Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

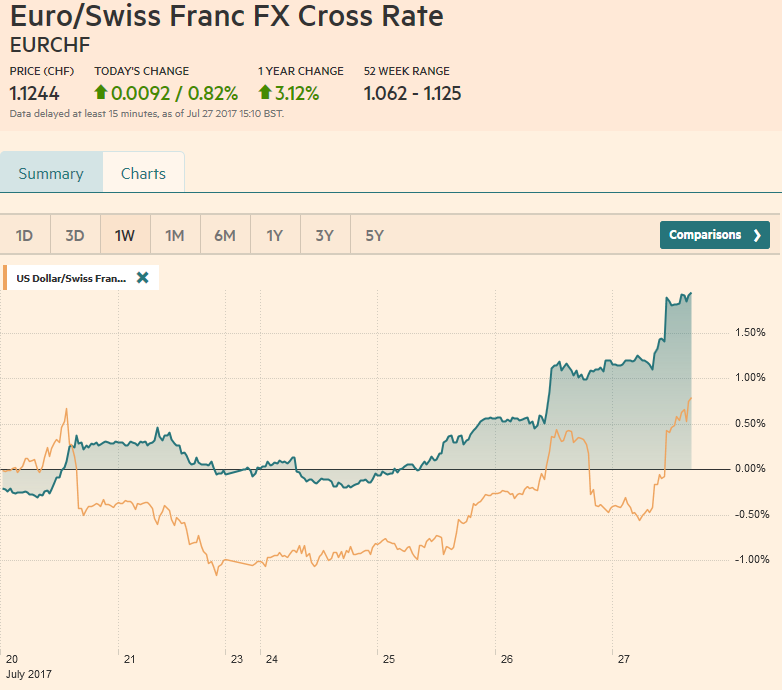

Swiss FrancThe Euro has risen by 0.82% to 1.1244 CHF. |

EUR/CHF and USD/CHF, July 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is narrowly mixed after selling off following the FOMC statement. Sometimes the narrative explains the price action, and sometimes the price action explains the narrative. This seems to be the case of the latter. The dollar and interest rates fell, and so the Fed was dovish. First, let’s turn to the fall interest rates. At the end of last week, the two-year note yields 1.34%. It rose slightly at the start of the week and fell slightly yesterday. It sits at 1.35% now. The December Fed funds futures contract finished last week with an implied yields of 1.225%. It had risen to 1.24% on Tuesday, but finished yesterday at 1.225%. This shows that expectations for the trajectory of Fed policy have not changed. The 10-year yield, which has less directly to do with Fed policy, is five basis points higher this week. Second, consider that the dovish read of the consensus narrative was based the changed characterization of the current situation not in the forward looking section. The FOMC statement said that inflation was “below target” (not “persistently” as some press accounts characterized it) as opposed to the previous statement in June that said, “somewhat below target.” The FOMC did not change its assessment that inflation would move toward its target in the medium term. Third, consider the inflation data that have been released since the mid-June meeting. There was the May PCE deflator released at the end of June. As was seen with the May CPI, which was released a few hours before the June FOMC meeting concluded, the core PCE deflator eased for the fourth consecutive month. There was the June CPI in mid-July. The headline rates eased to 1.6% from 1.9%, but the core rate was unchanged at 1.7%. This is to say that there has been limited high frequency price data over the past six weeks, which is also to limit the significance we attach to the word “somewhat” in the economic description. |

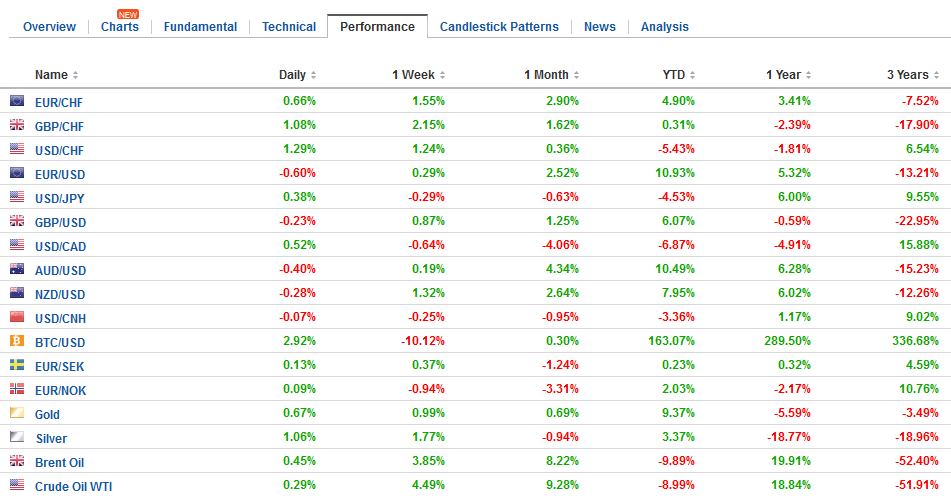

FX Daily Rates, July 27 - Click to enlarge |

| The bottom line is that the scenario we suggested after the June FOMC meeting remains most likely. That is for the FOMC to announce in September (“relatively soon”) that it will to completely rollover maturing securities but will allow some to roll-off. This will allow it to retire an equivalent amount of excess reserves, and through this allow its balance sheet to shrink. By doing so in September, it also succeeds in distancing its balance sheet operations from monetary policy. It also allows the Fed to “closely watch” the evolution of prices (inflation). The CME calculation puts the odds of a December hike near 47% while the Bloomberg model is a little lower.

