Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

There are three distinct classes of drivers in the week ahead. The first is high frequency data. The most important of the economic reports include the preliminary estimate of the February inflation in the euro area, the US January income, and consumption data alongside the Fed’s preferred inflation measure, the core PCE deflator, and Japanese retail sales and industrial production figures.

The second group of drivers is the key speeches by the UK’s Corbyn and May, Powell’s testimony before Congress, and Draghi appears before the European Parliament. The third group consists of two key political events in Europe–namely the Italian national election and the outcome of the vote by the SPD whether to join a new Grand Coalition.

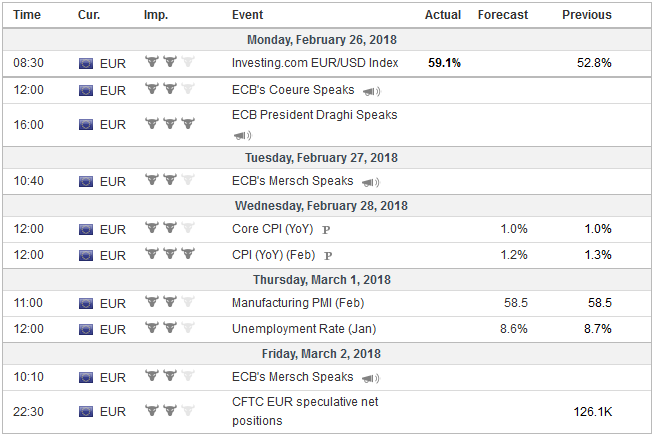

EurozoneLet’s turn to the economic data first. The preliminary February CPI for the eurozone is the most contemporaneous data. The headline rate may slow to 1.2% from 1.3%, partly reflecting the softer oil prices this month. The core rate, which while not targeted has assumed greater significance under Draghi than his predecessor Trichet, may have held steady at 1.0%. The market will be sensitive to any surprise, thinking that it will impact the debate between the doves and hawks as the last CPI report before the early March ECB meeting. On a trade-weighted basis, the euro edged fractionally higher, while service prices look firm. Money supply (M3) growth slowed every month in Q4 17 but may have stabilized in January. Separately, and consistent with the recent PMI readings, German IFO and ZEW and French business surveys, eurozone confidence surveys for February likely soften. |

Economic Events: Eurozone, Week February 26 - Click to enlarge |

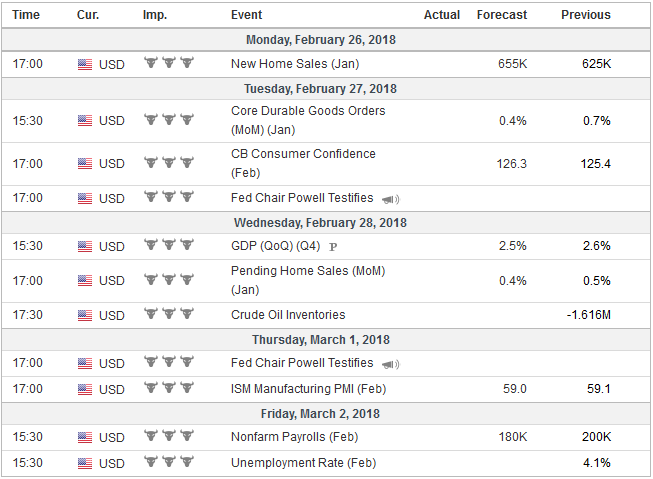

United StatesThe US provides a second look at Q4 GDP, and slightly softer consumption warns of downside risk to the initial 2.6% estimate. Two-thirds of the way through Q1 18, the report is too historical to matter much. Both the Atlanta Fed’s and NY Fed’s GDP trackers have converged to 3.1%-3.2% for the current quarter’s growth. The faster growth that is anticipated seems bumps up against changing composition. January retail sales were weaker than expected and the December series was revised lower. Retail sales account for a little less than half of the personal consumption expenditures. The January PCE is expected to slow to 0.2% from 0.5% average monthly gain H2 17 and would be the smallest increase since last August. Industrial output also slowed in January after a strong (perhaps spurred by rebuilding from storms) Q4. The trade balance deteriorated sharply in Q4, and the advance report for January merchandise trade is expected to show little improvement. In addition to January 2017, there was only one other month last year that the core deflator rose by 0.2%. This has two implications. First, even a 0.3% increase in the core deflator in January 2018 will leave the year-over-year rate steady at 1.5%. Second, an acceleration of price pressures, which so much seems to ride, is subtle at best, and slow in any event. The monthly increase average 0.13% in 2017 and 0.15% in 2016. It averaged 0.11% in H1 17 and 0.14% in H2 17. |

Economic Events: United States, Week February 26 - Click to enlarge |

JapanThere are several Japanese economic reports in the week ahead. Growth edged up a mere 0.1% in Q4 17 and seems stuck in a low gear at the start of this year. Consumption that rose 05% in Q4 appears to have slowed. Retail sales and overall household spending likely fell in January. Industrial output is expected to have fallen, as well. Nevertheless, the employment report is likely to show the labor market remains tight, and it has been augmented by women (who have a higher participation rate than in the US), immigrants (more than one million), and elderly people. |

