Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

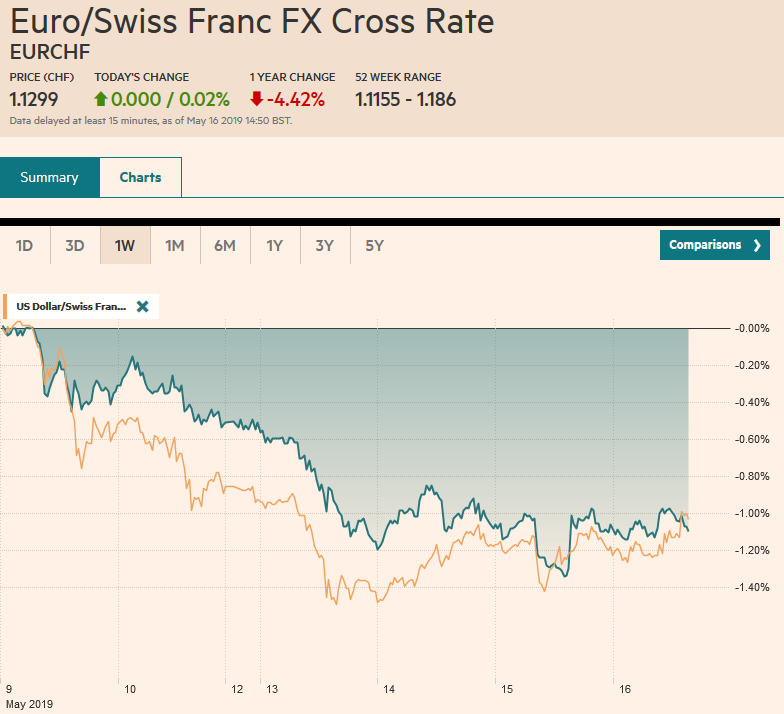

Swiss FrancThe Euro has risen by 0.02% at 1.1299 |

EUR/CHF and USD/CHF, May 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Retail sales and industrial production disappointed in both the US and China prior to the end of the tariff truce, declared by the US in a series of presidential tweets on May 5. The reaction function of the US to the drop in equities was to play down tensions on three fronts. First, a US team is expected to return to Beijing in the coming weeks. Second, Trump pushed out the decision about auto tariffs until the end of the year and hangs over the bilateral talks with Japan and Europe. Third, Treasury Secretary Mnuchin revealed that the US was close to resolving the steel and aluminum tariffs with Canada and Mexico but explicitly stated that this does not mean that the tariffs are being lifted. Asia Pacific equities were mixed after the S&P 500 gain about 0.6%, with China, Australia, and India moving higher. Japanese shares have fallen in seven of the eight sessions since the extended holiday ended. Bond markets are firm. A milquetoast jobs report from Australia that saw unemployment rise to 5.2% from a revised 5.1% sent the 10-year yield down five basis points to about 1.63%, to approach the cash rate (1.50%) as the market pushes rate cut expectation forward. The US 10-year is just below 2.36%. It had seemed to bottom near 2.34% at the end of March. The 10-year German Bund yield is recording new two-year lows (minus 11 bp). The low point in the summer of 2016 was minus 20.5 bp. The dollar has a slightly heavier bias against the major currencies through the European morning. Sterling is underperforming as Brexit anxiety continues to take a toll. The Chinese yuan was slightly softer though within the ranges seen in recent days. |

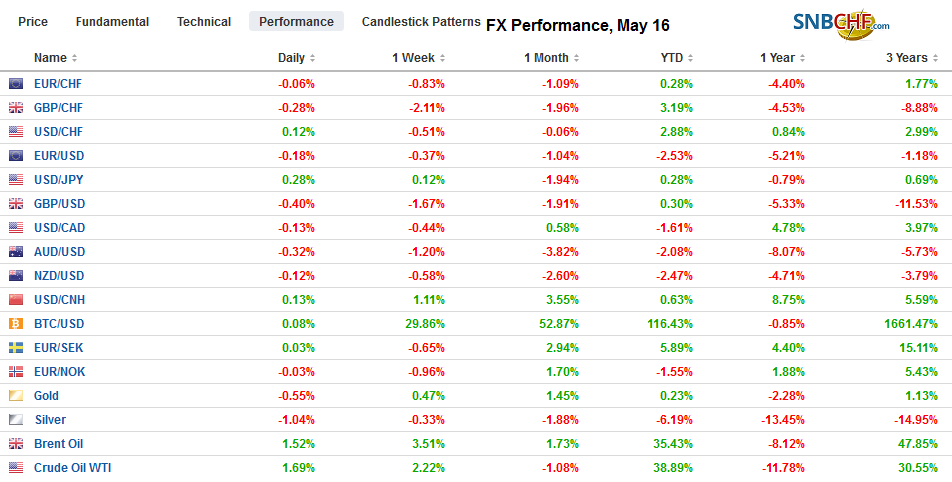

FX Performance, May 16 - Click to enlarge |

Asia PacificAs well telegraphed, the Trump Administration took action that will essentially restrict Huawei and ZTE from selling 5G equipment in the US. Many observers are framing this in terms of the trade tensions. However, it may be important to separate the trade issue from the other multi-faceted confrontation between the US and China. The initial charges are not about the potential for espionage, but for violating the trade restrictions against Iran. The US has thus far been mostly unsuccessful in getting other countries to ban Huawei though some, like the UK, took precautionary steps to limit its presence. Violations of trade restrictions typically are punished by fines, not arrests. |

