Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

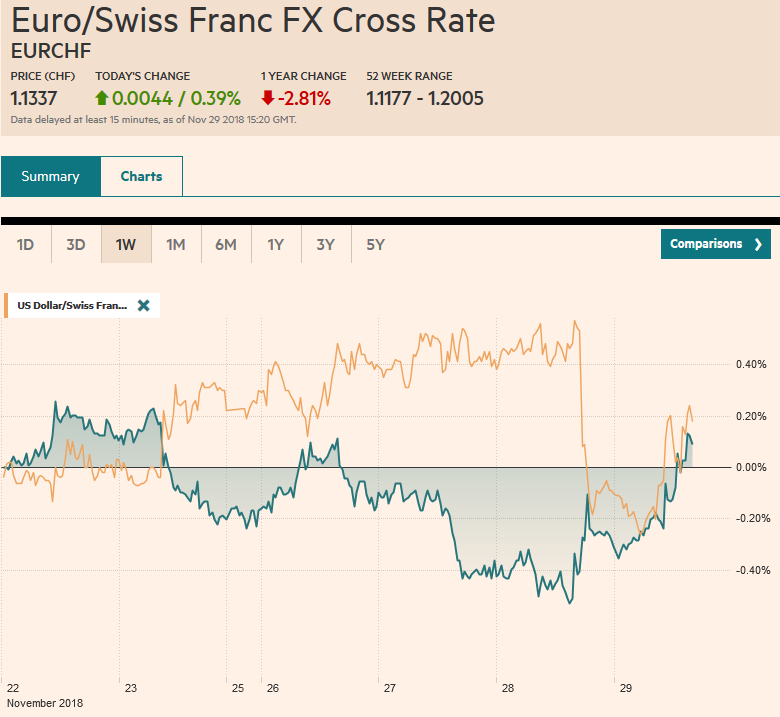

Swiss FrancThe Euro has risen by 0.39% at 1.1337 |

EUR/CHF and USD/CHF, November 29 Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The biggest US equity advance since Q1 has helped lift global markets today. The MSCI Asia Pacific Index rose for the fourth session, and nearly all the bourses in the region rallied with the notable exception of China and Hong Kong. Almost all the sectors in Europe are rallying but energy and real estate. US oil inventories rose three times more than expected and Putin expressed little support for fresh output cuts. February Brent is slipping below $58 a barrel, and January WTI is making new lows below $50 a barrel. Bond yields are falling, and the US 10-year yield is dipping below 3% for the first time since decisively moving above in mid-September. The dollar is mixed after yesterday’s reversal, but among the majors, only the yen and the Australian dollar have extended yesterday’s gains. Emerging market currencies are mostly higher, led by the Turkish lira and the South African rand. |

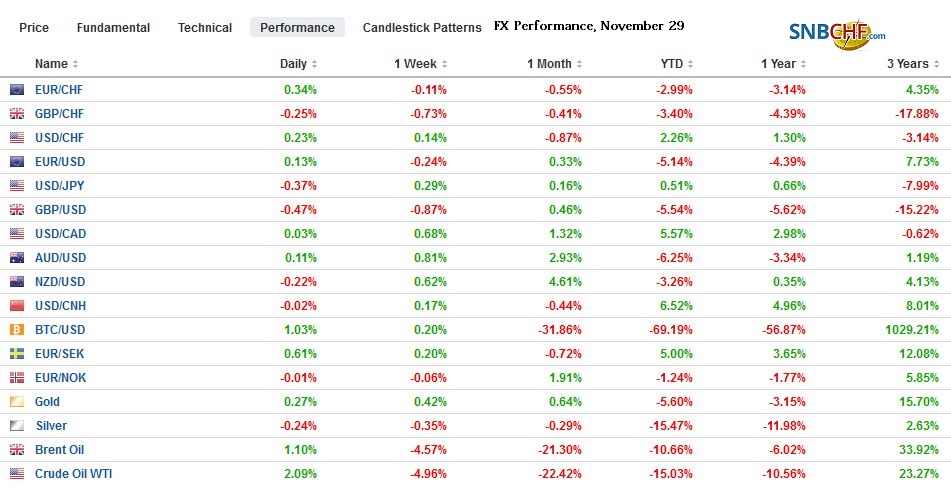

FX Performance, November 29 - Click to enlarge |

North America

The S&P 500 gapped higher yesterday and was near opening levels when Powell took the stage in NY. Contrary to some accounts, Powell did not say rates were just below neutral. He said that the fed funds rate was just below the broad range of estimates of the neutral level. Those estimates as of the September forecasts were 2.5%-3.5%.

Powell’s comment then should not be considered forward guidance, but a simple observation, which we suspect was meant to correct his remark from early October that seemed to emphasize that policy was still very accommodative as the target rate was still well below neutral. Rather than being contradictory, both statements are correct if you grant that Powell first referred to the median forecast of the neutral rate and in NY specifically referred to the range.

The December hike will put the upper end of the target range at 2.50%, the lower end of the range of views of neutrality. That does not mean policy is neutral. It means that the most pessimistic Fed officials see it as neutral. The median is 3.0%. At the December meeting, the newly sworn-in Governor Michelle Bowman will also provide forecasts, and she is thought to add to centrist views, which is to follow the Fed’s leadership.

The upper end of the current target range is three hikes from the median estimate of neutrality. This fed into our view that the Fed to pause in the middle of next year after hiking rates in December and twice in H1 19. The Fed itself signaled its anticipation of slowing its pace of hikes next year. This year it anticipated four hikes and next year three.

