Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

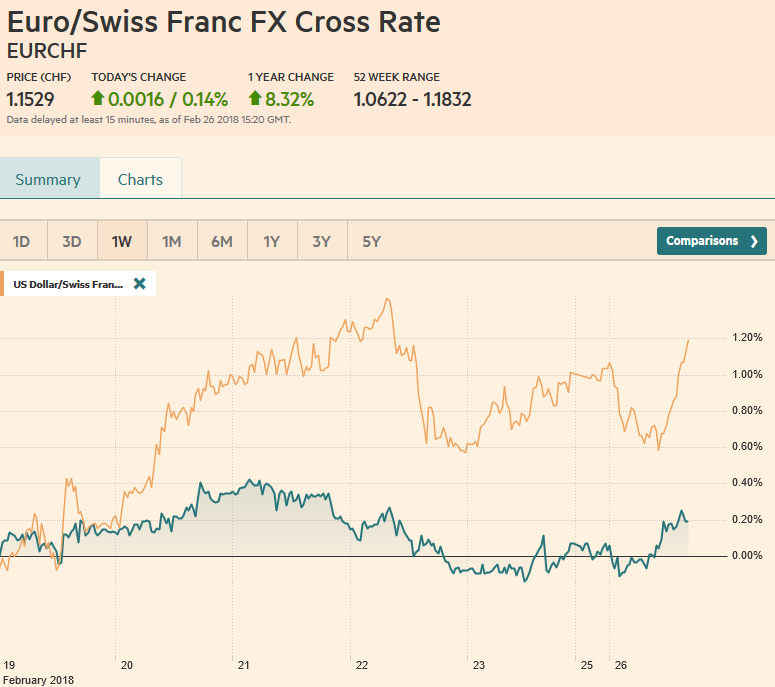

Swiss FrancThe Euro has risen by 0.14% to 1.1529 CHF. |

EUR/CHF and USD/CHF, February 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

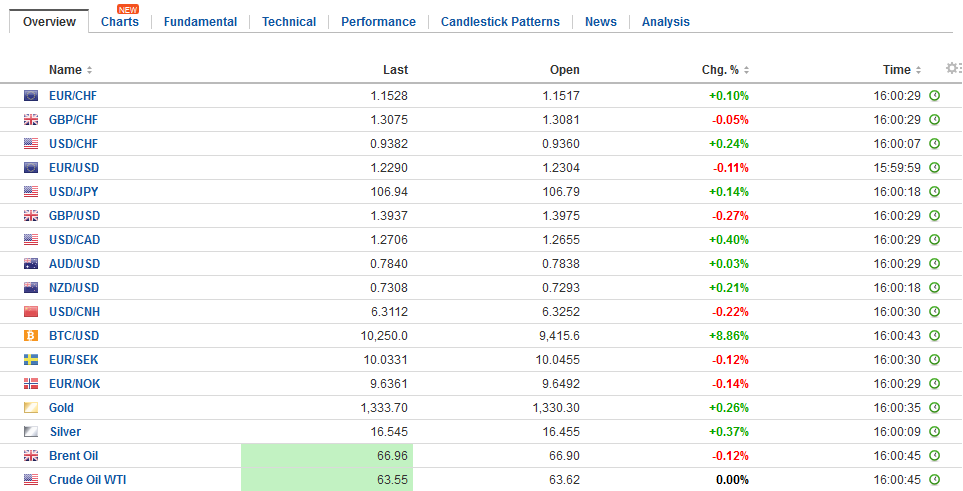

FX RatesThe US dollar has begun the new week on heavy footing. It is being sold against virtually all the currencies, major and emerging market currencies. There is one exception, and although the local market is not open, the Mexican peso is under some pressure that could be linked to a dispute between the President of Mexico and the US that prompted the former to cancel a visit to the latter. It makes for a poor backdrop for the resumption of NAFTA negotiations, and the other NATFA member, Canada as the weakest of the major currencies today (practically flat at CAD1.2625). Sterling is the strongest of the majors, gaining 0.6% today. It reached a six-day high near $1.4070, which tests a downtrend line drawn off the January high of $1.4245. Note that there is a large GBP2.3 bln option struck at $1.40 that expires today. |

FX Daily Rates, February 26 - Click to enlarge |

| The main consideration appears to by the turn toward the hawks by BOE Deputy Governor Ramsden. Ramsden was one of the dissents from the decision to hike rates last November. In an interview with the Sunday Times, Ramsden acknowledged coming around and seeing a case for faster hikes. He appeared to pin his views on the prospects of wage growth. UK interest rates are a bit firmer (one-two basis points), but the odds of a May hike have changed little just below 50%, interpolating from the OIS.

