Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

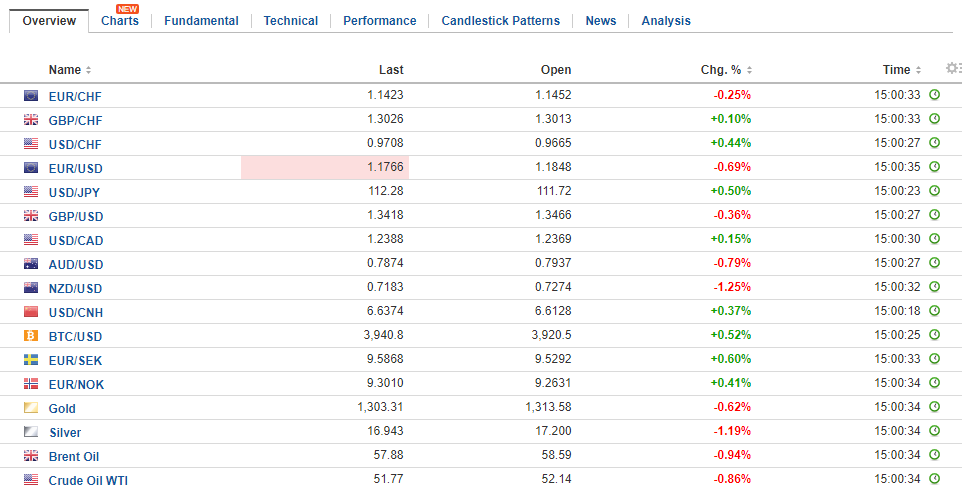

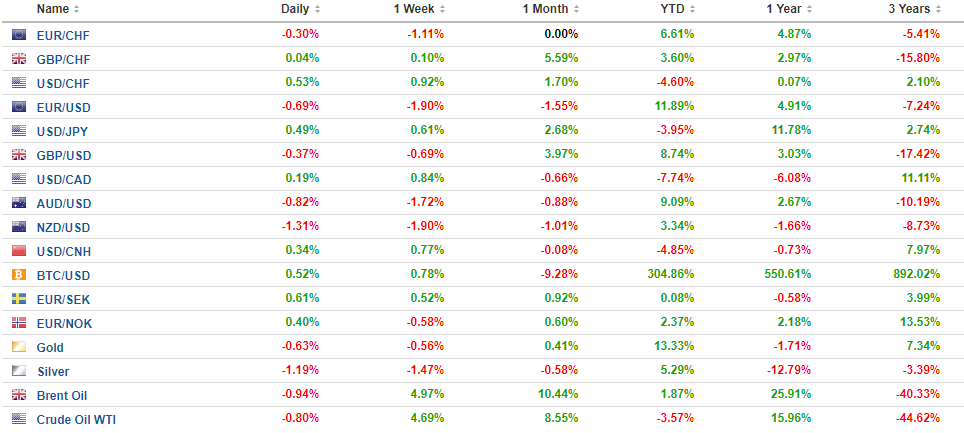

Swiss FrancThe Euro has fallen by 0.01% to 1.1446 CHF. |

EUR/CHF and USD/CHF, September 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is firmer against most major currencies today. The implications the Jamaica coalition in Germany is understood to be less likely to support a new vision for Europe in the aftermath of Brexit and the Great Financial Crisis. The euro’s low for the year was set at the very start near $1.0340. The first quarter or so was spent consolidating the gains in H2 16. It was trading below $1.06 in early April. However, the turn, in the form of a gap higher opening on April 24, as it becomes clear that the so-called populist-nationalist moment was not sweeping through Europe. This coincided with an inflation scare that sent the euro toward $1.15 by mid-year. The euro has been consolidating its gains this month and appears to have carved out a topping pattern. Perhaps it has been helped by a seeming pattern of unsourced European official comments when the euro pokes through $1.20. Momentum traders are getting frustrated. It has become more expensive to short the dollar against the euro. The spread between US Libor and the one-year cross-currency basis swap is near -35 bp which is dearest the dollars have been here in H2 (the spread bottomed at the end of last year near -52 bp). The two-year interest rate differential is near 2.14% today, the highest since March. It has steadily climbed since the end of Q2 when it reached almost 1.90%. |

FX Daily Rates, September 26 - Click to enlarge |

| The euro is making a new low for the month today. A convincing break of $1.18 would seem to confirm the topping pattern. The initial objective is near $1.16, though last month’s low was seen near $1.1660. A more aggressive target is near $1.1425, which corresponds to a 38.2% retracement of this year’s gains. There is an option for nearly 980 mln euros struck at $1.1825 that expires in NY today.If the euro-dollar exchange rate has become a bit less sensitive to interest rate differentials, the dollar-yen rate remains very sensitive. The correlation (on percent change) over the past 60 sessions of US 10-year yield and dollar-yen remains historically high (~0.81). In fact, it does not look like it has been higher since at least 2000 than it is today. The 10-year US Treasury yield reached a high on September 20 near 2.29%. The dollar reached a high against the yen the next day near JPY112.70. Both have eased since, and today initial support in both markets is seen near yesterday’s lows (~JPY111.50 and 2.21%). There is a $660 mln option struck at JPY112 that expires in NY today. It may not be in play unless US yields pop. |

