Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

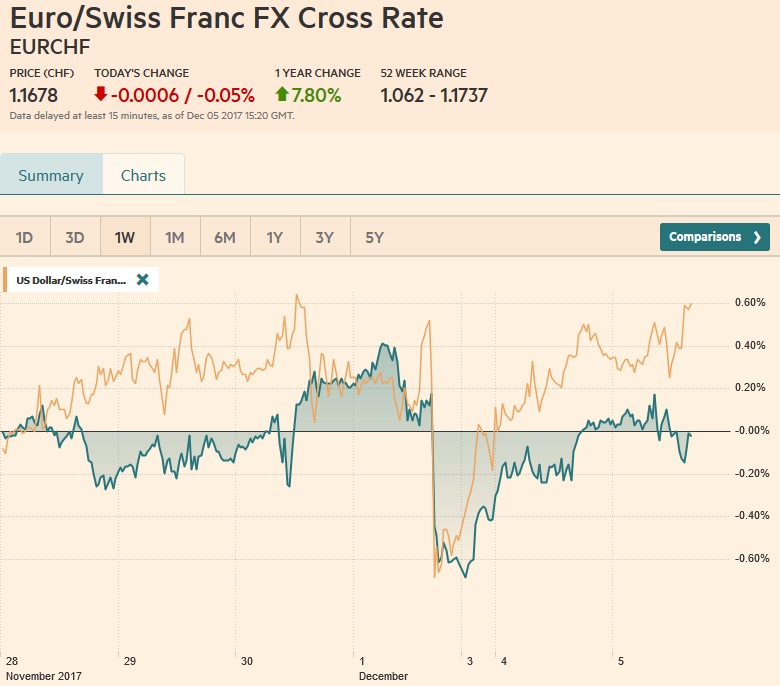

Swiss FrancThe Euro has fallen by 0.05% to 1.1678 CHF. |

EUR/CHF and USD/CHF, December 05(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is confined to narrow ranges against the euro and yen, straddling unchanged levels in the Asian session and the European morning. The action in elsewhere. The British pound is the weakest of the majors, paring 0.4% against the greenback, though around $1.3425, it can hardly be considered weak. A month ago, sterling was a few cents lower. Still, its gains reflected two things: broader dollar weakness and optimism on Brexit talks. The British government was in denial, and perhaps because of this, many investors do not recognize the conflicting and mutually exclusive demand s that have been unleashed by opening the proverbial Pandora’s Box. Specifically, there are three issues the UK needs to address. the role of the ECJ to protect EU citizens in the UK after Brexit, the Irish border, and making good on its financial commitments. |

FX Daily Rates, December 05 - Click to enlarge |

| Since the end of March when the UK triggered Article 50 there has only been apparent movement on the funds, and it was belated at that. The ECJ represents encroachment upon sovereignty that antagonizes many who advocate the UK leaving the EU. The EU, of course, sees it quite differently. We have highlighted the mutually exclusive demand over the Irish border. The EU and Ireland refuse to accept a hard border between Northern Ireland the Republic of Ireland. The DUP, which the Tory government’s survival rests, refuses to countenance a hard border between Northern Ireland of the UK.

Moreover, upon hints that May was going to accept the EU and Ireland position, the DUP expressed its disapproval (via phone call in the middle of May’s lunch with Juncker, which she had to take as the future of her government was likely threatened). Some officials in Scotland and London, wanted the same privilege of being allowed to remain in the single market. It indeed a sticky wicket. |

FX Performance, December 05 - Click to enlarge |

United KingdomUK data were disappointing. The BRC like-for-like retail sales for November showed consumers still reluctant to buy non-essentials. Food sales were up and that helped blunt the impact of the decline in non-food sales. Auto registrations (proxy for sales) remain depressed. The -11.2% year-over-year in November compares with a gain of nearly 3% last November. The service PMI fell to 53.8 from 55.6. It offset the better manufacturing survey and the composite fell to 54.9 from 55.8. |

U.K. Services Purchasing Managers Index (PMI), Nov 2017(see more posts on U.K. Services PMI, ) Source: Investing.com - Click to enlarge |

