Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

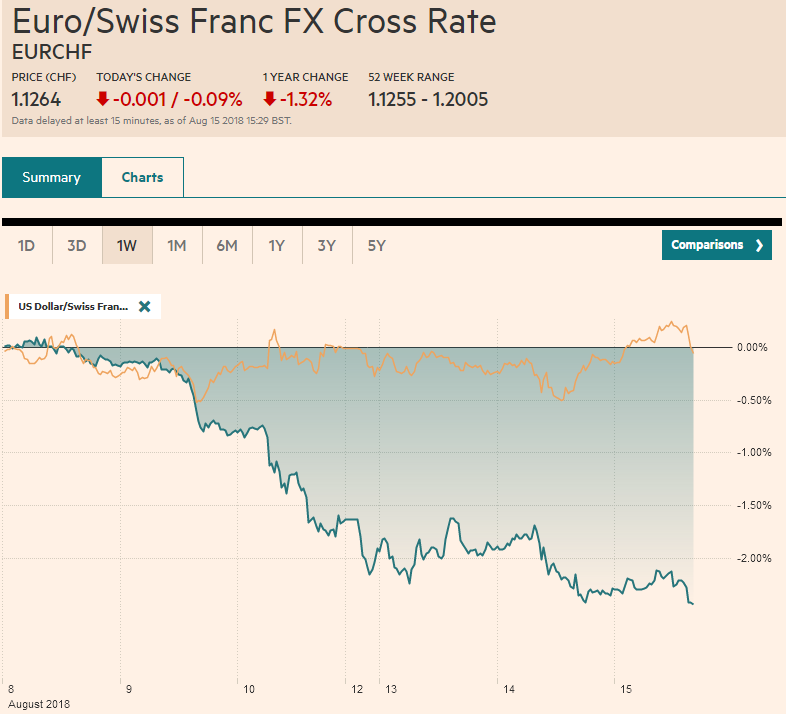

Swiss FrancThe Euro has fallen by 0.09% to 1.1264. |

EUR/CHF and USD/CHF, August 15(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe Turkish lira is extending yesterday’s recovery today on the back of actions by officials that are aimed at limiting foreign access to the lira to short. Without introducing new capital controls, regulators halved the amount of swap transactions banks can do to 25% of shareholder equity. This is meant to make it more difficult to access lira in the offshore swaps market, which is an important channel. The US dollar fell to TRY5.8830 before recovering toward TRY6.16. At the time of this writing, it is near TRY6.10, nearly four percent lower on the day after the 7.75% pullback yesterday. If the lira’s dramatic plunge hit other markets, its recovery appears to have gone largely unnoticed. Most other emerging market currencies are weaker, led by the South African rand (-0.6%), Polish zloty (-0.4%) and Russian ruble (-0.4%). That said, Indonesia hiked rates by 25 bp, making it a cumulative 125 bp increases since the end of Q1. Officials are thought to have intervened yesterday, and the currency strengthened slightly. The Hong Kong Monetary Authority intervened today to defend the lower end of its currency band and bought HKD2.158 bln. They had intervened (~HKD70 bln) in similar defensive posture by in early Q2 in almost 20 operations. In terms of flows, we note two developments. First, an estimated $90.4 mln flowed into the MSCI iShare Turkey ETF yesterday, which appears to be the most in at least a year, and was the third consecutive session of inflows (totaling a modest $161 mln) or around 5.7% of assets. Second, despite (or maybe partly because of) steep losses in South African bonds and the rand recently, investors flocked to yesterday’s debt auction. The ZAR2.4 bln of paper was oversubscribed by a factor of four, the most in nearly five months. The US dollar remains firm against the major currencies. The euro made new lows for the move near $1.1315. The next target is the 61.8% retracement objective of last year’s rally that is found a little below $1.1190. The measuring objective of head and shoulder pattern on the weekly bar charts is near $1.05. It finished yesterday outside its Bollinger Band for the third consecutive session. The lower band is near $1.1345 today. |

