Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

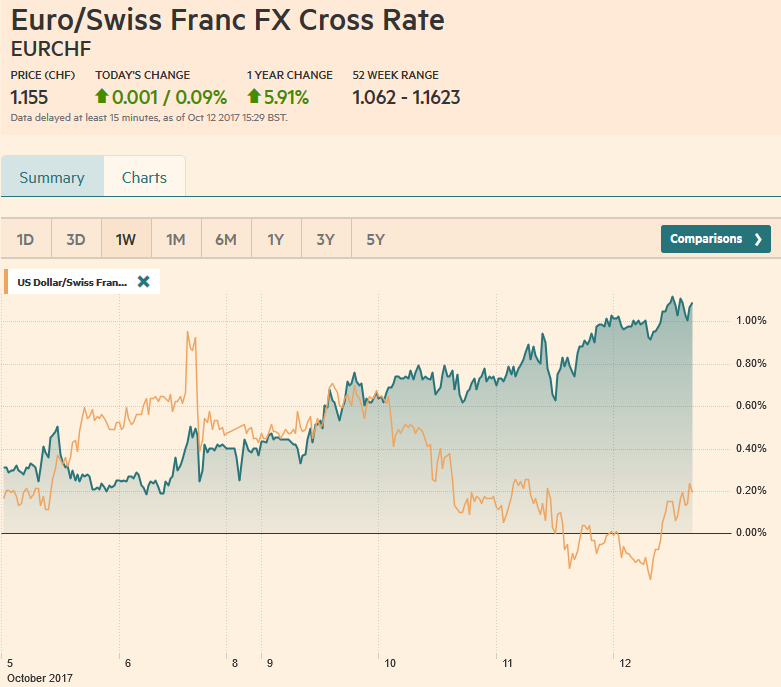

Swiss FrancThe Euro has risen by 0.09% to 1.155 CHF. |

EUR/CHF and USD/CHF, October 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesFollowing the release of the FOMC minutes from last month’s meeting, the consensus narrative that has emerged says that it was dovish because there is a growing worry the reason inflation fell is not simply due to transitory factors. This explains, according to the narrative the dollar’s losses and the stock market rally. It seems reasonable until one looks closer. The best proxy for Fed expectations is not the dollar or the 10-year yield or stocks. It is the Fed funds futures and the short-end of the coupon curve. The implied yield on the December 2018 Fed funds futures rose one basis point yesterday. The two-year note yield rose half a half a basis point yesterday. The signal is not in the magnitude of the move but direction. The market has come to accept a December rate hike, just as it had to be led by the hand to recognize the March hike. It has been skeptical of hikes next year. Consider that the effective average Fed funds rate has been 1.16% since June’s hike. A December hike will bring it 1.42%. A hike in 2018 would then lift the effective average rate to 1.67%. The first Fed funds futures contract that has an implied yield at that level is March 2019. |

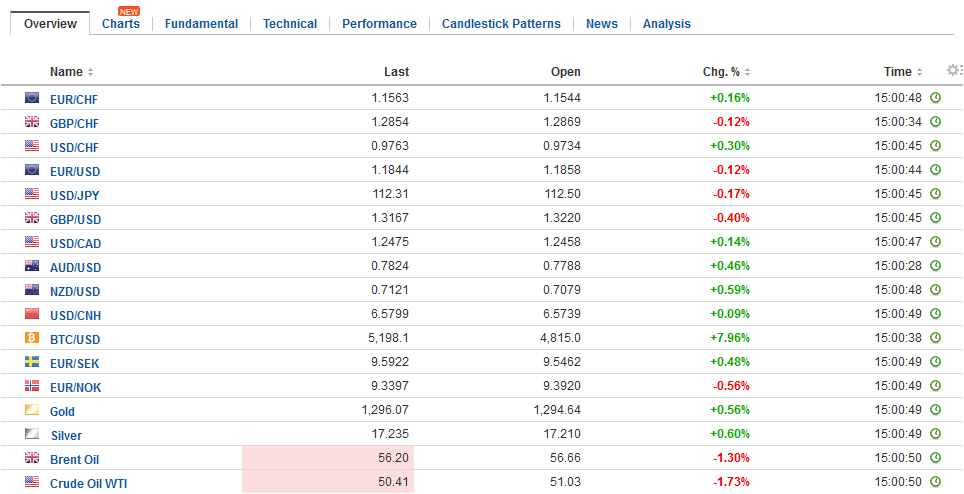

FX Daily Rates, October 12 - Click to enlarge |

| What of the dollar? It had sported a softer profile this week after reversing higher following the US jobs data at the end of last week when in our view, the market had nearly completely discounted a Dec rate hike, and the 10-year yield reached the upper end of its six-month trading range. We thought that the focus would shift back to the ECB from the US employment data. Perhaps, also contributing to the pullback in US yields are the concerns about the status of tax reform.