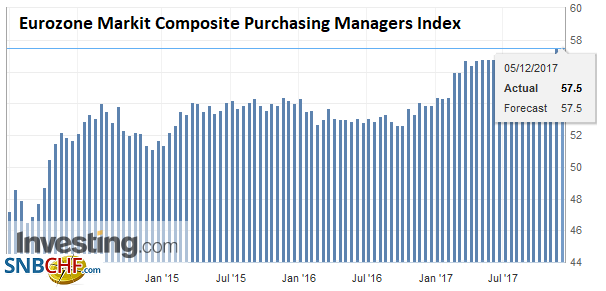

EurozoneThe final eurozone service and composite PMIs were spot on the flash readings. However, its masks some new news. |

Eurozone Services Purchasing Managers Index (PMI), Dec 2017(see more posts on Eurozone Services PMI, ) Source: Investing.com - Click to enlarge |

Eurozone Markit Composite Purchasing Managers Index (PMI), Dec 2017(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

|

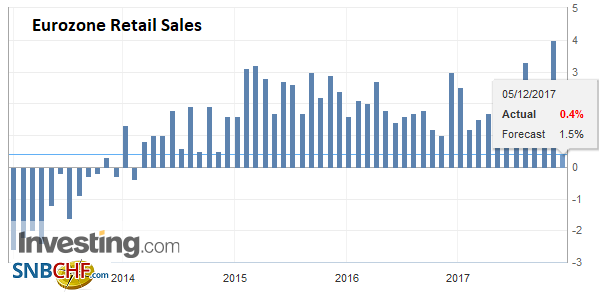

Eurozone Retail Sales YoY, Oct 2017(see more posts on Eurozone Retail Sales, ) Source: Investing.com - Click to enlarge |

|

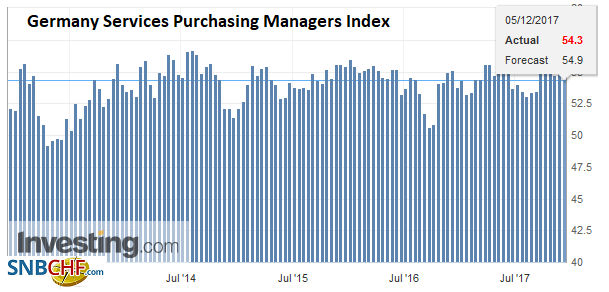

GermanyGerman service PMI was revised to 54.3 from 54.9. It was 54.7 in October, but surprisingly it is now lower than it was last November (when it was at 55.1). |

Germany Services Purchasing Managers Index (PMI), Dec 2017(see more posts on Germany Services PMI, ) Source: Investing.com - Click to enlarge |

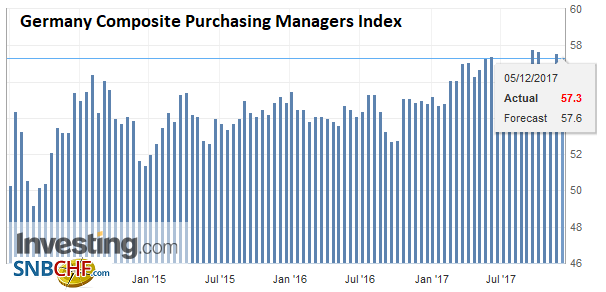

| Owing to the strength of manufacturing, the composite PMI is at a lofty 57.3 (57.6 flash and 56.6 in October). |

Germany Composite Purchasing Managers Index (PMI), Dec 2017(see more posts on Germany Composite PMI, ) Source: Investing.com - Click to enlarge |

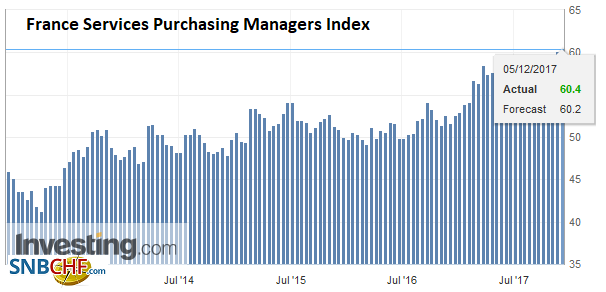

FranceFrench service and composite readings were revised slightly higher from the flash readings. |

France Services Purchasing Managers Index (PMI), Dec 2017(see more posts on France Services PMI, ) Source: Investing.com - Click to enlarge |

