Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

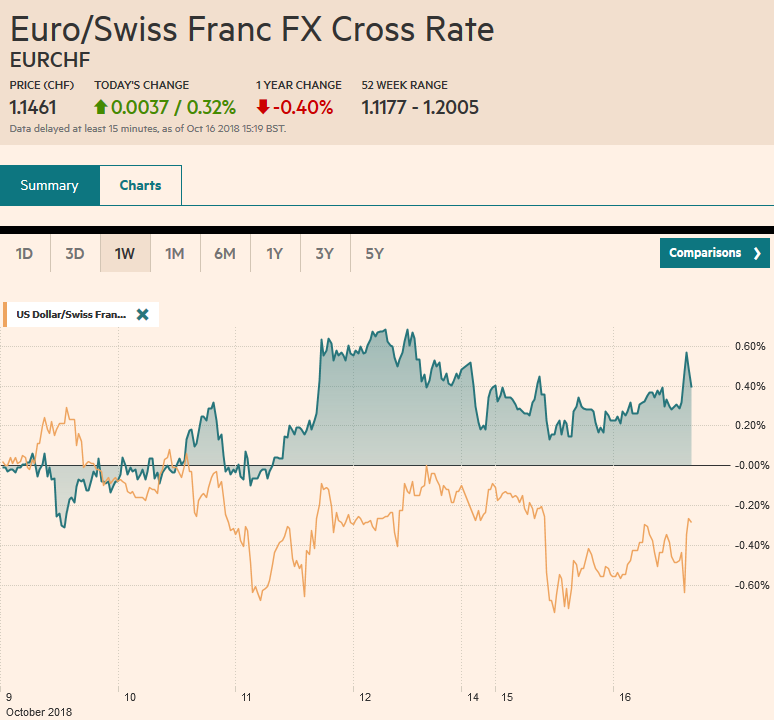

Swiss FrancThe Euro has risen by 0.32% at 1.1461 |

EUR/CHF and USD/CHF, October 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Although the S&P 500 was unable to sustain early gains yesterday, the largely consolidative session was part of the stabilization of equities after last week’s jump in volatility. Asia and European stocks are also cautiously steadying. Most Asia equity markets advanced with the Nikkei’s 1.25% advance most bourses higher. China was a notable exception, The Shanghai Composite recorded new lows for the year and finished uninspiringly on its lows. Europe equities are mostly firmer, led by Italy and Spain. The Dow Jones Stoxx 600 is almost 0.5% in late morning turnover, with most sectors participating save energy and consumer staples. Core bonds yields are one-to-two basis points higher, while peripheral European 10-year benchmark bond yields are two-to-five basis points lower, led by Italy and Greece. The dollar is mostly softer, and the softness of the Swiss franc and Japanese yen also reflect the easing of investor anxiety. Emerging market currencies are mostly firmer, led by the South Korean won (~+0.6%) and the South Africa rand (+0.5%). The Turkish lira is struggling to extend its seven-day advance. |

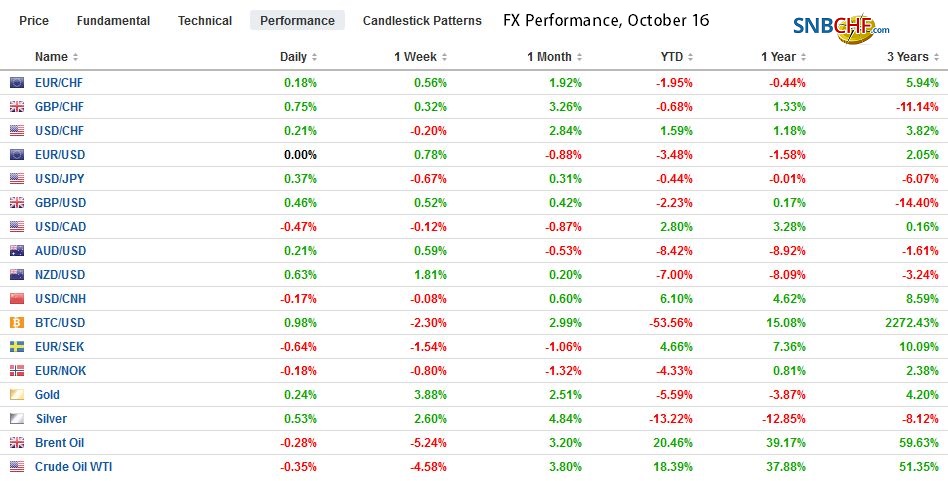

FX Performance, October 16 Source: investing.com - Click to enlarge |

Asia-Pacific: There were fourth economic reports of note. First was China’s inflation. Its September CPI rose 2.5% from 2.3% in August. It is about food prices, which more than doubled to 3.6% from 1.7% in August. It reflects weather-induced shortages and unfavorable base effects. It may also be a sign of counter-tariffs imposed by China amid reports that US soybeans are headed there to meet the shortage. Non-food prices eased to 2.2% from 2.5%, helped by slower increases in medical costs (increase has been more than halved since reaching 6% at the start of the year). Producer prices slowed for the third consecutive month to stand at 3.6% and peaked this year in June at 4.7%. The yuan remained confined in narrow ranges (with the dollar mostly CNY6.9150-CNY6.9250).