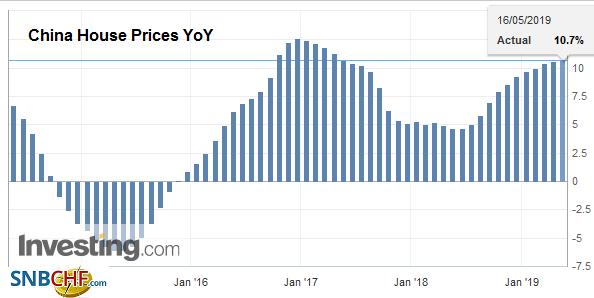

China House Prices YoY, April 2019(see more posts on China House Prices, ) Source: investing.com - Click to enlarge |

| Many observers are also stretching to link another story to the trade tensions. The US Treasury data showed that China reduced its Treasury note and bond holdings by $20 bln in March, the most in more than a year. What is unusual, according to some observers quoted in the press, is that ebb and flow on China’s holdings appears to have more to do with controlling the yuan than the investment considerations like yield. However, in March, the yuan was firm. The dollar has frayed the lower end of where officials seemed to indicate they were prepared to accept (~CNY6.70). However, the first thing that is important to note is that nearly half of the proceeds from the liquidation of US bonds and notes were recycled into short-term securities, like bills. When this is taken into account, China’s holds fell. In fact, the decline in March was the first in four months. The $10 bln fall in overall holdings was less than 1%. In this imprecision of the TIC data and the fact that it subject to revision as transactions in financial centers often later get redistributed to the beneficiary buyers. With China’s vast holdings and questionable intent, it makes sense to monitor its activities in the US bond market, the weaponization of their holdings, we argue, come at a high price (in terms of return, liquidity, and transparency) and represents a much higher rung in the escalation ladder. |

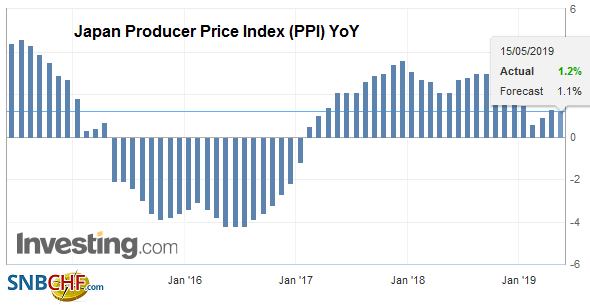

Japan Producer Price Index (PPI) YoY, April 2019(see more posts on Japan Producer Price Index, ) Source: investing.com - Click to enlarge |

Australia reported that it created 28.4k jobs last month, which was a little more than March, and nearly double expectations. However, it was not sufficient to curb rate cut speculation. All the jobs created were part-time positions. The number of full-time positions fell by a 6.3k. The participation rate increased (65.8% from 65.7%), but the new entrants did not find work, and the unemployment rate rose to 5.2% from a revised 5.1% (initially 5.0%). Interpolating from the overnight index swaps, the market had raised the odds of a cut next month to a little more than 50% from nearly 40% yesterday.

The Australian dollar initially was sold off. It briefly dipped below $0.6900 but reversed higher to test the $0.6930 area before stalling in the European morning. A move, and ideally a close above $0.6940-$0.6950 is likely needed to signal a low is in place. The dollar remains within Monday’s range against the yen as it has all week. In each session, the range has been compressed. Today’s range has been about a quarter of a yen. The pattern is often associated with a continuation of the near-term trend, which is lower. There are options for about $1.3 bln in between JPY109.40 and JPY109.50. Previous support near JPY110 is now resistance.