The implied yield of the December 2019 fed funds futures contract fell yesterday reflecting the more dovish interpretation of Powell’s comments than argued here. However, when the implied yield slipped only half a basis point below the low seen last week. Moreover, at 2.70%, it is 50 bp on top of the current effective fed funds rate of 2.20%. That would seem to imply two, not one, more hike. And if the Fed widens the gap between the interest paid on reserves (required and excess) and the top of the fed funds target range, then arguably more than two hikes are discounted.

There is much on tap in the US today. The personal income and expenditure data for October will give investors a better sense of how the economy has begun Q4. The inflation measure is expected to be mixed with the headline rate maybe rising to 2.1% from 2.0%, while the measure the Fed targets, the core rate, may slip to 1.9% from 2.0%. Weekly jobless claims will also be reported. It tends to be noisy. However, ahead of next week’s national report, it may draw some attention. Recall that weekly jobless claims have risen for the past two consecutive weeks for the first time since July. With other evidence of late-cycle behavior, weekly jobless claims may also be carving out a bottom. Later this afternoon, the FOMC minutes from the November meeting will be released, and around the same time, six regional Fed presidents will speak at a Boston conference. The S&P 500 stalled in front of the 200-day moving average (~2761.5) and is an important psychological metric.

Canada reports Q3 current account figures today and GDP tomorrow. Growth is expected to have slowed to from nearly 3% in Q2 to 2% in Q3. The Bank of Canada meets next week, but no action is expected until Q1 when the market has about a 75% chance discounted. The US dollar made a new five-month high against the Canadian dollar yesterday near CAD1.3360 before reversing lower. However, there was no follow-through to the downside, and the greenback is knocking on CAD1.33.

Europe

The euro snapped a three-day slide yesterday, posting a bullish outside up day, but has stalled at a retracement objective a little below $1.14. An option there for almost 785 mln euro expires today. The next chart point is near $1.1425, and a move above there could see $1.1475. In between those two points ($1.1450) is a nearly 600 mln euro option that also expires today. On the downside, there are 2.32 bln euros in options struck at $1.1345-50. Separately, there is a nearly 500 mln euro option at GBP0.8860 that will be cut today.

There are several macro developments to note today. First, although German reported an unexpected decline in unemployment (5.0% from 5.1%), investors are more interested in the preliminary inflation figures. The states are mostly reporting slower price increases and Saxony, the only state to report a core rate, saw some slippage. The national estimate will be reported shortly. Spain also reported soft November CPI (1.7% vs. 2.3%). The preliminary EMU-wide figures will be released tomorrow.

Separately, the German and Italian economies were not the only European economic contractions in Q3. Today, Sweden reported its economy contracted by 0.2% in Q3. Economists had expected an expansion of the same magnitude, and adding insult to injury, Q2 growth was shaved to 0.5% from 0.8%. The weaker growth supports the doves at the Riksbank, which meets on December 20. Switzerland also reported an unexpected 0.2% contraction in Q3. There, economists had been looking for a 0.4% expansion. Trade appears to have been a significant drag.

Sterling recovered a little more than a cent on the back of the greenback’s weakness yesterday. For the past six sessions, it has been in a sawtooth pattern-alternating between gains and losses. If the pattern is going to hold, sterling should fall today. Like the euro, it also stopped at a key retracement level near $1.2850. The next hurdle is seen in the $1.2880-$1.2900 range. There are two expiring options to note: GBP215 mln at $1.2780 and about GBP565 mln at $1.2830.

The take away from the Bank of England’s stress test and assessment of the impact of an exit from the EU without an agreement was fairly straight-forward. The banks are strong enough, it says, to withstand such a disruptive event that could see sterling depreciate by a quarter, and the economy to shrink by as much as 8% over the following year and nearly a 30% decline in house prices. Prudence dictates that when assessing adverse scenarios, those worst cases need to be considered. Like gamblers, investors and business are best advised to avoid the risk of ruin. On the one hand, the BOE has been criticized for fear-mongering, the same way the US study, apparently disowned, on climate change was criticized for examining some worst-case scenarios. On the other hand, informed decision-making and risk assessment require that kind of thinking.

Asia Pacific

The Japanese economy contracted n Q3, and it is part of the global slow down story. However, the weakness was spurred by natural disasters, and the rebuilding should help the economy grow again here in Q4. October retail sales jumped 1.2%, the most in six months and this may in part be flattered by the replacement of goods. The year-over-year rate rose to 3.5%, the fastest this year.

The yen is the strongest of the major currencies, seemingly more sensitive to the decline in rates than the rally in stocks and the rebound in emerging markets. The dollar initially pushed above JPY114 yesterday for the first time in a couple weeks before turning lower to dip below JPY113.50. Today, the greenback has eased to almost JPY113.20, where it appears to be basing. It corresponds to a 50% retracement of the advance from last week’s lows. There are $1.44 bln in options expiring between JPY113.35 and JPY113.50 today. The Antipodean currencies remain firm near yesterday’s highs.

The Chinese yuan remains remarkably stable, as many expected ahead of the meeting of the presidents. The Trump Administration is playing a different set of tactics. It is ratcheted up its rhetoric and threats. This includes the publication of Lighthizer’s damning report and the new look into China’s retaliatory tariffs on US autos. Previously, we noted that GM sold more cars in the first nine months of the year than it did in the US and that these were not exported, but assembled locally. European car companies producing in the US and exporting to China are the ones caught in the retaliatory tariffs. Meanwhile, the US is again threatening to impose 25% tariff on imported vehicles.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$CHF,$CNY,$EUR,Federal Reserve,newsletter,SPX