Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

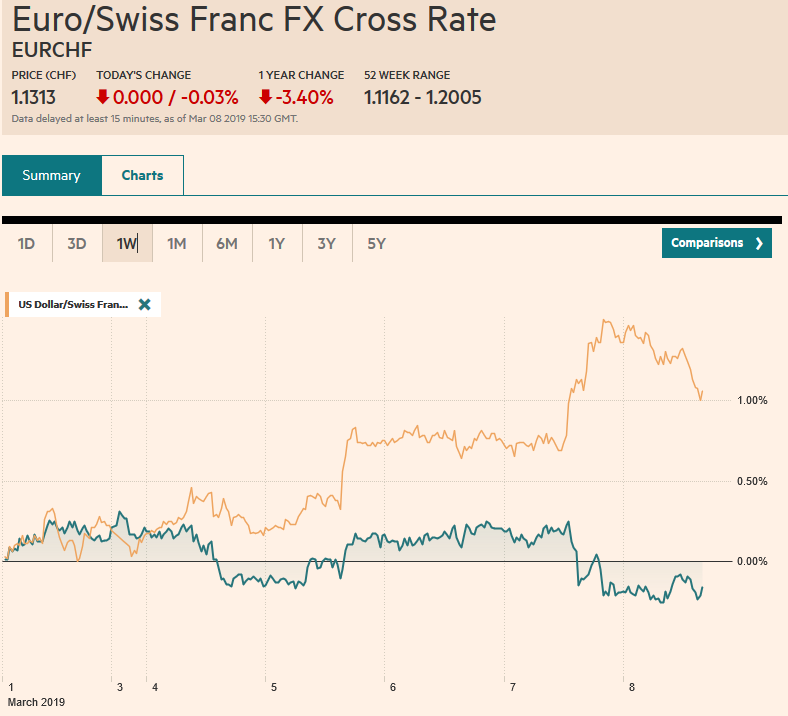

Swiss FrancThe Euro has fallen by 0.03% at 1.1313 |

EUR/CHF and USD/CHF, March 08(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A weak economic assessment in the Beige Book and an ECB that slashed growth forecasts have been followed by news of a nearly 21% slump in China’s exports have marked the end of the dramatic equity rally that was seen in the first part of 2019 after the sharp losses late last year. The Shanghai Composite dropped 4.4%, the largest fall in six months, ending the eight-week rally with a 0.8% decline. All the markets in Asia were lower. It is the second consecutive weekly loss for the MSCI Asia Pacific Index. European markets are falling and the Dow Jones Stoxx 600 is off for the third day. This week is the second of the year that this regional benchmark is lower. The S&P 500 has fallen for seven of the last eight sessions. It closed below the 20-day moving average for the first time since January 4 and below its 200-day moving average for the first time since February 11. Growth concerns and weak equities keep Asian and core European yields soft. US 10-year yields have moved lower every session this week and are a little lower now. At 2.63%, the yield is off 12 bp this week, the most since the first week last December. The US dollar is consolidating yesterday’s gains, giving it a softer profile. The yen appears to have been lifted by the weaker stocks and lower yields. Its four-week drop is ending. US and Canadian jobs data are the highlight before the weekend. After the markets close, Powell will discuss monetary policy and note that the Fed Chair will be on “60-Minutes” this Sunday. |

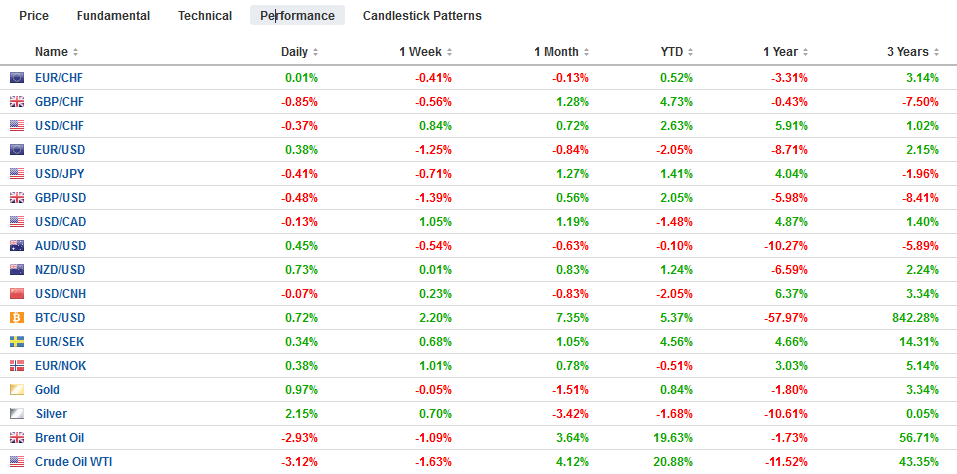

FX Performance, March 08 - Click to enlarge |

Asia Pacific

With China’s National Party Congress endorsing a large stimulus program, including about a $300 bln of tax and fee cuts, officials may feel a bit bolder to resist US pressures. Recall, last year, the US fiscal stimulus was understood to give it a cushion to absorb the disruption spurred by the Trump Administration’s more vigorous pursuit of economic nationalism. Now the shoe may be on the other foot. Reports yesterday claimed Chinese officials were wary of a quick trade deal and did not want to commit to US structural demands. Also, given the unpredictable element and last minute demands of the “art of the deal,” there may be some reluctance for President Xi to come all the way to the US without knowing a deal is in hand. The risk of the loss of face (see US walk away from North Korea) may not be acceptable.