EuropePrime Minister May will meet with the party backbenchers today. She is coming increased pressure to step down by the middle of next month. The most likely scenario is that after the European Parliament elections, which likely will be the third election that May has led the Tories into defeat, she will offer Parliament another go at the Withdrawal Bill. It has been defeated three times already. The risk, May says, is if not the Withdrawal Bill, perhaps the UK does not leave at all. If May is replaced, a hard Brexiter will be her likely successor. This raises the risk of leaving without an agreement, and the success of the Brexit Party in the EU Parliament elections (though it has no representation in the UK Parliament) may embolden the hard exit camp. |

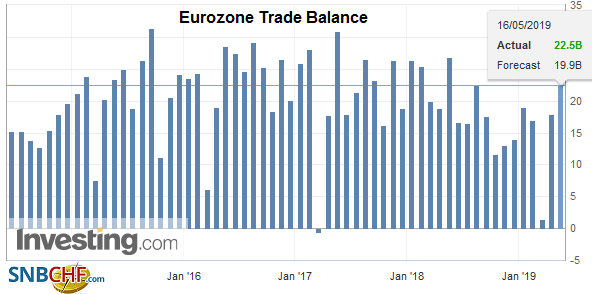

Eurozone Trade Balance, March 2019(see more posts on Eurozone Trade Balance, ) Source: investing.com - Click to enlarge |

Italian bonds are participating in today’s rally. The benchmark 10-year yield is off around 4.5 bp, which recoups nearly the entire loss of the first part of the week. Note that despite the firmer bond tone, Italian bank shares have extended their losses. An index of bank stocks is off almost 15% since peaking in mid-April. Italy’s challenges are mounting in the broad risk-off environment. However, there has been some deterioration in the macro backdrop, including Blackrock’s pullout of support for Carige, a troubled Italian lender. The slower growth will push toward a wider deficit without corrective action, and the EU warned of further fiscal deterioration next year. The outcome of the European Parliament elections will likely influence the course of Italian politics, with a strong showing by the League seen emboldening Salvini to precipitate a crisis in the government, which is not particularly difficult, forcing a new election that could lead to a new center-right government.

The euro recovered after being pushed a little below $1.1180 yesterday. It finished the US session little changed, but above $1.1200. Today, it returned to yesterday’s high (~$1.1225) before finding sellers in the European morning. The recent North American bias has been to sell the euro in the morning and buy it back after Europe closes. Sterling is a dog. It is off against the dollar for the fourth consecutive session. It has fallen against the dollar in eight of the past nine sessions. It is approached the mid-February lows found near $1.2775, which is the next obvious target. Against the euro, it is even worse. It has fallen in all nine sessions. It appears to be the longest losing streak since 2000. The euro is trading at its best level against sterling in three months as it pushes further above GBP0.8720, where the (38.2%) retracement of this year’s losses is found. The 50% retracement is located closer to GBP0.8790.

America

The disappointing April consumption and production data in the US will prompt economists to lower their Q2 GDP forecasts. The Atlanta Fed’s GDPNow tracker sees 1.1% growth rather than 1.6%. Industrial output fell for the third time in four months. It was driven by the 0.5% decline in manufacturing output, but utility output fell 3.5% to a four-month low, while mining/extractive rose (1.6%) for the first time in four months. The manufacturing sector saw broad declines, but vehicles and machinery were particularly weak. Perhaps mitigating the sting was that the May Empire State manufacturing survey was stronger than expected and rose to its best level since last November. However, the auto and light truck sector that was a drag on manufacturing was also partly responsible for the disappointing retail sales report. Retail sales fell 0.2%, but excluding auto sales a small gain of 0.1% would have been recorded. The median forecast in the Bloomberg survey was for a 0.7% increase ex-autos.

The threat of auto tariffs remains, but it is not imminent. Commerce Secretary Ross, who apparently is advocating tariffs, suggested that the half of the US trade deficit that is not accounted for by China can be traced to auto and light trucks. These imports accounted for about $190 bln last year, with Canada and Mexico accounting for around half. The National Automobile Dealers Association estimated that a 25% tariff on autos would boost the cost of domestically made cars by as much as $2270 and foreign made cars by $6815. It is almost as if the US is forcing Japan and Europe to accept “voluntary export restrictions” (which were acceptable under GATT but not the WTO) or face involuntary ones.

The US is expected to report a recovery in April housing starts and permits after declines in March. The Philadelphia Fed survey for May is due. A firm report like yesterday’s Empire State survey may temper the pessimism. Canada reports its monthly international transactions report, which is like the US TIC data. Foreign investors sold C$20 bln of Canadian securities last December, the most since 2007, but have bought C$40 bln in the first two months of 2019. Mexico’s central bank meets today and is widely expected to leave the overnight rate target at 8.25%.

The US dollar was turned back yesterday after it approached the upper end of its recent range near CAD1.35. It is now challenging the lower end of the range near CAD1.34. We had suggested that firm prices and strong employment report would likely underpin the Canadian dollar when the other two main drivers were not offsetting the macro story. The other two forces were the risk appetite (using the S&P 500 as a proxy) and oil prices. The intraday technicals warn that the losses in Europe have left the greenback overextended. The dollar recorded an outside down day against the Mexican peso yesterday, and follow-through selling has pushed the greenback below MXN19.00 for the first time since last week. Once again, it looks like players took sold into dollar weakness and the peso remains a favorite amid high yields and a relatively strong currency. Initial support for the dollar is seen near MXN18.90.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,China House Prices,EUR/CHF,Eurozone Trade Balance,Japan Producer Price Index,newsletter,tic,Trade,treasuries,USD/CHF