Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

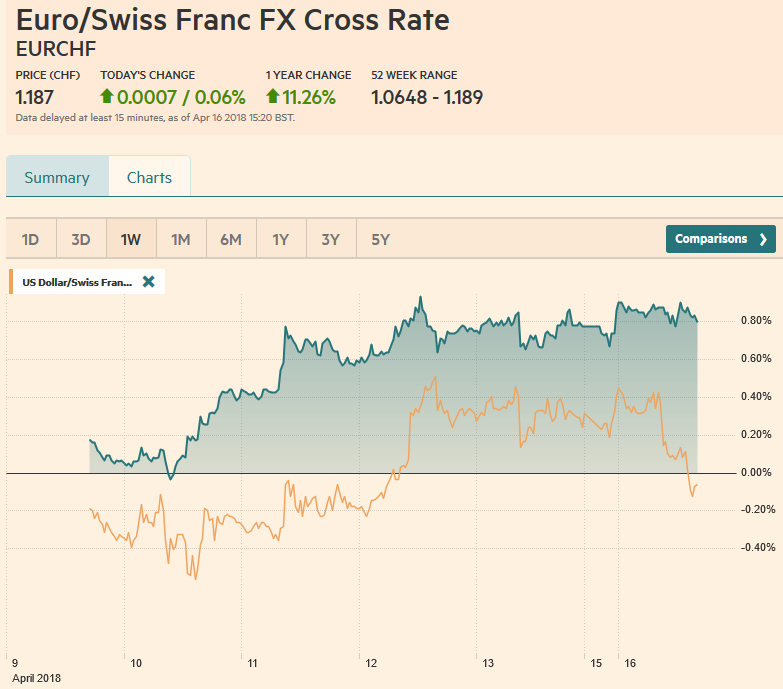

Swiss FrancThe Euro has risen by 0.06% to 1.187 CHF. |

EUR/CHF and USD/CHF, April 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe Syrian strike over the weekend, and the official indication that “mission accomplished” and that was a limited one-off strike has spurred little market reaction. There is one more loose end, as it were, and that is that the US has indicated it will announce additional sanctions on Russia for its involvement in Syria’s chemical weapon use. The ruble is volatile but slightly firmer to start the week, and while dollar-bond yields are firmer, the ruble benchmark is steady. Nor did the US decision to add India to its Treasury’s watchlist for countries meeting one or two of the legislated metrics for currency manipulation. The US dollar rose against 0.3% against the Indian rupee. It is knocking on the upper end of its range from Q4 17. |

FX Daily Rates, April 16 - Click to enlarge |

| The Hong Kong dollar got no reprieve over the weekend. Despite repeated intervention by the HKMA, the currency is pinned, with the greenback at the top of the band. Hong Kong and Chinese shares earlier today, and it was enough to negate gains in most other markets to leave the MSCI Asia Pacific Index little changed (-0.1% after rising in four of five sessions last week).

The Hang Seng fell 1.6%. It was the third consecutive decline and all the major industry groups fell. Mainland shares that trade in Hong Kong Hong Kong Enterprise Index) was off a little more than 2%. The Shanghai Composite fell 1.6% and is now nursing a three-day slump. Japan’s Nikkei rose 0.25%. It is within striking distance of 22000, which has capped it since the end of February. |

