Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

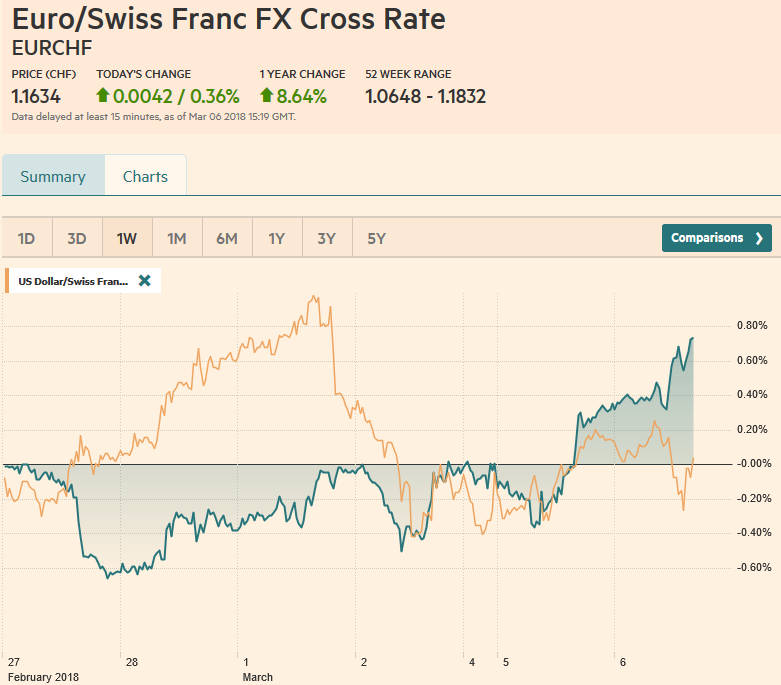

Swiss FrancThe Euro has risen by 0.36% to 1.1634 CHF. |

EUR/CHF and USD/CHF, March 06(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe resiliency of the status quo is again on display. After much chin wagging and finger pointing after the Italian elections and the modest decline in Italian assets, they have bounced back today. Italian bonds and stocks are participating in today’s advance. Italian equities were off 0.5% yesterday and are up a 1.1% near midday in Milan. Italy’s 10-year yield rose three basis points yesterday is off five today. It is true that in these early hours after the election, in which the center parties lost handily, the new government is hard to envision. There does seem to be a lot of posturing. However, recall that in September German SPD leader Schulz ruled out another grand coalition, but this past weekend, the SPD approved it, though with Schulz. Renzi offers to resign as leader of the PD, but only apparently after a new government is formed and the PD is not part of it. |

FX Daily Rates, March 06 - Click to enlarge |

| Last week’s indication that the US Administration was preparing to put a 25% tariff on steel imports and a 10% tariff on aluminum sent ripples through the capital markets. It is the beginning of a tit-for-tat trade war were told. Shades of Smoot-Hawley. The system of checks and balances continues to unfold.

Republican leaders have pressed the President to reconsider, as they successful did on his stance on guns and immigrants. Gary Cohn, head of the National Economic Council has reported pulled together an industry summit explain to the President why the tariffs will end up undermining the US economy and offset the beneficial impact of the tax cuts. |