FX Performance, September 26 - Click to enlarge |

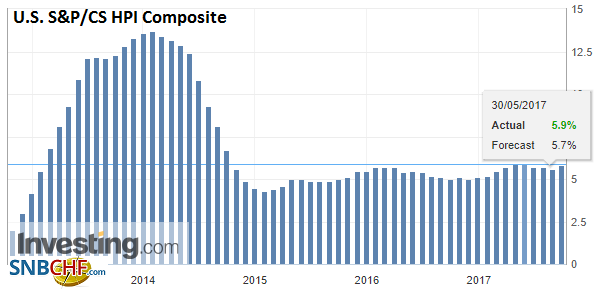

United StatesHowever, the US economic calendar is light. S&P CoreLogic house prices are released shortly before the stock market opens, the report is not typically a market mover. |

U.S. S&P-CS HPI Composite - 20 n.s.a. YoY, Jul 2017 Source: Investing.com - Click to enlarge |

| August new home sales are reported at the same time as the options expire. A small bounce is expectedafter the outsized 9.4% drop in July. Meanwhile, Fed officials speak all morning, with the highlight being Yellen at 12:45 pm ET. It is her first public statements since last week’s press conference. |

U.S. New Home Sales, Aug 2017(see more posts on U.S. New Home Sales, ) Source: Investing.com - Click to enlarge |

| Also in the US today, there is a special Republican contest for Attorney General Sessions’ Senate seat. The contest is between a Republican establishment pick, Strange, and Moore, a candidate more at home with the Freedom Caucus. The election is billed as a contest for the soul of the Republican Party. While the market impact is likely to be minor, it may shape expectations for next year’s primaries and mid-term elections (November 2018). |

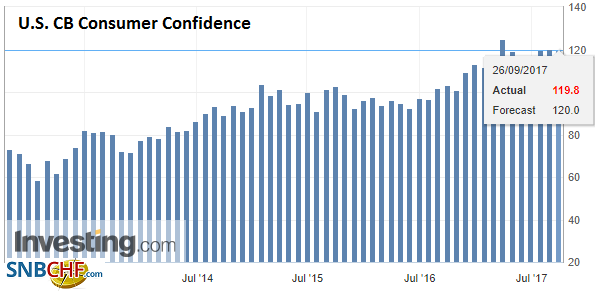

U.S. CB Consumer Confidence, Sep 2017(see more posts on U.S. CB Consumer Confidence, ) Source: Investing.com - Click to enlarge |

Sterling is being protected by ideas that the BOE will hike rates, becoming the third G7 country to do so this year (US and Canada being the other two). Although May’s speech last week did not seem to be sufficient for EU officials, it does not seem to be much of a factor for the market. Sterling is consolidating the run-up in the first half of the month. Yesterday’s sterling recorded a low near $1.3430, the lowest level since the day after the BOE meeting and its surprisingly hawkish tone. A break of $1.3400 would set up a test on the $1.3300-$1.3350 area, where several technical levels converge.

Meanwhile, the euro is breaking down against sterling. It is at two-month lows and is threatening the mid-July lows near GBP0.8740 and key technical support near GBP0.8730. A break of there could fan ideas of a move toward GBP0.8500 as the parity plays are unwound. The euro is pinned near yesterday’s lows against the yen (~JPY132). A break of the JPY131.70-JPY131.80 could spur a move toward JPY131, and possibly JPY130.

Oil is coming in touch softer today after Brent reached a two-year high yesterday and WTI reached a four-month high. The proximate trigger was news that Turkey threatened to cut of oil flowing from Iraq’s Kurdistan. Iraq does not recognize the referendum for independence by the Kurds, which would aggravate Turkey’s challenges. At the same time, major producers are talking the market up, and reports suggest production cuts are beginning to bite. Still, there is a significant spread between WTI and Brent. In fact, the roughly $6.60 spread is the widest in a couple of years. The deep discount of WTI speaks to relative supply, but also some unique US developments. Many cite the ongoing technological progress. This is part of the story, but so is cheap credit and a certain regard for the environment. The November contract rose to a little more than $52.10 but is coming off now. Initial support is seen today in the $51.25-$51.50 area.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$EUR,$JPY,$TLT,EUR/CHF,newslettersent,OIL,U.S. CB Consumer Confidence,U.S. New Home Sales,U.S. S&P/CS HPI Composite - 20 n.s.a.,USD/CHF