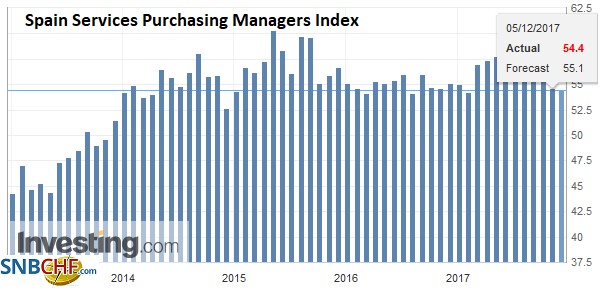

ItalyItaly also report strong data, while Spain was more mixed, but the composite ticked up. The disappointment of the day though comes from the October retail sales. It fell 1.1% on the month. |

Italy Services Purchasing Managers Index (PMI), Nov 2017(see more posts on Italy Services PMI, ) Source: Investing.com - Click to enlarge |

SpainEconomists were looking for a 0.7% decline. The data means that European retail sales grew only 0.4% over the past year, despite falling unemployment and among the strongest growth seen in over a decade. |

Spain Services Purchasing Managers Index (PMI), Nov 2017(see more posts on Spain Services PMI, ) Source: Investing.com - Click to enlarge |

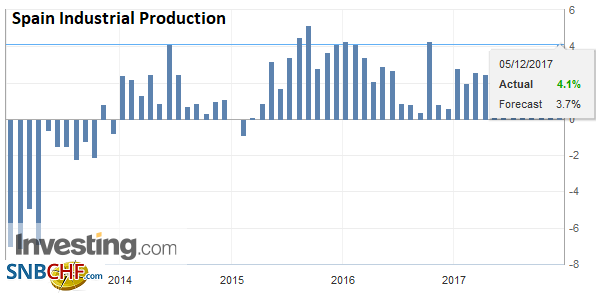

Spain Industrial Production YoY, Oct 2017(see more posts on Spain Industrial Production, ) Source: Investing.com - Click to enlarge |

|

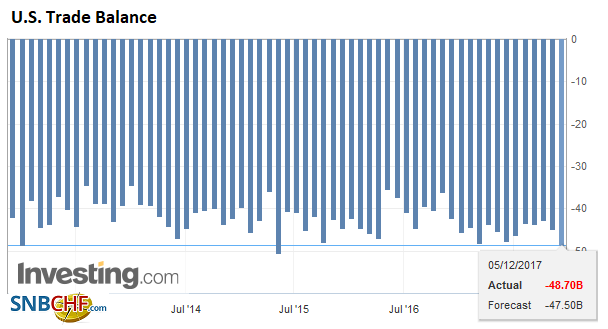

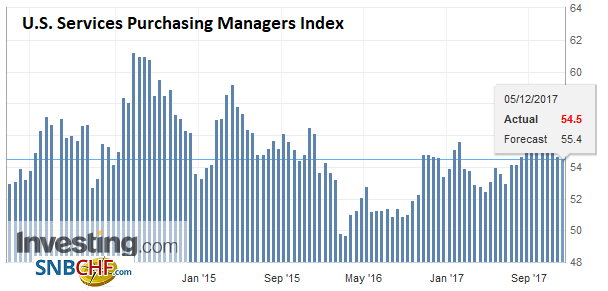

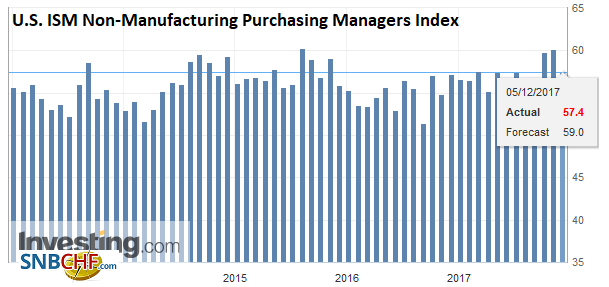

United StatesWhile the US sees the October trade balance (likely wider deficit despite the amazing energy story) and service PMI and ISM, the real focus is elsewhere for investors. |

U.S. Trade Balance, Oct 2017(see more posts on U.S. Trade Balance, ) Source: Investing.com - Click to enlarge |

| The tax reform that the Senate passed early this past Saturday retained the Alternative Minimum Tax for corporations (and some individuals). rushed. |

