Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

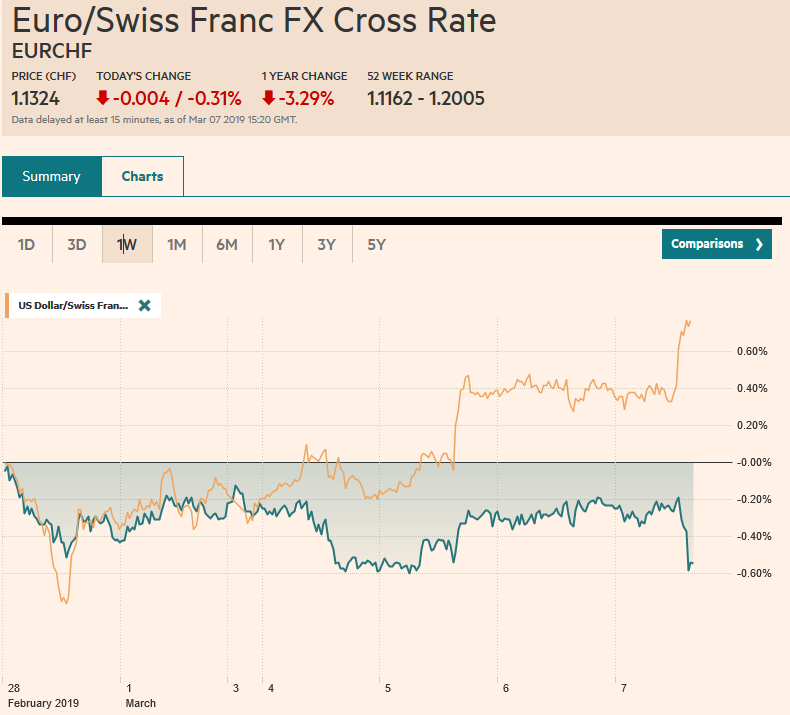

Swiss FrancThe Euro has fallen by 0.31% at 1.1324 |

EUR/CHF and USD/CHF, March 07(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The ECB meeting is today’s highlight. A dovish signal is expected. The euro remains pinned near its lows ahead it. The global equity market rally in January and February is faltering this week. Asian equities were mixed, but the Nikkei eased for the third consecutive session. Although the Shanghai and Shenzhen Composites eked out small gains, the CSI 300 tumbled more than 1% to nearly halve this week’s gains. Europe’s Dow Jones Stoxx 600 is trading lower for a second session. The S&P 500 is taking a three-day losing streak into today’s session, where it is poised to open lower. The S&P 500 has fallen in six of the past seven sessions. US 10-year yields are lower for a fourth session. After rising 10 bp last week, the benchmark yields is seven basis points lower this week. Asian yields slipped, but European yields are slightly firmer. The foreign exchange market is calm. The dollar-bloc is consolidating yesterday’s loss and posting small gains. While the greenback has a lower bias, sterling is struggling amid the growing realization that nothing has come from the EC-UK last-minute negotiations. |

