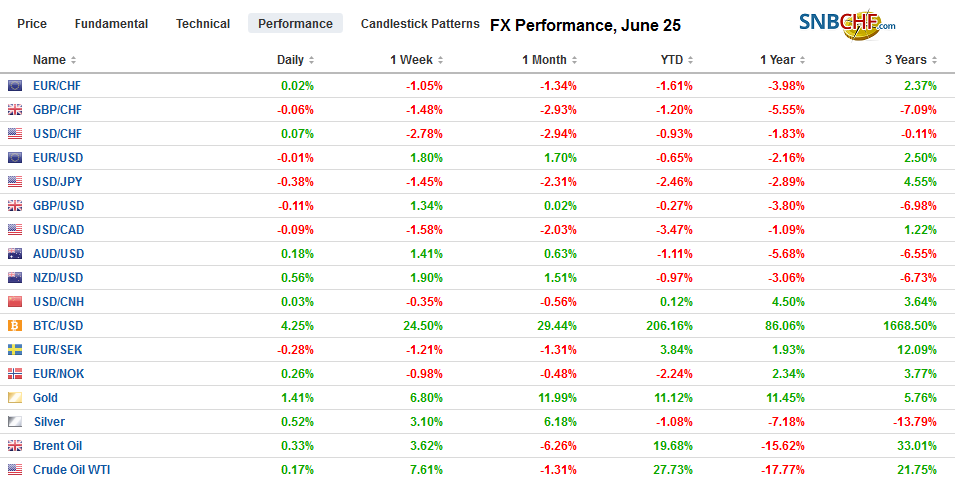

FX Performance, June 25 - Click to enlarge |

Asia Pacific

The US is pressing Iran hard. The economy is crippled through the embargo and now adding insult to injury, the US has sanctioned the Supreme Leader, Ayatollah Ali Khamenei, and eight senior military officers. The foreign minister is expected to be added shortly. At the same time, the US says it is open to negotiations, but at least at first, Iran seems to be moving in the other direction. One risk is that is it solidifies Iran’s relationship with Russia, which could help it economically and militarily.

The US also says it wants to negotiate with China, but its actions seem to make it more difficult. The latest US blacklisting of a handful of Chinese companies involved with developing China’s supercomputer is not for violating an embargo or spying but appears to be primarily commercial competition. Separately, and with some impact in trading today, the press reports that a US judge found three Chinese banks in contempt for refusing to comply with subpoenas regarding activity that may have violated the sanctions against North Korea.

The dollar fell through JPY107 for the first time since the flash crash on January 3. It found some bids in late Asia near JPY106.80 and resurfaced above JPY107 by early European turnover. There is an option for a little more than $900 mln at JPY107.25 that expires today. Note that a $1.4 bln option at JPY107 is on the bubble tomorrow. There are also $2.2 bln in options between JPY107.30 and JPY107.50 that will expire tomorrow and will likely offer resistance today. The Australian dollar is edging higher and is looking to extend its advance for the sixth consecutive session. Over this run, it has appreciated by a cent. It is testing trendline resistance from mid-April peak (~$0.7200) and the high from earlier this month (~$0.7025). Rate cut expectations for a move next week continue to run high (~80% chance).

Europe

From the outside, it appears to be a disconnect between what the EC is saying and what the candidates for Tory leader are advocating. The EC states that it will not re-negotiate the Withdrawal Agreement, yet both candidates seem to think this is a bluff. Johnson claims that a majority of Parliament now support a no-deal exit, but that also does not seem likely. In fact, several high profile Tory MPs have threatened to vote against the government were it to seek such a course. With four months left until the end of October deadline, the next month will not feature talks with the EU, but the selection the next Tory leader. Our bias is toward a national election that will again postpone the exit date.

Italy has now another week to persuade the EC not to proceed with excessive debt procedures. EU finance ministers meet on July 8-9 and will take up the recommendation of the EC. While the Prime Minister and Finance Minister pledge adherence to the EU budget rules, the squabbling coalition appears pushing in the other direction. It is not so much about the “mini-BOTs”–the uses of a new T-bill offering in some denominations, which as the ECB has noted is either a parallel currency, which is illegal or a debt instrument that would have to be added to the country’s obligations and is also problematic. Rather, League leader Salvini is pressing ahead with his pledge of a flat tax, and he is seeking inclusion next year’s budget. There are suspicions that Salvini is trying to antagonize the EC to precipitate a political crisis that could lead to new elections and replace the unwieldy coalition with the Five Star Movement with a center-right coalition that he would ostensibly lead.

The euro initially extended its gains for the fifth consecutive session but is reversing lower after briefly poking above $1.1410. Initial support is pegged near $1.1380, but if this goes, a move back into the $1.1325-$1.1350 area is likely. Sterling is outperforming the euro. With today’s gains, its advancing streak is in its sixth session, during which time, sterling has gained a little more than two cents to test the $1.2780 area today. The momentum appears to be stalling and a lower close today at the end of the North American session cannot be ruled out. Support is seen in the $1.2720-$1.2740 area.

AmericaFive Fed officials speak today, but the focus is on Chairman Powell’s remarks at 1:00 pm ET. The issue that is on the top of everyone’s mind is the outlook for policy. The market has increased the odds of a 50 bp move at the end of next month to nearly 40% from practically no chance at the end of May. Some argue that there have been cycles in which the Fed initiated with a 50 bp move. Two differences strike us. First, rates were considerably higher so that proportionately, the 25 bp now is roughly the same as 50 bp then. Second, the ostensible purpose of the cut is not to arrest economic deterioration. In fact, the Fed’s dot plot reaffirmed its growth and unemployment forecasts. The issue, the way the Fed framed it, was the uncertainty around forecasts have increased. |

U.S. House Price Index YoY, April 2019(see more posts on U.S. House Price Index, ) Source: investing.com - Click to enlarge |

The Dallas Fed’s Kaplan took the opposite tack from what the fed funds futures are showing. He suggested adding more stimulus now could contribute to building up excesses and imbalances in the economy. Kaplan noted that financial conditions and the availability of credit are robust. Some observers are stressing the importance of next week’s US jobs report, but Kaplan suggested that what appears to be a low estimate of job creation (60k-120k) that would be acceptable.

Mexico’s two-week inflation report showed price pressures eased to 4% in the first half of June. This is the top of the central bank’s 2%-4% target. However, the core rate ticked up. The central bank meets Thursday, and no rate cut is expected. Many expect a decrease in Q3, while others have it at the end of the year. Pressure is building for lower rates. The IGEA economic activity index, a proxy for GDP reported yesterday, fell 1.41% year-over-year in April after averaging 1.18% in Q1. It is the first negative reading since March 2018. Today Mexico reports April retail sales and a small bounce is expected after sales slipped 0.2% in March.

After dipped below MXN18.90 last week, the US dollar is advancing against the peso for the third consecutive session. It is trading near a two-week high now near MXN19.23. Technically, we look for a test on the MXN19.33 area, which is the high since the tariff threat was suspended. Ahead of that, the 20-day moving average can be found near MXN19.29. The Canadian dollar continues to consolidate last week’s gains. The US dollar continues to be confined to its pre-weekend range (~CAD1.3160-CAD1.3230). The intraday technicals warn of the risk to at least the upper end of the range. The Dollar Index spiked to 95.85 today before finding a bid. Its recovery today is threatening to put in a bullish hammer candlestick pattern. If so, some follow-through buying toward 96.40 would not surprise.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,EUR/CHF,Iran,Italy,Mexico,newsletter,U.S. House Price Index,USD/CHF