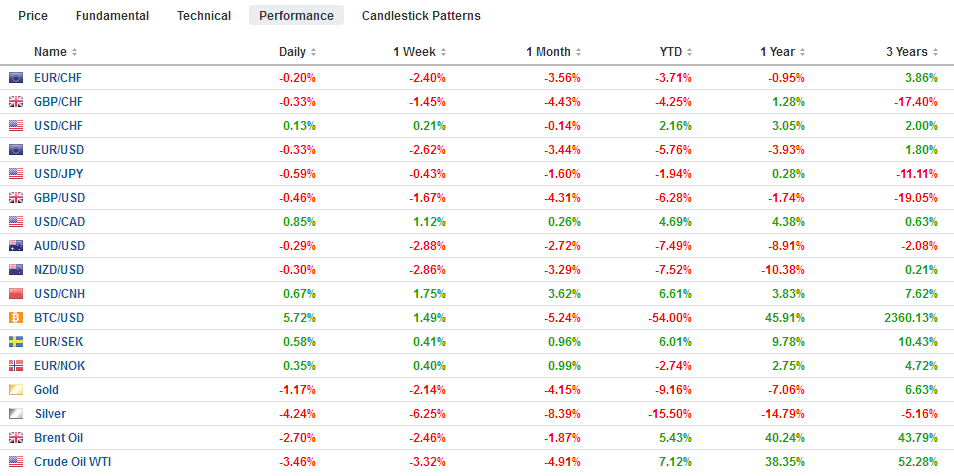

FX Performance, August 15 - Click to enlarge |

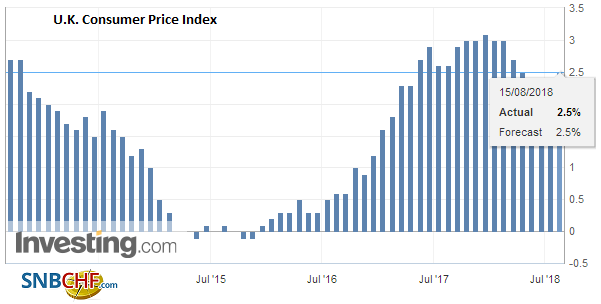

United KingdomThe UK reports an uptick in headline CPI to 2.5% from 2.4%, albeit as expected, and sterling remains heavy. It traded below $1.27 for the first time since June 2017. The core rate was steady at 1.9%, the lowest since March 2017. There is an expiring $1.2750 option (~GBP400 mln) today that could come into play if North America takes some profits on long dollar positions. Note that there is a GBP1.4 bln option at $1.27 that expires tomorrow. |

U.K. Consumer Price Index (CPI) YoY, July 2018(see more posts on U.K. Consumer Price Index, ) Source: Investing.com - Click to enlarge |

The dollar extended its recovery against the yen. At the start of the week, the dollar has tested support near JPY110.00 and today’s gains lifted it to almost JPY111.45. The long-term trendline comes in near JPY111.55. However, we suspect North American operators will be reluctant to push it through the trendline today, preferring perhaps to follow Tokyo’s lead.

Pulled down by a continued sell-off of China shares and weakness in Japan, the MSCI Asia Pacific Index off nearly 1%, for its biggest loss in a couple of weeks. European shares are narrowly mixed, leaving the Dow Jones Stoxx little changed in late morning dealings. Material and telecom are the largest drags, but nearly half the major sectors are lower. Information technology and industrials are firmer. Of the largest bourses, only the DAX is advancing (slightly) today.

Benchmark bond markets remain firm. The 10-year JGB yield eased a little more than a basis point to below 9 bp. Only Italy among the major European bond markets is seeing a higher yield today. Some investors remain concerned that there are voices in the governing coalition, especially in the League, that are not committed to the EU. Still, the deputy who is also a committee chair does not speak for the government, and the market’s reaction says more about the market’s anxiety than the veracity of the claim (EMU would be dismantled unless the ECB defends the spread between Italian and German bonds).

The US 10-year yield has come back softer after testing the 2.90% level late yesterday. In the futures market, the September note tested important resistance near 120-16 at the start of the week and backed off to 120-00 yesterday and is firmer today. A break of this range could signal the direction of the next half point or more.

After a quiet couple of days, the US economic calendar is chock full today. For economists, the non-farm productivity and unit labor costs for Q2 are among the most important. They are both metrics of US competitiveness, and with slow workforce growth, productivity becomes all the more important. However, they are not the stuff that moves the market. For those in the market today, the retail sales report, which covers a little less than half of US personal consumption expenditures, is the most important. Weaker auto sales likely will dampen the headline, but the components used for GDP calculations should recover smartly after being flat in June. As we know, it is not so much a rise in real earning that is driving consumption but the creation of 1.5 mln jobs this year and an increase in consumer credit. US industrial production and manufacturing output are expected to have remained firm, even if off the 0.6% and 0.8% gains were seen respectively in June.

Canada reports July existing home sale following a 4.1% increase in June. Many investors continue to closely track the Canadian housing market. With the June report, the three-month average turned positive for the first time this year. The June rise was also the most since December, which itself (4.5%) was the most since February 2017. The US dollar is trading firmer after bouncing off CAD1.3050 area, where a $740 mln option expires today.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$EUR,$JPY,EUR/CHF,newsletter,U.K. Consumer Price Index,USD/CHF