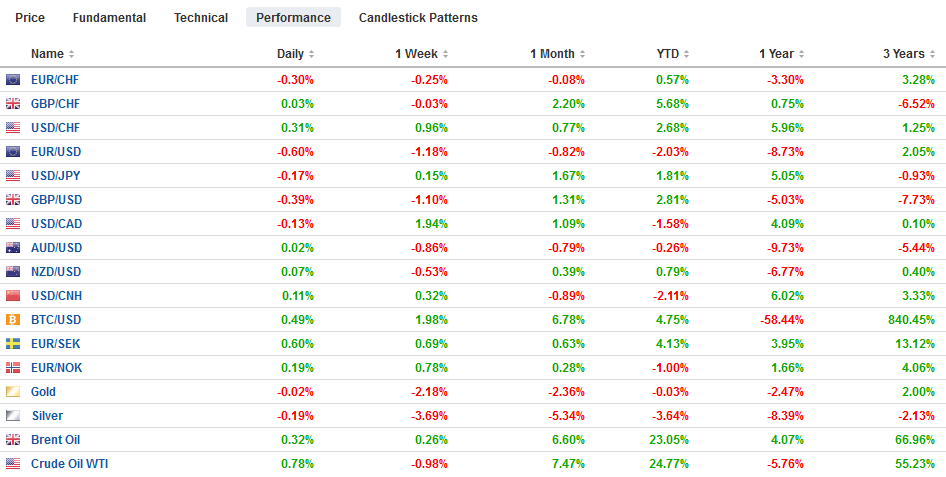

FX Performance, March 07 - Click to enlarge |

Asia Pacific

Nearly every day the media repeats the official claims that the US-Chinese trade talks are making progress. But details are lacking. All that seems to be agreed upon is China will buy more US goods (it looks like agriculture and energy, but higher-valued added goods, e.g., manufacturing are scarcely mentioned), and there will be monitoring discussions on various official levels. China will take some additional actions to protect intellectual property rights. It has officially indicated its policy is a stable yuan, which the US also seemingly wants. There may be scope for China to revisit its support for industry, but can one imagine China complaining that the US government ownership of the housing market, through the nationalization of Fannie and Freddie is an unfair encroachment in the private sector and distorts the competitive landscape? Or that the Export-Import Bank (sometimes derisively called the Boeing Bank) also gives an unfair advantage. We suspect that a trade deal may prevent an escalation of tit-for-tat tariffs but may not lead to a full dismantling of existing tariffs immediately.

Japan reported its leading economic indicator fell to 95.9 in January from 97.5 in December. It matches the low from May 2016. The economy is off to a weak start in 2019. Tomorrow, Japan is likely to announce that the economy grew a touch faster than the 0.3% estimate in Q4. Due to stronger business investment, Q4 GDP may have expanded at a 0.4% annualized pace (the same as Canada). Japan is also expected to report a small current surplus for January. It will mask a significant deterioration in its trade balance. The trade deficit is expected to swell to its largest in five years. The current account surplus is driven by investment income (interest/dividends/ royalties, licensing fees, etc.). Note that the US-Japanese trade talks are expected to formally begin later this month.

The dollar’s four-week climb against the yen is under threat. The greenback has stalled around JPY112. For the four sessions, it has finished the North American session between JPY111.75 and JPY111.90. It slipped to new lows for the week today, just below JPY111.60. There are two chunky sets of option expiries that may also stymie the price action. There are $1.24 bln in options struck between JPY111.50 and JPY111.75 that will be cut. There is another roughly $1.58 bln in options between JPY112.00 and JPY112.05. The intraday technical indicators suggest an initial push higher in North America is likely. The Australian dollar is consolidating yesterday’s decline. Yesterday’s lows near $0.7020 held. The Aussie saw it highs in Asai near $0.7050 but has in narrow ranges in Europe. While lower levels are still likely, the short-term players appear to have turned more cautious given the proximity of $0.7000. The dollar has slipped below CNY6.70 last week and early this week, but for the second consecutive session has remained above this level, which we had understood Chinese policymakers hinting at the limit of yuan appreciation.

Europe

Today’s ECB meeting has been anticipated since at the last ECB meeting the risk assessment was altered without updated forecasts in an unprecedented move that expressed urgency and concern. There are three elements that investors will focus on today. First, the staff forecast will play catch-up to the official change in the risk assessment. Growth this year will likely be cut from 1.7% to 1.2%-1.4% while inflation will likely be shaved from 1.6% to 1.4%. The extent of the concern will also be evident in the changes to forecasts for 2020 and 2021. Negligible changes in the future years will show officials still putting much trust hope in the improvements in the labor market to underpin growth and prices. Second, the ECB could adjust its forward guidance. It currently says it will not raise rates until after this summer. However, the market has already pushed interest rate expectations into next year. The ECB is under no urgency to confirm or validate the market’s move, but it could, and this would also underscore the dovishness of today’s hold. Third, the ECB could commit to a new long-term lending facility for midyear without revealing the “modalities” yet. Failure to do so, at this juncture, would disappoint market participants.