Second was the minutes of the Reserve Bank of Australia recent meeting. It essentially reiterated its stance. The weaker currency was a welcome development as it may help growth. Interest rates will continue to be held steady. It is closely monitoring the impact of weaker house prices on consumption, but it anticipates a firm Q3 GDP figure. Meanwhile, tomorrow the September employment report will be released. The Australian dollar continues to bump against a retracement objective and resistance in the $0.7145-$0.7150 area. If it does not succeed in establishing a foothold above it soon, short-term momentum players give up.

Third, stronger than expected inflation has lifted the New Zealand dollar to its best level in a couple of weeks near $0.6600. Consumer prices in Q3 rose 0.9%, up from 0.4% in Q3. This lifted the year-over-year pace to 1.9% from 1.5%. It is too soon to expect the central bank to consider hiking rates, though at 1.75% the cash rate is no longer positive after adjusting for inflation.

Fourth, Japan reported the final August industrial output figures were much weaker than the preliminary estimate suggested. Instead of rising of 0.7%, it only rose 0.2%. Shipments were also revised lower. It leaves industrial output up 0.2% year-over-year. Separately, the Abe government confirmed that it will put together a disaster-relief budget and reaffirmed its commitment to lifting the sales tax next year. The dollar continues to straddle the JPY112 area. Today there are approximately $3.3 bln in expiring options struck between JPY111.65 and JPY111.85. A move above JPY112.30-JPY112.50 would lift the technical tone.

Turning to Europe, two data points stand out: The UK’s employment report and the German ZEW survey. The UK’s jobs data were mixed. The job creation disappointed, but earnings growth was firmer than expected. The UK reported the first loss of jobs (three-months/three months) of the year in August with a 5k decline. It is the fifth consecutive month of deterioration. The unemployment rate was steady at 4% in August. The September claimant count rose to 18.5k, the most since April and it is the fourth consecutive increase. On the other hand, weekly average earnings unexpected ticked to up 2.7% in August from 2.6%, and 3.1%, excluding bonuses, from 2.9%, which represents a new cyclical high. Sterling briefly poked above $1.32, stopping well short of last week’s high near $1.3260. Support is seen around $1.3180 today.

The German ZEW survey results were miserable. The assessment of the current situation fell to 71.1 from 76.0. It unwinds the gains from the past two months to sit at its lowest reading since the end of 2016. The expectations component collapsed to -24.7 from -10.6. It has not been positive since March. Investors have not been this pessimistic since August 2012. The euro has flirted with the $1.1600 level with little satisfaction for the fourth session running. There continue to be expiring options there (~950 mln euros today). On the downside, there is a large (~1.3 bln euro) $1.1550 option that also expires today and may attract prices.

The US data calendar is chock full, with industrial output, JOLTS, and TIC data. Industrial output is expected to slow to 0.2% from 0.5% in August. Note that through August, the average monthly rise in industrial output has been almost 0.3%. Last year’s average was 0.25%. The JOLTS report is expected to reflect the robust labor market where there are more openings than measured unemployed and the among the least educated are being absorbed faster than before. The Treasury’s International Capital report for August is due. Through July, the TIC shows a monthly average of $95.6 bln of portfolio inflows into the US. This is more than twice the average for the same period last year (~$41.4 bln) or for last year as a whole (~$35.5 bln). The repatriation of earnings from overseas by US corporations appears to be playing a significant role.

The new San Francisco Fed President Daly is speaking today. Although she has written extensively, many market participants are not familiar with her views. Also, for the first time, the US will offer two-month T-bills today. There will be $25 bln of these new eight-week bills sold today and $40 bln in four-week bills. The Dollar Index is stuck in a narrow range. The recent lows have been set near the 100-day moving average (~94.85) while the high from last Thursday, when equities fell dramatically (~95.45) has been capping the upside.

Canada reports its monthly portfolio flows as the Canadian dollar looks content to consolidate within yesterday’s broad range (~CAD1.2950-CAD1.3050). It has tended to regain its composure after last week’s slide, encouraged by the more stable tone in equities. Support for the greenback extends to CAD1.2930, but with the Bank of Canada the next major central bank to lift rates, assuming the equity markets continue to stabilize, there may be potential for more of a recovery for the Canadian dollar.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF,newsletter,NZD,USD/CHF