Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

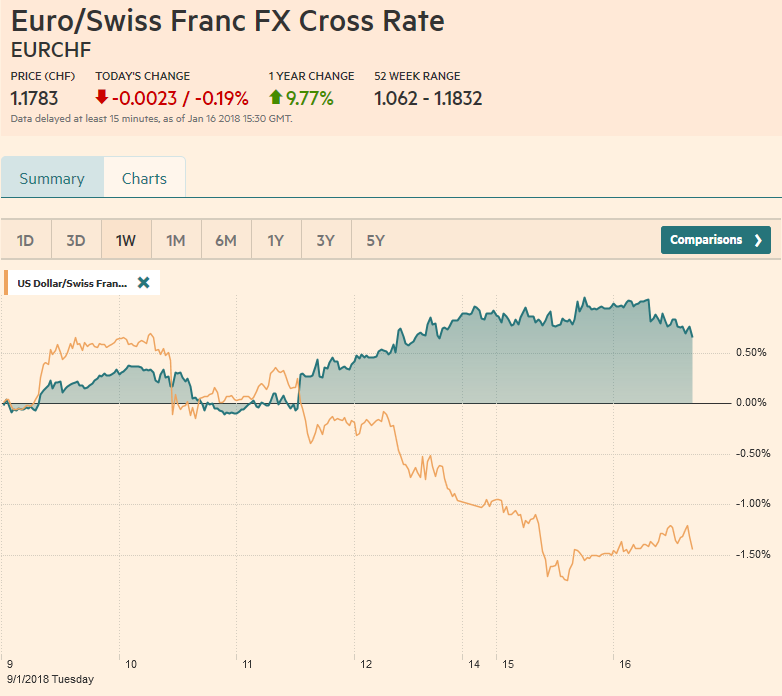

Swiss FrancThe Euro has risen by 0.19% to 1.1783 CHF. |

EUR/CHF and USD/CHF, January 16(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesAfter extending its recent slide yesterday, which the US markets were on holiday, the dollar is firmer against all the major currencies and most of the emerging market currencies. There does not seem to be macroeconomic developments behind the dollar’s stabilization, and the gains are quite minor, suggesting a pause in the downtrend rather than a reversal at this juncture. That said the extent and duration of what appears to be little more than a technical adjustment is the key to the near-term outlook. The euro rose for the fourth session yesterday and approached $1.23. Today, the pullback took place mostly in the European morning. Initial support is seen in the $1.2180 area. News from the eurozone is light. Germany and Italy confirmed their December inflation readings ahead of the aggregate report tomorrow. Much of the discussion of the ECB stance, including the record from the December meeting that the market read so hawkishly, was before the preliminary release of the December CPI. Recall that it was softer than expected. The headline eased to 1.4% from 1.5%, but it was the flat core at 0.9% that was most disappointing. Recall that the core measure bottomed at 0.6%. The core rate jumped to 1.2% in early Q2 17 and returned to it in early Q3, but has returned to the middle of its four-year range. |

FX Daily Rates, January 16 - Click to enlarge |

| China’s rating agency Dagong cuts its rating assigned to the US to BBB+ from A- (stable outlook) citing that tax cuts reducing revenue. Investors do not typically take the agency rating seriously. As Bloomberg note, Dagong puts the US credit rating on the same level as Colombia. Although the rating agency is not an official (state-owned), the downgrade looks political and perhaps retaliation for S&P’s downgrade of China’s sovereign rating last September and protested a downgrade by Moody’s earlier last year.

While corrective forces apparently on this Turn Around Tuesday in the foreign exchange market, equities continue to motor higher. The MSCI Asia Pacific Index advanced 0.4% after a 0.6% advance yesterday. It is driving the MSCI Emerging Markets Index to record highs. European share is also extending the year’s strong start. The Dow Jones Stoxx 600 is up 0.4%, led by the beaten-up utilities. Materials and energy are drags, as base metals and oil are softer. Bond markets are moving higher today alongside the equity markets in Europe. Yields on Japan and Australia edged higher today, but benchmark 10 -year yields are two to five basis points lower in Europe and the 10-year Treasury yield is off 2.5 bp to 2.52%, a four-day low. |