Separately, and apparently shrugged off was news that January business lending fell 1.4% year-over-year. It is the first drop since 2015 and follows softer PMI readings. Investors are also able to compartmentalize Brexit angst. Although not in his prepared remarks, Corbyn is expected to support some effort to maintain a customs union with the EU, which is the essence of an amendment attached to a trade bill. This will challenge government’s position. May’s approach, expected to be spelled out in a speech at the end of the week, has already been rejected by EU negotiators. |

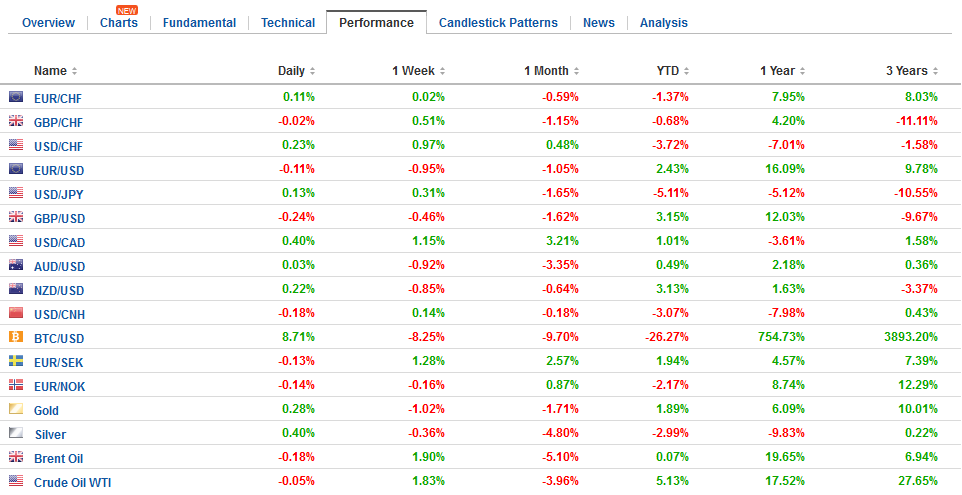

FX Performance, February 26 - Click to enlarge |

United States |

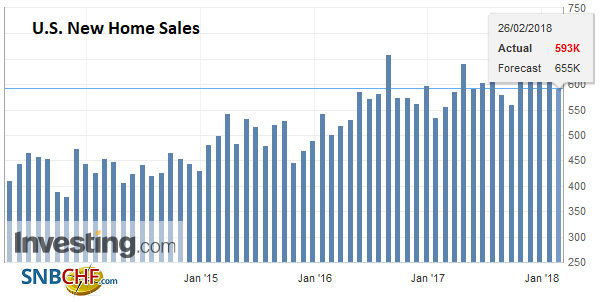

U.S. New Home Sales, Jan 2014 - Jan 2018(see more posts on U.S. New Home Sales, ) Source: Investing.com - Click to enlarge |

While it is not unusual for a softer dollar to lift commodity prices other forces are at work. Iron ore and steel prices have rallied despite signs that the US is considering 24% tariffs (on national security grounds). Iron ore futures rose 1.5% in Singapore to reach 10-month highs before closing 0.1% higher. Steel rebar prices in Shanghai jumped nearly 4%, though closed up 2%. Before the weekend, officials in Tangshan, a key steel center, extended its pollution-inspired production cuts that were to end in the middle of March. The new end date is mid-November. This idles an estimated 9.9 mln tons of capacity.

Investors did not seem disturbed by reports that China is considering lifting term limits for the President and Premier. This seems to be largely expected consequence of the concentration of power by President Xi. Xi has three official roles, head of party, head of military and head of state. It is only the last that has a term limit. Longer-term, there contradiction between a modernizing economy and an archaic political structure is a concern.

Chinese investors have returned from the Lunar New Year celebration in a bullish mood. The Shanghai Composite rose 1.25% today. In the three sessions since re-opening, the Composite has risen a little more than 4%. It is partly fortunate that global equities were also in recovery mode. The MSCI Asia Pacific Index rose 0.8%. It is at its best level since February 5. It has nearly retraced 61.8% of its earlier drop. The Nikkei, by contracts, is testing the 38.2% retracement of its decline.

European equities are following suit. The Dow Jones Stoxx 600 is up 0.5%. It too had stalled last week near the 38.2% retracement of its recent swoon, but it gapped above it today (~381.4). The 50% retracement is near 385.6. As the Italian election draws near, the equities may struggle to maintain the previous strength. It is the best performing G7 equity market this year, though over the past several sessions it is in the middle of the pack.

The bond market is different story. Peripheral bonds yields are lower in Europe, with the four-basis point decline in Italy’s 10-year benchmark bond leading the way. Italy’s two-year yield is a single basis point lower, but this is more than Spain. Core yields through the coupon curve are slightly firmer.

Powell’s testimony tomorrow may overshadow the economic data in the coming days. Today’s reports include the Chicago Fed’s National Activity Index for January and the Dallas Fed manufacturing index for February, which are not typically market-movers in the first place. January new home sales may attract some interest, but after a 9.3% slide in December, some bounce is widely expected. Form the Fed, Bullard and Quarles speak but their views are known.

The euro is at the upper end of a narrow four-day range. There are some chunky options that expire today. The $1.2350 is the most pressing (1 bln euros), but there are 656 mln euros struck at $1.23 and 825 mln euros struck at $1.24 that will also be cut. There is a JPY106 strike for $965 mln and JPY107.00-JPY107.05 for $2.38 bln). There is a A$510 mln option struck at $0.7900 that expires today.

The Dollar Index is testing the 89.50 area, which corresponds to a 38.2% retracement of its gains off the February 16 low, and the 20-day moving average. The low does not seem to be in place for the day. The next target is 89.00-89.25.

Graphs and additional information on Swiss Franc by the snbchf team.

Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,newslettersent,SPY,U.S. New Home Sales,USD/CHF