The recent strength of the US dollar coupled with the rise of the US 10-year Treasury yield has weighed on the price of gold and silver. Since 19 April, gold has lost roughly 2.3%, while silver lost almost 4.5% in USD terms.

At the start of the year, these two drivers were sending conflicting signals: higher US real rates were weighing on non-yielding gold, but the decline in the greenback was acting as a tailwind for gold priced in dollars. Unfortunately for precious metals, the recent broad strength of the US dollar is now also sending a negative signal.

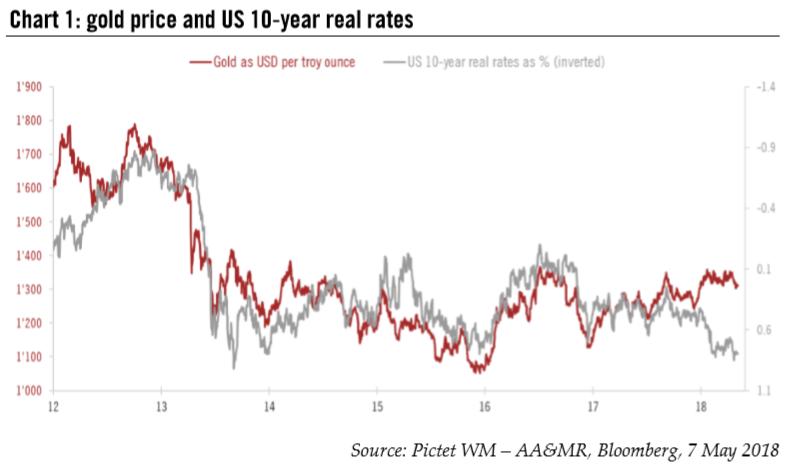

| This could continue in the short term (see “Euro weakness should prove temporary”) .With the risk we see spikes in the US 10-year Treasury yields above 3% (see “US ten-year Treasury update”), gold might trade below the USD1300 per ounce threshold that has held since the start of the year. However, to the extent that any spikes in US rates are linked to inflation fears (hence capping US real rates and potentially weighing on risk appetite) and dollar strength is temporary, we see the downside potential for gold as relatively limited from current levels.

Demand for gold as a hedge against inflation is unlikely to come into play anytime soon as US inflation would have to rise substantially from current levels (possibly above 6%) to trigger a sustained impact on gold prices. The demand for gold as a hedge against tail risks in financial markets has likely been supportive given recent stock market volatility and concerns about a global trade war. However, our baseline scenario remains that such fears should abate in the coming months. We expect further recovery in jewellery demand after a poor 2016, thanks notably to robust growth outlooks in China and India (which together represent more than half of global jewellery demand). However, we do not expect any strong impetuous from this driver. Finally, official demand should remain supportive of gold, as central banks keep buying the yellow metal. However, net purchases by central banks have declined since a peak in 2013, so are unlikely to stimulate gold prices much either. Overall, we think gold price should remain rather trendless over the remainder of this year as the effects of US real rates and the dollar, the main directional drivers, cancel each other out. Our end-of-year projection is for a price of USD1325 per troy ounce. |

Gold Price and US 10-Year Real Rates, 2012 - 2018(see more posts on Gold prices, ) - Click to enlarge |

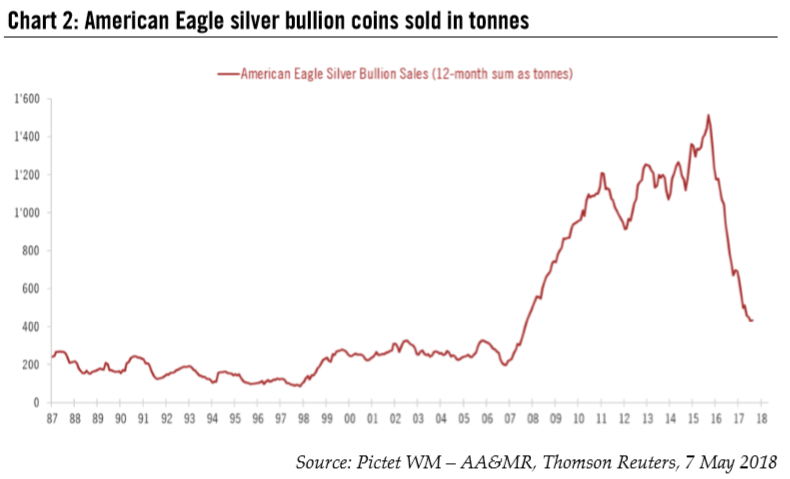

Silver still laggingThe performance of silver since the start of the year has been unimpressive, losing roughly -2.7% (vs. 0.9% for gold). Given the recent moderation in global business activity, the underperformance of this part-precious partindustrial metal makes some sense. However, silver had already been underperforming (in 2017, when global business activity was improving, silver gained only 6.3% in USD vs. 13.5% for gold). This is more puzzling, as silver is deemed cheap compared to gold (the gold/silver price ratio is roughly 28% above its long-term average) and industrial metals are performing well. The major drag on demand for silver seems to be coming from a sharp drop in investment appetite (i.e. for coins and bars, which represents slightly less than 20% of total demand) since last year, in stark contrast with the boom in demand for silver coins and bars from 2007 to 2016. The only comforting news is that we are rapidly approaching the price range seen prior to 2007, so stabilisation seems likely in the not too distant future. |

American Eagle Silver Bullion Coins Sold in Tonnes, 1987 - 2018 - Click to enlarge |

Overall, we continue to prefer silver over gold as the synchronisation in global growth should be supportive of the industrial component of silver demand. Although we acknowledge that investment appetite could remain lacklustre, it seems that the worst is behind us and a re-rating of silver compared to gold remains overdue.

Full story here Are you the author?Tags: Gold prices,Macroview,newslettersent,silver prices