Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.13% at 1.1415 |

EUR/CHF and USD/CHF, November 09(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The US dollar’s gains scored in the wake of the Fed’s signal that will continue on course to gradually hike rates have been extended. Most emerging market currencies are lower as well. Equity markets are heavy. Bond yields in Europe and US are a little lower, with the exception of Italian bonds. The concern about the clash between the EC and Italy is nearing an inflection point as Italy’s formal response is due next week and the government is not prepared to back down. Oil prices continue to trade heavily amid strong supply indications. A decline today would extend the streak to ten sessions, the longest losing streaks in last thirty years. Prices have dropped more than 20% since early October. OPEC countries meet in Abu Dhabi this weekend. If quotas are to be re-introduced, this weekend’s meeting is not the likely forum, though intentions and sentiment will be important. |

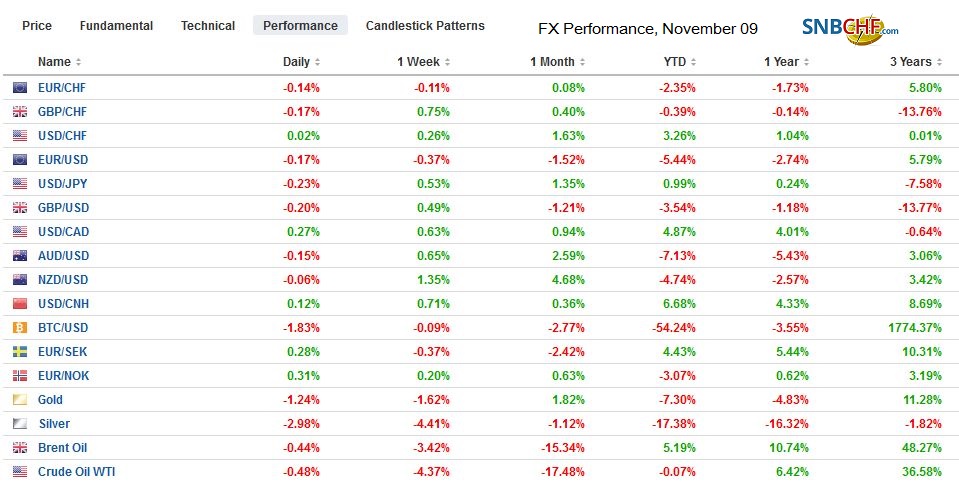

FX Performance, November 09 - Click to enlarge |

North America

As universally expected the Federal Reserve did not change policy yesterday. Its assessment of the economy was essentially unchanged. Growth is strong. Unemployment is low. Inflation and inflation expectations stable. Gradual hikes will continue. Barring a major shock, which is more than a correction in the stock market, the Fed will raise rates in December.

The tensions in the money markets will continue until at least the December FOMC meeting. Some are disappointed the Fed did not act now to reassert control over rates as some repo rates have traded above the upper end of the fed funds range. Bloomberg reporters have emphasized the role that unwinding the balance sheet may be having. Their solution is to slow down the unwind, not because of the economic impact but because of the technical consequences. What is less understood is the Fed’s response. In the minutes from the September FOMC meeting, the Fed pushed back against that hypothesis which is being treated as a fact. Fed officials argue that the increase in bill issuance (and therefore settlements) coupled the rising rate environment and technical development in other repo markets appear to be the main culprits.

The Federal Reserve is not oblivious to the problem. In September, it introduced a spread (five basis points) between the interest it pays on reserves and the top of the fed funds range. Although it is common to describe what the Fed pays as interest on excess reserves it obscures the fact that the Fed pays interest on required reserves too. Paying interest on reserves at all is post-crisis development in the US. The Fed has not indicated the end point of its balance sheet unwind. The bar to changing the unwinding of the balance sheet seems high, and the Fed is more likely to widen the spread between spread between the interest it pays on reserves and the upper end of the fed funds rate again.