FX Performance, January 16 - Click to enlarge |

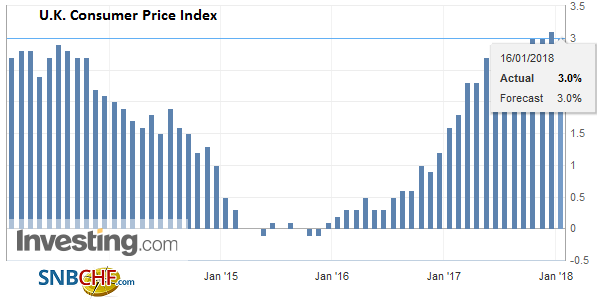

United KingdomThe UK reported December prices today. Headline CPI was in line with expectations, rising 0.4% on the month, which saw the first decline in the headline rate (3.0% from 3.1%) in six months. The core rate eased a little more than expected. The 2.5% year-over-year rate is the lowest in five months. Service inflation also fell to 2.5%, which is a nine-month low. Given the re-weighting of airfare, it may be premature to read too much into today’s report, but many, including ourselves, continue to look for the past decline of sterling to drop out of the comparisons, which would point to a general easing of price pressures. Also, a favorable dynamic was apparent in producer prices, where input prices slipped more than expected while output prices were firmer than expected, which speaks to margins. Separately, news reports suggest that the EU has toughened its demands for a transition deal. The negotiators were given more specific terms that will complicate the talks. The UK is being asked to adhere to EU rules on immigration and rights of EU citizens to live in the UK during the transition, as well as agree to no new trade agreements and no renegotiating fishing rights during the transition. In essence, these latest conditions appear to make more concrete what a “standstill” transition means. Four sessions ago, sterling was fraying support seen near $1.35. Yesterday, it saw $1.3820. Recall that $1.3805 is the 61.8% retracement of sterling’s drop following the 2016 referendum, and $1.3885 is the 38.2% retracement of the decline since the 2014 peak a little shy of $1.72. Sterling has slipped to nearly $1.3740 in the European morning. Support is seen in the $1.3680-$1.3700. |

U.K. Consumer Price Index (CPI) YoY, December 2017(see more posts on U.K. Consumer Price Index, ) Source: Investing.com - Click to enlarge |

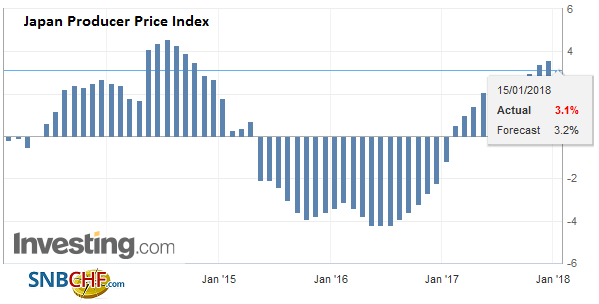

JapanThe BOJ’s Kuroda reiterated his commitment to continue to pursue policies that will push inflation toward the 2% target, while recognizing improvement that has been secured. Finance Minister Aso was careful not to say much about current yen levels, but did speak against excess moves in exchange rates. The dollar is stabilizing against the yen after approaching JPY110.30 yesterday. The dollar began last week above JPY113.00. |

Japan Producer Price Index (PPI) YoY, December 2017(see more posts on Japan Producer Price Index, ) Source: Investing.com - Click to enlarge |

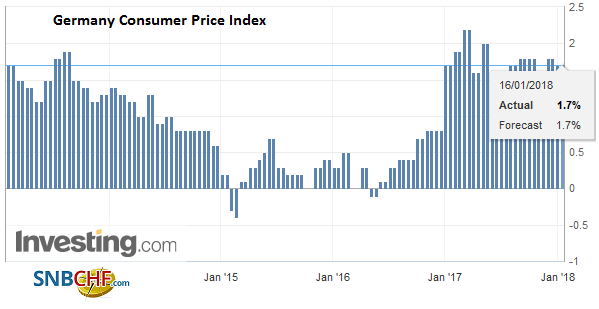

GermanyNews yesterday that both the German and French central banks have purchased Chinese yuan for reserve purposes is notable but not surprising. The ECB indicated was adding yuan to its reserves around the middle of last year and it makes sense that it is partly duplicated within the Eurosystem. Still, it should not be exaggerated. The yuan has the smallest of shares of a reserve currency of a little more than 1%. It is also not surprising that some central banks have added yuan given that since the end of 2016 it is part of the SDR. More striking, we thought were the comments from the BBK official recognizing that China’s effort to boost the internationalization of the yuan has stalled lately. |

Germany Consumer Price Index (CPI) YoY, December 2017(see more posts on Germany Consumer Price Index, ) Source: Investing.com - Click to enlarge |

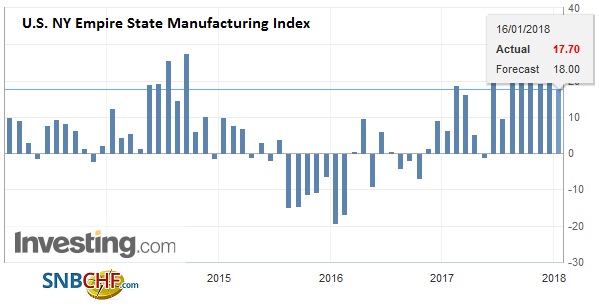

United StatesThe light North American calendar features the Empire State Manufacturing Survey (an early look at January). Tomorrow the Bank of Canada meets and is widely expected to lift rates. There is scope for “buy the rumor, sell the fact” or other disappointment given market positioning. Tomorrow the Fed’s Beige Book, industrial production, and the TIC report are on tap. Fourth quarter corporate earnings will also be reported throughout the week. US earnings are expected to have risen by around 12% last year.

|

U.S. NY Empire State Manufacturing Index, Janaury 2018(see more posts on U.S. NY Empire State Manufacturing Index, ) Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CNY,$EUR,$JPY,$TLT,EUR/CHF,Germany Consumer Price Index,Japan Producer Price Index,newslettersent,U.K. Consumer Price Index,U.S. NY Empire State Manufacturing Index,USD/CHF