The euro is extending its four-day advance into today’s session. The gains have carried it to the $1.1880, which corresponds to 50% of the drop since reaching almost $1.21 on September 8 and bottoming last Friday near $1.1670. The next retracement objective is near $1.1930. We anticipated this euro bounce and suspected that late longs are vulnerable to tomorrow’s US CPI and retail sales report that will be impacted by the storm, and the tight inventory/sales balances for some household goods. Again, we point out that while the September jobs report was skewed by the storm, the upward revision to August average hourly earnings was not. |

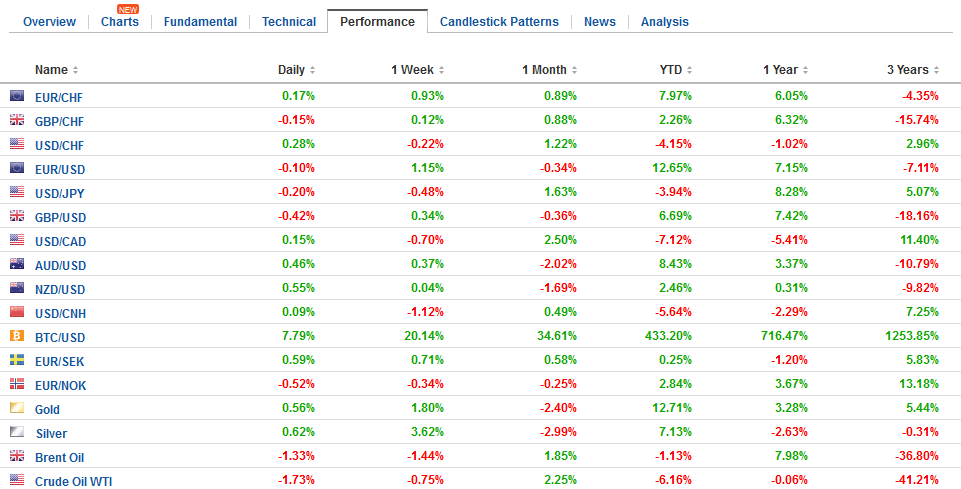

FX Performance, October 12 - Click to enlarge |

EurozoneThe enthusiasm for Spanish assets is somewhat diminished today. The bonds are flat while European bonds are mostly firmer. The stock market is off, but holding up better than most other major European markets. Rajoy has taken a measured step in the face of Catalonian officials signing a declaration of independence and then many signing a decree suspending it. Rajoy has given officials until Monday morning to clarify their stance. And if they insist on claiming independence, they will be given another three day grace period to reconsider before Rajoy sets into motion the process that would force the Catalan administration out of office. Rajoy appears to have the opposition Socialists support. Rajoy did appear open to the Socialist proposal for a committee to be established to discuss regional powers, but not to enable a referendum for independence. Following the recent national reports from Germany, Italy, and Spain, it is not surprising that eurozone industrial output surged in August. The 1.4% increase was the largest since January, and the July series was revised to 0.3% from 0.1%. These kind of reports that show the eurozone economy continues to expand at a robust and above-trend pace are a bit beside the point ironically. The message from the ECB’s leadership is about disappointment with price pressures not sluggish growth. The issue at the upcoming ECB meeting is the tradeoff between the size of the continued asset purchases and the length of the program. Also, the ECB’s chief economist also suggests more information about the reinvesting of maturing proceeds, which market estimates at around 15 bln euros a month next year. If the ECB were to cut its new purchases to 30 bln euro a month, half of what is it’s currently buying, the roll-over would bring the gross purchases to 45 bln euros a month. |

Eurozone Industrial Production YoY, Aug 2017(see more posts on Eurozone Industrial Production, ) Source: Investing.com - Click to enlarge |

JapanIn addition to the euro’s streak, there is another notable streak underway: Japanese stocks. The Nikkei rose for the eighth consecutive session and now is at its highest level since 1996. This advancing brings the Nikkei to a solid if not spectacular 9.6% rise for the year. Japanese stocks have been helped by the global rally and growing confidence that Abe and the LDP will win the snap election later this month. The MOF will provide new data tomorrow, but we note that in the last week of September, the most recent data, foreign investors snapped a nine-week streak in which they were net sellers of Japanese shares. Year-to-date, foreign investors have sold $17 bln of Japanese and it all took place in Q3 and most of that (~$15.5 bln) in September. The best indicator of the dollar-yen exchange rate remains the 10-year US yield. The correlation of the percentage change of the two over the past 60 days (0.81) appears to be the highest since at least the mid-1980s. After peaking at 2.40% before last weekend, the yield slipped to 3.32% earlier today. The dollar is trading inside yesterday’s range against the yen, which is inside Tuesday’s range. The 20-0day moving average is found near JPY112.30. The dollar has not closed below this average since September 11. On the other hand, it has not closed above its five-day moving average (~JPY112.55) in a week. |