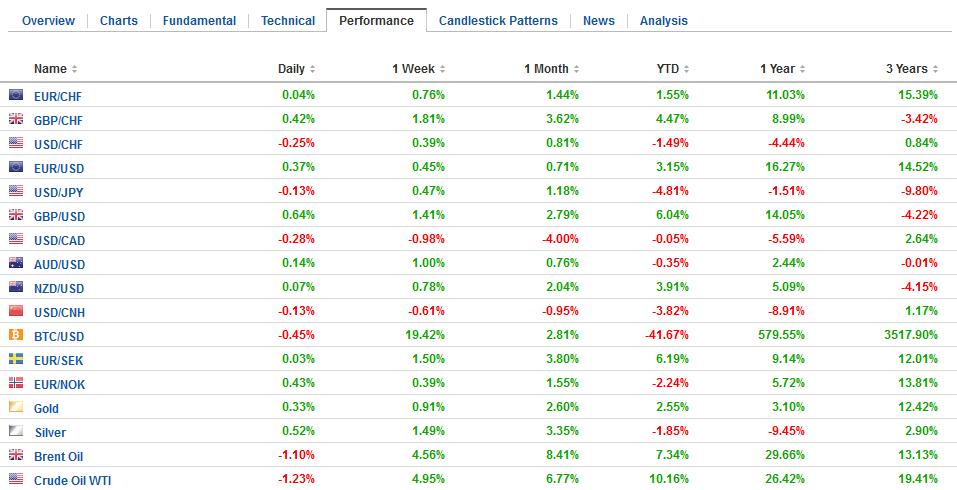

FX Performance, April 16 - Click to enlarge |

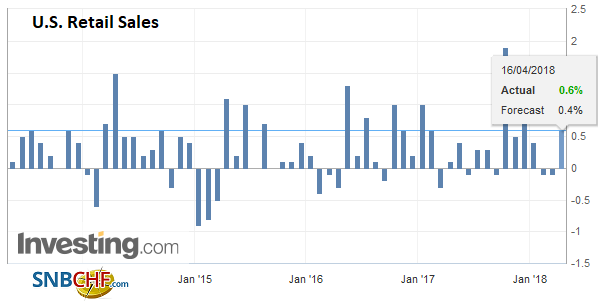

United StatesThe US reports the Empire manufacturing survey for April, but will likely be overshadowed by March retail sales. |

U.S. NY Empire State Manufacturing Index, May 2013 - Apr 2018(see more posts on U.S. NY Empire State Manufacturing Index, ) Source: Investing.com - Click to enlarge |

| Retail sales are expected to snap a three-month decline with a 0.4% advance, helped by stronger auto sales. The components used for GDP calculations are expected to rise by 0.3%. It averaged a monthly gain of 0.4% in 2017 and 0.5% in Q4 17. It has been down two of the past three months, but this seems to overstate the pullback in US consumption. |

U.S. Retail Sales, May 2013 - Apr 2018(see more posts on U.S. Retail Sales, ) Source: Investing.com - Click to enlarge |

The Dow Jones Stoxx 600 is struggling to hold on to early upticks and is putting at risk the two-day advance seen at the end of last week. Energy and consumer staples are leading the losses. Healthcare and information technology are holding on to small gains near midday in Europe. Oil is giving back some of last week’s gains. Brent and WTI are off nearly 1.5% after gaining more than 8% last week.

Bond yields are mostly higher with the US, and core European 10-year rates are three basis points higher, while peripheral European yields are up a bit less. After a deluge of supply, the US flood slows this week, with only the usual bill offerings and a five-year floating rate note on tap.

The US dollar is under some modest pressure. It is only firmer against the Canadian and New Zealand dollars. The Swedish krona, which was the weakest of the major last week, after inflation missed expectations, is the strongest, gaining 0.5% against the greenback.

The euro is just above the middle of the $1.23-$1.24 range seen last week. There is a large 1.3 bln euro option struck at $1.23 that expires today. The dollar rose to JPY107.75 before the weekend but has lost any upside momentum today. It pulled back to nearly JPY107. The $550 mln option that struck at JPY107.40 that expires today may cap upticks.

Prime Minister Abe remains mired in several scandals, and his support has fallen. Sunday’s much-watched Nippon TV survey showed support for the prime minister had eased to 26.7%, the lowest since he was elected in late 2012. Abe trip to the US may brandish his international credentials and stabilize his support. Some press reports quote from former Prime Minister Koizumi suggesting that Abe may step down at the end of the Diet session in June. Since Abe has been a vocal advocate of weaker yen in word and deed, the decline of his fortunes is seen as supportive, at least on the margins, for the currency.

Sterling remains firm and is within striking distance of the best level since the 2016 referendum against the dollar that was seen in January near $1.4345. Prime Minister May is expected to be criticized by the opposition for not seeking parliamentary approval before the weekend strike, but as a whole, it will support her actions. It seems more like political theater than a substantive attack. The euro staged a reversal against sterling before the weekend, and there was initial follow-through euro buying, but it fizzled near GBP0.8670. A move below GBP0.8640 suggests more work is needed to build a base.

The Canadian dollar has had a strong recovery beginning around the middle of last month. It entered into a consolidative phase in recent days. The US dollar can edge higher in this corrective period. The CAD1.2650 offers the initial corrective target. After being rebuffed by $0.7800 at the end of last week, the Australian dollar is flattish today, consolidating in a 15 tick range on either side of $0.7765.

After the markets close today, the US Treasury will release its TIC data, which is among the most comprehensive reports of US portfolio flows. Foreign investors bought a $36.675 bln a month of US paper assets in 2017 and were sellers of $11.22 bln a month in 2016. The increase in dollar LIBOR has boosted the cost of hedging US fixed income investment, ostensibly deterring foreign purchases. Note the January purchases of nearly $120 bln of US financial assets was more than in all but two months since August 2015.

At least ten Fed officials (of 15 Presidents and Governors) speak this week. Kaplan, Kashkari, and Bostic get the ball rolling today. The market remains convinced that there will be at least two more rate hike this year, with the next move coming in June.

A busy week for Canada begins slowly. This week, central bank meets. It is expected to be on hold, but a rate hike in Q3 is still is the favored scenario. Later this week, Canada reports retail sales and CPI.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,newslettersent,SEK,U.S. NY Empire State Manufacturing Index,U.S. Retail Sales,USD/CHF