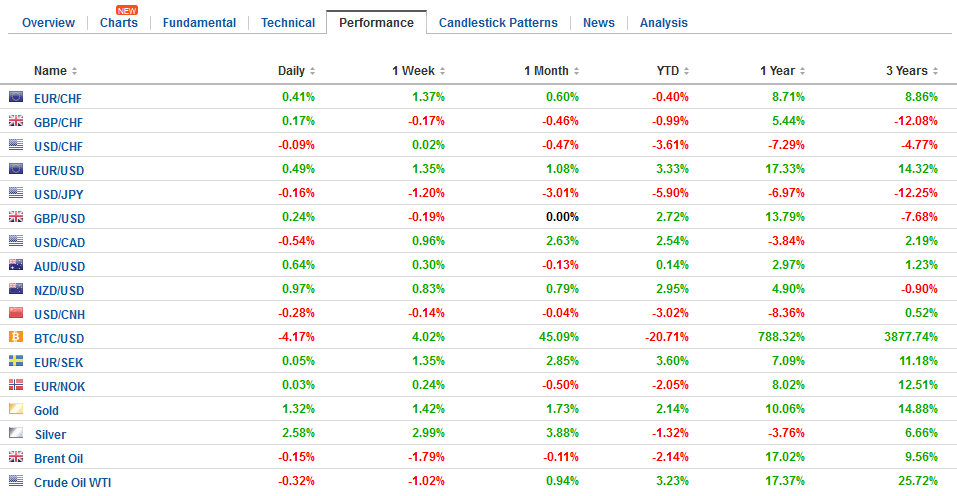

FX Performance, March 06 - Click to enlarge |

Eurozone |

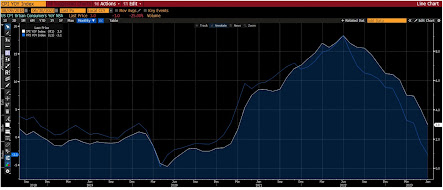

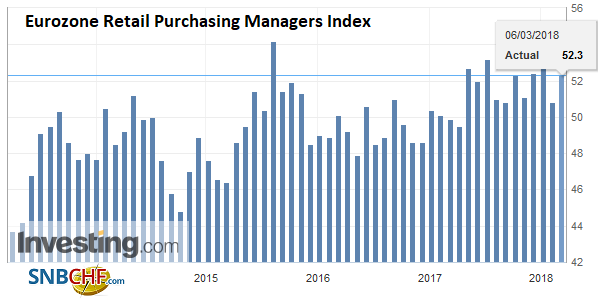

Eurozone Retail Purchasing Managers Index (PMI), Mar 2013 - 2018 Source: Investing.com - Click to enlarge |

If persuasion is not sufficient, there is more Congress can do. Republican Senator Lee has proposed a bill, Global Trade Accountability Act, which would claw back some of the power the legislative branch has surrendered to the executive branch. It subjects all trade action to Congressional approval. There is scope for additional legislative action. The President may want to extend Trade Promotion Authority, but Congress can block this in the coming weeks. Also, there is talk of attaching an amendment to a bill that needs to be passed, such as the spending bill, that would block the tariffs.

One of the challenges of finding a veto-proof way to combat the tariffs is that there are many Democrats that are sympathetic to them. However, this is not really new news. Typically, trade legislation is backed by most Republicans and a free-trade wing of the Democrat Party.

Another element of resilience is the global equity market. The threat of a trade war seemed end the recovery after the swoon early last month. Yet, the S&P 500 reversed higher before the weekend and extended those gains yesterday. A move above 2734 would re-target last week’s high near 2790. In the wake of Wall Street’s strong gains yesterday, the MSCI Asia Pacific Index rose 1.3% today, snapping the five-day slide. European shares are also advancing. The Dow Jones Stoxx 600 is up 0.7% today, led by materials, financials and telecom.

There are two economic developments to note. First, after reporting softer than expected retail sales and a larger than expected current account deficit, the Australian central bank left rate on hold and made only small changes to the accompanying statement. While it expects exports to improve, it is watching household consumption closely. There is little indication that the RBA will change policy any time soon. Meanwhile, the decline in net exports and capex in Q4 warns of downside risks to the Q4 17 GDP report that is due tomorrow.

The second development was the comments by BOJ Governor Kuroda before the Diet. Kuroda reiterated his comments from last week. Essentially, he is saying that in the fiscal year starting in April 2019, when the BOJ currently projects that inflation will reach its target, the BOJ may begin thinking about exiting its extraordinary policies. The exit is conditioned on reaching the inflation target, and the BOJ has frequently pushed further out it time when this condition will be met. The takeaway is that the BOJ is not on the verge of removing its support.

The US dollar is sporting a slightly heavier profile today. The Swiss franc and the beleaguered Canadian dollar are the exceptions. Year-to-date, the Canadian dollar is the worst performing major currency, having lost 3.1% against the US dollar. The Swedish krona is the second worst, losing 0.8%. Comments earlier today by the Riksbank Governor Ingves, explaining to Parliament, his cautiousness, even though the refi rate is at -0.50% and growth is robust (~3.3% in Q417). The euro did record new multiyear highs against the krona earlier today before profit-taking was seen. Most of the major currencies are little changed as the market awaits this week’s key development, including the ECB and BOJ meetings and US jobs data.

The US economic calendar features factory orders and the final durable goods orders report. The tax cuts, depreciation allowance, and the repatriation are projected by economists to boost investment in the US. The preliminary January durable goods orders did not show this. In fact, excluding defense and aircraft, durable goods orders fell. Revisions are possible today with the factory goods orders, but they are not likely to be substantial. New York Fed’s Dudley speaks early, while Brainard speaks late in the day (after the markets close) and Kaplan will speak early in the Asian session on Wednesday. Both Brainard and Kaplan (Governor and Dallas Fed President, respectively) are likely candidates to not favor committing to four hikes this year.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: $AUD,$EUR,$TLT,EUR/CHF,Eurozone Retail PMI,Italy,newslettersent,SEK,SPY,USD/CHF