As was widely foretold, the last minute UK-EC talks about the backstop has not changed anything. The vote in the House of Commons on the Withdrawal Bill is slated for Tuesday. The EC has given the UK until the end of business tomorrow for new proposals. Alas, the cupboard is empty. Any important proposal would have already been made. This sets up for another defeat of the Withdrawal Bill next week. The following day (Wednesday), the House of Commons will also likely reject leaving with no deal. Then (Thursday) it votes on seeking an extension. This seems to be the path of least resistance, but in a pique, this bill could also fail to secure a majority. Stay tuned.

The euro has typically fallen on ECB meeting days over the past year, with last September being the exception that proves the rule. The euro has struggled to spend time above the middle of the $1.13-$1.15 ranges that has confined the bulk of the price action over the last few months. The short-term and speculative market is going into the ECB meeting short euros. The fact that the US reports the February jobs data may complicate the extent of the price action that is sustained today. We continue to favor continued range trading, even if the range frays a bit. There is an option for 2 bln euros struck at $1.1250 that expires today and another large one there tomorrow. On the upside, there are also 2.8 bln euro in options struck between $1.1360-$1.1375. Could these option strikes mark today’s potential range? Since closing below $1.32 on Monday, sterling has been unable to resurface above it in subsequent trading. The week’s low was near $1.31, and if this support fails, another half-cent decline is likely.

America

The central banks of the US and Canada were dovish yesterday. The Fed’s Beige Book downgraded growth to “slight to moderate” from “modest to moderate.” These nuances are significant from the Fed’s vantage point. About half the districts attributed some of the slowing to the government shutdown. Some noted that the poor weather may have dampened consumption. This is feeding speculation that the Fed forecasts (dot plot) will be cut. However, in some ways, the news is not surprising. Although Q4 growth held up better than expected, the soft patch is widely expected to have deepened in Q1. However, even now there is some evidence that the economy has begun getting better traction. A day before the Beige Book, the non-manufacturing ISM rose sharply to stand at a three-high, for example. Later today, the US will report January consumer credit. It is expected to have expanded by about $17 bln. In January 2018, it rose by $12.2 bln.

Many were puzzled by the abrupt reversal of Fed policy. Bank of Canada has reversed nearly as quickly. Bank of Canada Governor Poloz has gone from declaring that economy no longer required stimulus late last year to monetary accommodation is still needed yesterday. Next month, the Bank of Canada may lower its assessment of neutrality, which currently stands 2.50%-3.50%. The cash rate is currently at 1.75%. The market is reluctant at this juncture to price in a rate cut. Interpolating from the OIS, it looks like about a 10-12% chance of a cut is discounted.

Mexico reports February CPI figures today. The year-over-year pace is expected to fall below 4% for the first time since the end of 2016. With the economy slowing, lower price pressures are needed for the central bank to ease policy. While the OIS has yet to show it rate cut expectations, the Cetes have rallied, and while the overnight rate is at 8.25%, the one-month Cetes yield about 8.05%.

The Canadian dollar was sold in response to the dovish sounding central bank. It surpassed the CAD1.3440 technical target to rise to almost CAD1.3460. It is consolidating today in narrow ranges. Support may be seen near CAD1.3375. A soft inflation report and the risk-off mood could see the dollar test the mid-February high near MXN19.47. The year’s high is closer to MXN19.77. For its part, the Dollar Index remains within Tuesday’s range (~96.65-97.00). The S&P’s are struggling to sustain the upside momentum. The 20-day moving average is found near 2766. The S&P 500 has not closed below this moving average since January 4. A close below it would suggest corrective potential toward 2733-2750 in the near-term.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF and USD/CHF,MXN,newsletter,SPX