U.S. Markit Composite Purchasing Managers Index (PMI), Nov 2017(see more posts on U.S. Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

| This came as a surprise to many as earlier drafts had not included it. If in the final version, it would of the other tax cuts. |

U.S. Services Purchasing Managers Index (PMI), Nov 2017(see more posts on U.S. Services PMI, ) Source: Investing.com - Click to enlarge |

| It is seen hurting technology companies and insurers the most, according to some reports. There has been some suggestion that its inclusion may have been an oversight as the bill was rushed. |

U.S. ISM Non-Manufacturing Purchasing Managers Index (PMI), Nov 2017(see more posts on U.S. ISM Non-Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

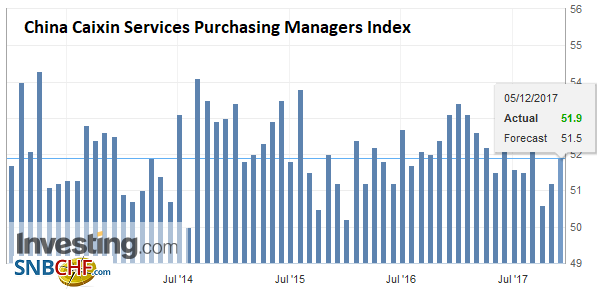

China |

China Caixin Services Purchasing Managers Index (PMI), Nov 2017(see more posts on China Caixin Services PMI, ) Source: Investing.com - Click to enlarge |

On the other hand, the Australian dollar is the strongest of the major currencies. Its 0.6% gain is seeing it probe three-week highs near $0.7650. The market put more weight on the firm PMI (composite 54.3 from 53.1) and better retail sales (0.5% vs. 0.3% expected and a revised 0.1% gain in September, which had initially been reported as flat), than on the slightly wider Q3 current account deficit and the failure of net exports to add to Q3 GDP (flat compared with expectations for 0.25% after 0.30% in Q2). The first look at Q3 GDP will be released in Australia on Wednesday. A 0.7% on a quarter-over-quarter basis, about on par with Q2.

The Aussie moved higher on the data, but remained firm after the central bank meeting. The RBA, as widely expected, left the cash rate at 1.5%. However, the comments seem more optimistic on wage growth, and in any event, the central bank did not seem to be on the verge of easing policy. Some observers have been playing up that scenario especially considering the weakening of house prices. Australia’s two-year yield had dipped below the US 2-year yield last week, but today’s nearly 6 bp increase by Australia puts the rate back on top, and may be lending the Aussie some support. A convincing move above $0.7650 could see $0.7700-$0.7730.

For the better part of two weeks now, the euro has been consolidating its recovery in the first several weeks of November. It has found support near $1.1800 and has struggled to finish the North American sessions above $1.19. The near-term price action may be guided by the uptrend line drawn off the November 7 low, and several lows since then, and comes in near $1.1840 today. It was tested and held in early Europe today.

The poor showing of the US tech sector weighed on Asian equities today. The net loss of the MSCI Asia Pacific index was negligible, but it was the seventh consecutive loss. For the record, it is up about 25.7% year-to-date. European bourses are lower as well. The Dow Jones Stoxx 600 is off nearly 0.5%, led by health care and information technology. It is giving back around half of yesterday’s gains. It is up about 6.7% year-to-date. The MSCI Emerging Markets Index is off 0.4% today. Yesterday’s 0.55% gains broke a three-day slide. It is up 29.6% year-to-date.

The S&P 500 gapped higher, rallied a bit more to new record highs and the proceeded to retreat all session to close on its lows. It is largely flat now. It closed near 2639. A break of 2628 warns of the risk of a retest on 2600 is a retracement objective and where the 20-day moving average is found. Since late August, the S&P 500 has closed only once (November 15) below this average.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,China Caixin Services PMI,EUR/CHF,Eurozone Markit Composite PMI,Eurozone Retail Sales,Eurozone Services PMI,France Services PMI,Germany Composite PMI,Germany Services PMI,Italy Services PMI,newslettersent,Spain Industrial Production,Spain Services PMI,SPY,U.K. Services PMI,U.S. ISM Non-Manufacturing PMI,U.S. Markit Composite PMI,U.S. Services PMI,U.S. Trade Balance,USD/CHF