China reported a dramatic slump in February trade. The surplus shrank to $4.1 bln from $39.2 bln in January. The Bloomberg survey found a median forecast of $26.2 bln. Exports fell 20.7%, while imports were 5.2% lower. The Lunar New Year distorts the data, Some economists suggest looking at January and February data combined, though we are not sure that offers a “clean” read. Still, the trade figures would see to reflect domestic economic weakness, which makes sense given the other data and the aggressive action by officials.

Japan reported upbeat news. First, it revised up Q4 GDP from 1.4% at an annualized pace to 1.9% (0.5% rather than 0.3% on the quarter). Economists had forecast a revision to 1.7% on the back of improved capital expenditures. Second, it reported that overall household spending jumped 2% in January (year-over-year) from 0.1% in December. Economists were looking at a 0.5% decline. Third, Japan’s January current account surplus was larger than expected, helped by a smaller than anticipated trade deficit. However, note that on a balance of payments basis, Japan’s trade deficit was the largest in five years.

The dollar briefly slipped below JPY111.00 late in the Asian session but has stabilized in the European morning. It has not closed below its 20-day moving average (~111.00 today) since January 31. The initial retracement objective of the rally off that late January low is seen near JPY110.75. There are nearly $1.9 bln in expiring options struck between JPY111.50 and JPY111.65, which may now offer resistance to the greenback rather than support, which had looked likely previously. The Australian dollar has held psychological support at $0.7000 thus far today. An option for A$1.5 bln struck there expires after the US jobs report today. The $0.6950 area corresponds to a 61.8% retracement objective of the gains off the January 3 flash crash.

Europe

The ECB over-delivered a dovish message. The cut in the growth forecast was not only deeper than expected but next year’s forecast was shaved as well. And to drive home the point, as well as a compromise with those who are even more pessimistic, warned that the risks remained to the downside. The ECB extended its forward guidance to indicate it will not raise rates before the end of the year. Some officials wanted to extend the pledge through Q1 20. It also committed to a new TLTRO, whose initial details are less favorable the previous rounds. The term will less (two years rather than four), and the rate is tied to the main refinancing rate (now zero) rather than the deposit rate (minus 40 bp). European banks were sold on the news. Yesterday’s 3.3% drop in the Stoxx bank index had been followed by today’s 1.1% decline. For the week, this is a 5% loss and ends a three-week advance. The 10-year German Bund yield that finished last week a little above 18 bp is not around five bp, the lowest since Q4 16.

Outside of Germany, economic data today has surprised on the upside. Consider France. January industrial output rose 1.3%. The market was expected around 0.1%. Manufacturing output rose 1.0% compared with expectations for a small decline. Spain reported January industrial output surged 3.4% (month-over-month), which was a little more than twice what the median forecast in the Bloomberg survey anticipated, while the December fall was revised to -1.2% from -1.4%. Beleaguered Italy also the party. January industrial product jumped 1.7%. The median forecast was for a 0.2% increase after the December series was revised to -0.7% from -0.8%. Germany reported a disappointing drop in January factory orders. The 2.6% decline contrasts with the median guesstimate of a 0.5% gain. Still, some of the sting eased with the December revision to +0.9 from -1.6%.

The EC seemed to offer a half-hearted revision to the review of the Irish backstop, but this is likely too small to see the Withdrawal Bill win House of Commons support next week. Some sort of extension still seems to be the most likely scenario. However, an extension of the exit is an extension of uncertainty that is not good for business or investment.

The euro was sold to almost $1.1175 yesterday, the lowest level since June 2016 on the back of the more dovish ECB. It is consolidating those losses today in a narrow range of about 15 ticks on either side of $1.1200. There is an option at $1.1150 for 633 mln euros that expires today. There is a roughly 680 mln euro option at $1.1225 and 2.6 bln euro at a $1.1250 strike that also expires today. While we have been bearish the euro, we did not anticipate a sustained break of the range this week. The ECB’s measures, which Draghi suggested were “small steps” in a dark room “with pervasive uncertainty” was much bolder than expected. The euro has fallen for five consecutive sessions through yesterday and is posting small gains ahead of the US jobs report. Sterling is also consolidating yesterday’s loss. The $1.3060 area is important from a technical perspective. It houses the 20-day moving average, which sterling has not closed below since February 18, and the 50% retracement of the rally since mid-February. There is an option for about GBP380 mln struck at $1.30, a little above the 61.8% retracement of that advance.

America

The US employment data remains arguably the single most important monthly report. It sets the tone for the rest of the month’s data. There are three elements of the report that investors typically focus on job creation (establishment survey), unemployment rate (household survey) and average hourly earnings. The median expectation is for 180k net new jobs, an unemployment rate slipping to 3.9% from 4.0% and a 0.3% increase in average hourly pay, which would lift the year-over-year rate to 3.3%.

There is little doubt that the US economy slowed further in Q1. The government shutdown was cited in the Beige Book as a factor as was the cold weather. The government re-opened and from High Authority, spring is coming. Ideally, investors will begin seeing better data, but they seem to be looking past Q1. That said, the housing market, which buckled last year under seemingly affordability issues, may find better traction. Housing starts are expected to have bounced back in a big way (10%+) in January. A robust jobs report will underpin expectations that the US soft patch does not morph into a recession.

In contrast, Canada is expected to report softer housing starts and a flattish jobs report. After growing nearly 67k jobs in January, jobs growth is expected to have slow to a trickle in February, with the median forecast for a 1.2k increase. Wage growth is expected to have slowed a little (1.7% from 1.8%). Such a report would reinforce the shift in market expectations this week. At the end of last week, the market appears to be pricing in practically no chance of a cut this year, and many had been favoring another hike in H2 19. Now the market is pricing in almost a 1 in 4 chance of a cut this summer.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF and USD/CHF,newsletter,SPX