The news stream is light. Of note, Moody’s raised its outlook for China’s banking system to stable from negative. It expressed confidence in its regulators to manage the risks emanating from the shadow banking sector and forecast that the growth of new bad loans will moderate. Recall Moody’s cut the sovereign rating in May on its rising debt levels. Today’s announcement culminates an eight-month process whereby Moody’s upgraded rating on medium-sized banks last October, and five large banks a few months ago. Lenders with stable outlooks by Moody’s accounts for a nearly 90% the total assets of the Chinese banks that it rates. Asian shares rallied. The MSCI Asia Pacific Index rose nearly 1% to new multi-year highs. Favorable earnings reports by Samsung and Nintendo were among the highlights. The Nikkei advanced slightly even though the yen had strengthened. European markets are mixed, and the Dow Jones Stoxx 600 is little changed. Health care and industrials are the main drags, while telecom and consumer staples sectors are up more than 1%. It is an important earnings day for European companies, and some of the divergences in performance are due to the story stocks. |

FX Performance, July 27 - Click to enlarge |

United StatesThe US economic calendar includes the weekly jobless claims (expected to bounce back after last week unexpected fall), preliminary durable goods orders for June (expect a strong recovery in the headline after soft May), the June merchandise balance (expect little change) and wholesale and retail inventories. Economists will fine tune their forecasts for Q2 GDP which will be reported tomorrow. We have penciled in 2.25%. The Senate Banking Committee holds confirmation hearings on Fed nominee Quarles today. Also, the Senate continues to debate and vote on various proposals to pass a health care reform bill that would get the process to move to the reconciliation phase where a joint committee of Republicans would bring the House and Senate versions together. Meanwhile, the House is slated to start a five-week holiday on Friday, and tax reform and the FY18 budget (spending authorization) also appears to be stalling as the split between the moderate and conservative parts of the Republican coalition are at odds. |

U.S. Initial Jobless Claims, July 27 2017(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

Eurozone |

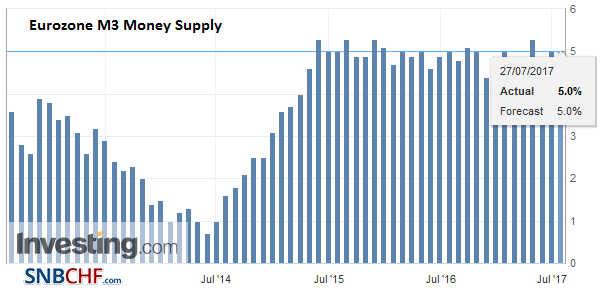

Eurozone M3 Money Supply YoY, June 2017(see more posts on Eurozone M3 Money Supply, ) Source: Investing.com - Click to enlarge |

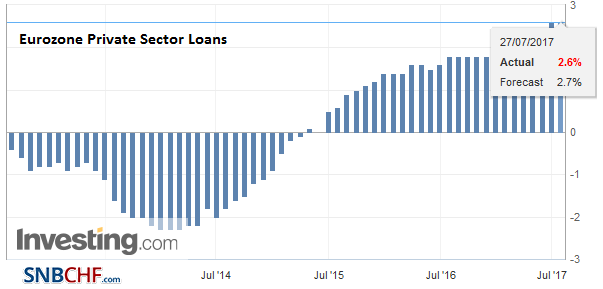

Eurozone Private Sector Loans YoY, June 2017(see more posts on Eurozone Private Sector Loans, ) Source: Investing.com - Click to enlarge |

|

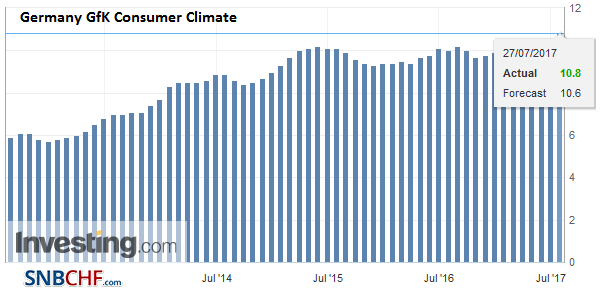

Germany |

Germany GfK Consumer Climate, July 2017(see more posts on Germany GfK Consumer Climate, ) Source: Investing.com - Click to enlarge |

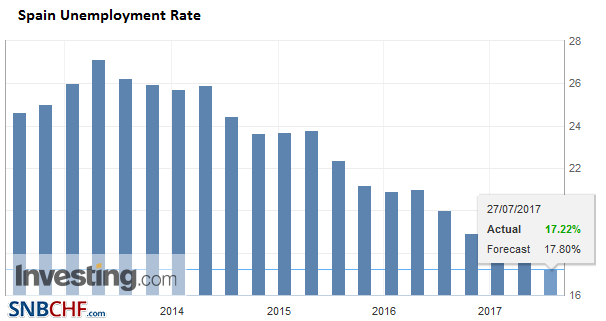

Spain |

Spain Unemployment Rate, Q2 2017(see more posts on Spain Unemployment Rate, ) Source: Investing.com - Click to enlarge |

Full story here Are you the author?

Tags: #USD,$TLT,China,EUR/CHF,Eurozone M3 Money Supply,Eurozone Private Sector Loans,FOMC,Germany GfK Consumer Climate,newslettersent,Spain Unemployment Rate,U.S. Initial Jobless Claims,USD/CHF