The US reports October producer price and the University of Michigan’s consumer sentiment and inflation expectations survey. Although economists can tease out some insight for consumer prices from the PPI, it is not typically a market mover. It has been a busy week for US participants, with the midterm election and the FOMC meeting behind them, participants welcome the weekend. The Fed’s Williams and Quarles speak in the morning now that the quiet period ahead of the FOMC meeting has ended, while the Fed’s first formal report on Supervision and Regulation will be released. The Dollar Index is up about 0.35% on the week (@96.85). If the gain is sustained, it will be the sixth gain in the past seven weeks. The high for the year was set at the end of October near 97.20. Our next text is around 98.00.

The Canadian calendar is also light. Watch USMCA (NAFTA 2.0) negotiations as the final language is adopted, and in the process, it is not uncommon for parties to push for little concessions. Some attributed the Canadian dollar losses yesterday to disputes about foreign wines in British Columbia and whether it applies to Ontario and Quebec as well. There are also some efforts in the dairy-specific too. Meanwhile, with the steel and aluminum tariffs still in effect, Prime Minister Trudeau has threatened not to attend the signing ceremony.

Asia

Here in the second half of 2018, the Chinese yuan has appreciated against the dollar in only three weeks, and this past week was not one of them. The dollar rose about 0.8% against the yuan this week. It was the largest move since late July. The question is what is fueling it. Many observers seem to attribute responsibility to Chinese officials managing it. However, we suspect if it were to float, the currency would fall further and faster. The US now pays a premium over China to borrow for two years. The 10-year premium China offered has collapsed from over 170 bp at the start of the year to 25 bp now. The Chinese economy is slowing.

Some measures that Chinese officials are taking also does not bolster investor confidence. The initiative unveiled today introduces quotas for large banks lend to the private sector. This plays on concerns about the bad loan problem in China, and bank stocks fell sharply today. The initiative overshadowed the release of the October CPI (unchanged at 2.5%) and the decline in producer prices (3.3% vs. 3.6%).

On trade, even though top Chinese officials signal they want to talk and find a compromise, the US does not seem in the mood to find a compromise. Indeed, the US may open another front in the trade conflict by seeking redress to the violation of a 2015 pact that prohibits electronic theft of intellectual property.

The US dollar has risen about 0.6% against the Japanese yen this week. It is the second consecutive weekly gain and the third in the past four weeks. The dollar briefly traded above JPY114.00, for the first time in a month today. There is a $1.2 bln option struck there that is expiring today. Another option at JPY114.20 for about $570 mln will also be cut. On the downside, there are also $3.1 bln in maturing options between JPY113.50 and JPY113.75.

Europe

After peaking at $1.15 in the middle of the week, its best level since October 22, the euro has been sold back toward the lower end of its range, reaching almost $1.1325 in the European morning. The market looks reluctant to push it through the $1.1300 base ahead of the weekend, where a 1.1 bln euro option will be cut. There are also 1.86 bln euros in options in the $1.1340-50 range and another 3.8 bln euros in expiring options stacked in $1.1375-$1.1400 area.

Italy’s debt and UK’s Brexit are the talking points today. Italy is pushing back against the EU’s claim that Italy will not grow as fast as the government project and that borrowing costs will climb and the deficit will be more than the government forecasts. The EU’s forecast for 2019 growth is 1.2% rather than the government’s 1.5%, and even this may be a bit optimistic. The EU forecast shows next year’s budget deficit would be near 2.9% of GDP and then 3.1% in 2020. Italy is due to formally respond to the EC’s request for revisions in its budget proposals early next week. Barring such changes, the EC will likely begin excess deficit proceedings.

The Irish border continues to vex the EC and UK negotiators. It looks as if the closer the EC-UK get to an agreement, the more challenging the domestic situation becomes. The Tories depend on the Northern Irish unionists, and they are balking at any proposal that treats Northern Ireland different than the rest of the UK. Prime Minister May appears to be banking on delivering a fait accompli to parliament. They either give approval to the plan negotiated with the EU (which is not final yet) or leave the EU without an agreement and transition phase.

The slew of UK data seemed to little importance to market participants today. Quarterly growth accelerated to 0.6% from 0.4% in Q2. The trade balance improved markedly. Employment and CPI for October will be reported next week. Sterling is holding on to about a 0.3% gain this week (@$1.3010), and that is with about a 0.8% pullback between yesterday and today. A convincing break of $1.30, where a GBP240 mln option will expire today, could see sterling slip toward the $1.2950 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,newsletter,USD/CHF