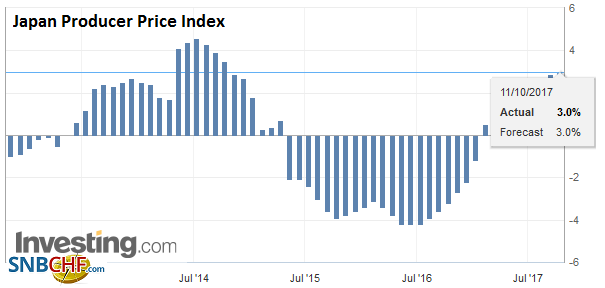

Japan Producer Price Index (PPI) YoY, Sep 2017(see more posts on Japan Producer Price Index, ) Source: Investing.com - Click to enlarge |

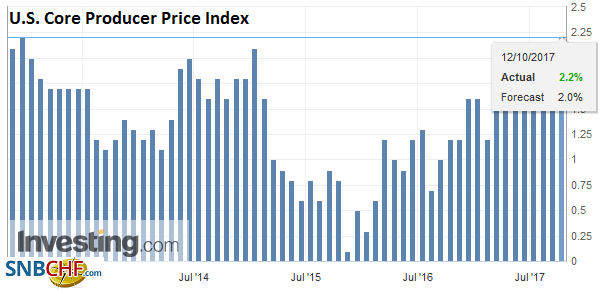

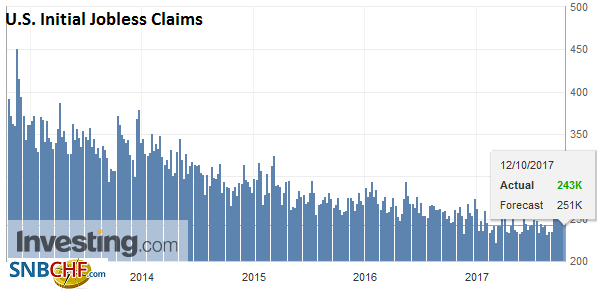

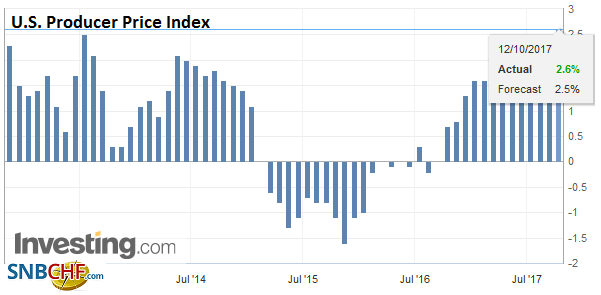

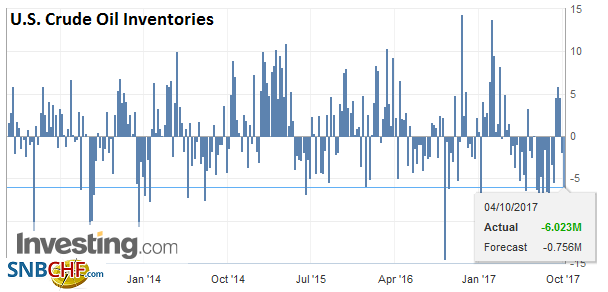

United StatesThe North American session features various speeches from the World Bank and IMF meetings, weekly initial jobless claims, which should continue to normalize, and September PPI. The headline measure of producer prices is expected to rise, but the core measure is expected to be flat at 2.0%. Canada reports news house price. The US Department of Energy reports the official measure of crude stocks. A third weekly drawdown is expected (~6 mln barrels). |

U.S. Core Producer Price Index (PPI) YoY, Sep 2017(see more posts on U.S. Core Producer Price Index, ) Source: Investing.com - Click to enlarge |

U.S. Initial Jobless Claims, 12 October 2017(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

|

U.S. Producer Price Index (PPI) YoY, Sep 2017(see more posts on U.S. Producer Price Index, ) Source: Investing.com - Click to enlarge |

|

U.S. Crude Oil Inventories, Oct 2017(see more posts on U.S. Crude Oil Inventories, ) Source: Investing.com - Click to enlarge |

|

France |

France Consumer Price Index (CPI), Sep 2017(see more posts on France Consumer Price Index, ) Source: Investing.com - Click to enlarge |

Two other short points to note. First, Sweden’s CPI disappointed and the market immediately took it out on the Swedish krona. It is the weakest of the major currencies, losing about 0.55% against both the dollar and euro. The market appeared to have been anticipating that a firm inflation report would encourage the end of the super-easy monetary stance in the face of strong growth and inflation above target. For the record, the CPIF, which uses fixed mortgage interest rates, rose 0.2%, half of the median expectation, for an unchanged 2.3% year-over-year rate. Second, the New Zealand dollar has underperformed over the past few sessions, until today when it is the strongest of the major currencies (0.50%) as New Zealand First tries to make up its mind which side to join. Ideologically it would seem to have more in common with the National government, but pragmatism and the desire to share power may be more important.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: $EUR,$JPY,$TLT,EUR/CHF,Eurozone Industrial Production,France Consumer Price Index,Japan Producer Price Index,newslettersent,U.S. Core Producer Price Index,U.S. Crude Oil Inventories,U.S. Initial Jobless Claims,U.S. Producer Price Index,USD/CHF