Economic Events: Japan, Week February 26 - Click to enlarge |

United KingdomTurning to speeches, many see UK Prime Minister May’s speech at the end of the week as key. We are skeptical. The government’s position has crystallized: leaving the single market and customs union but strike a close trade deal with aligned regulations. But it is DOA as in dead-on-arrival. Brussels has already rejected this approach, which strikes many of its officials as a cherry-picking exercise. Perhaps more important for the evolution of Brexit is Labour leader Corbyn’s speech at the start of the week. Corbyn is likely to confirm a subtle shift in Labour’s position to remaining in the customs union. It may not sound like a significant move, but it sets the stage for parliament to possibly reject the Brexit deal the government negotiates. Meanwhile, Remainers from both main parties is supporting an amendment to a trade bill along these lines. The employer’s association, CBI, also backs remaining in the customs union. It also would solve the problem of the Irish border. However, May’s position is not untenable. She could make the vote on the trade bill a vote of confidence. In any event, a defeat for the Tories in local elections this spring could see a leadership challenge. |

Economic Events: United Kingdom, Week February 26 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week February 26 - Click to enlarge |

The new Federal Reserve Chairman appears before both houses of Congress in the coming days. Many are hoping to glean more insight into Powell’s leanings, but little new is likely to be garnered. Powell’s confirmation hearings and the report issued at the end of last week underscores investors’ belief that although President Trump chose to change chairs, he ultimately achieved as much stability and continuity as can be reasonably imagined.

At the risk of over-simplifying the Fed’s economic assessment can be summarized in five observations:

- The labor market remains solid, and wage growth is likely to increase.

- Household wealth is rising.

- Confidence measures are robust.

- The global backdrop is strong.

- Financial conditions are accommodative.

Is it true, as one journalist put it for many, that the Fed is under pressure to act more quickly to guard against the possibility that economy overheats? That assessment seems wide of the mark. The Federal Reserve indicated in December, and more recent comments have not contradicted it, that three hikes this year are likely to be appropriate. The market is the one behind the curve. It does not have three hikes discounted.

Some investment houses forecast four hikes this year, but that is not what is discounted in the OIS or futures market. Perhaps owing to the slow start of the rate hikes (one in 2015 and one in 2016), some criticized the Yellen Fed for over-promising and under-delivering. Tactically, a case can be made for Powell under-promise and over-deliver by not formally calling for a fourth hike.

Powell will be able to raise rates at his first meeting, which helps create this persona as Chair. It would be a knock again him if at the meeting he facilitated an increase to four hikes, but then due to changing circumstances could only hike three times. The equity market swoon that marked his first days as Chair we suggest is purely coincidental.

Powell may be pushed on his views of that drop in the stock market, and investors will be interested in knowing if there is a Powell Put. We think it has gotten a bad name, but central banks ought to take into account major disruptions in the capital markets when setting policy because of the risks to the underlying economy. That said, the context matters, and we suspect that Powell will not strike a different chord than several other Fed officials who played down the significance of the recent decline.

ECB President Draghi will speak to the EU Parliament, and he will be joined by Spain’s De Guindos, who is tipped to be the next Vice President of the central bank. Draghi is unlikely to break new ground, but the market will be looking for clues into the March 8 meeting. New staff forecasts will be available, and many are looking for modest tweaks in the statement that show the ECB’s commitment to winding down its asset purchases.

However, it is important the arguments of those opposed to the ECB that Draghi’s will address. Inflation is not yet on a durable, self-sustaining path toward the target. This is a time for patience and perseverance. The extraordinary measures are showing results. Some in the media suggest that an early exit to the asset purchases is a genuine possibility. We think otherwise, and indeed, judging from comments from several ECB officials, including some thought to be hawks, suggest a consensus has formed to taper further after September.

Lastly, the two big political events on March 4 may also influence investors in the days ahead. The Italian election will be held and the results of Germany’s SPD decision on forming another grand coalition with Merkel’s CDU/CSU. Merkel’s center-right coalition is expected to endorse the grand coalition early next week.

Polls suggest the SPD will, in fact, endorse the coalition. The failure to do so could spur a sharp decline in the euro. It would force either a minority government or new elections. New elections are risky. Polls show that popular support for the SPD has continued to fall since last September’s election and that it is now in third place behind not only the CDU/CSU but the populist AfD as well. If new elections are needed, it is less clear that Merkel will survive as Chancellor, and it raises questions about new initiatives in Europe this year.

The Italian elections were seen as the major European political risk this year. The polls before the blackout period had the center-right getting the most votes, but not a majority. Polls showed a battle for second between the center-left and the Five-Star Movement. A splinter group that broke away from the center-left PD over a disagreement with Renzi could account for the difference.

Like others, we had thought that in the run-up to the election, Italian asset would underperform, but they have not. Italy’s 10-year yield has risen six basis points this year. Germany’s 10-year yield is up nearly 23 bp. Spain is a more comparative asset to Italy than Germany. Its yield is up three basis points. Portugal’s 10-year yield is up 13 bp.

The short-end of the coupon curve tells a similar story. Italy’s two-year yield has risen 10 bp this year; so has Germany’s. Spain’s two-year yield has risen 21 bp and Portugal 17 bp.

Italy’s stock market (FTSE-Milan) is the best performing in the G7 this year. It is up 3.75%. Germany’s DAX is off 3.4%, Spain’s IBEX is off 2.2%, and the Dow Jones Stoxx 600 is off 2.1%.

We suspect the most likely result is that the center of the center-right bloc and the center of the center-left bloc form a government after some false starts. The odds seem to favor EU Parliament President and a member of Berlusconi’s Forza Italia as the next Prime Minister.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,newslettersent