Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

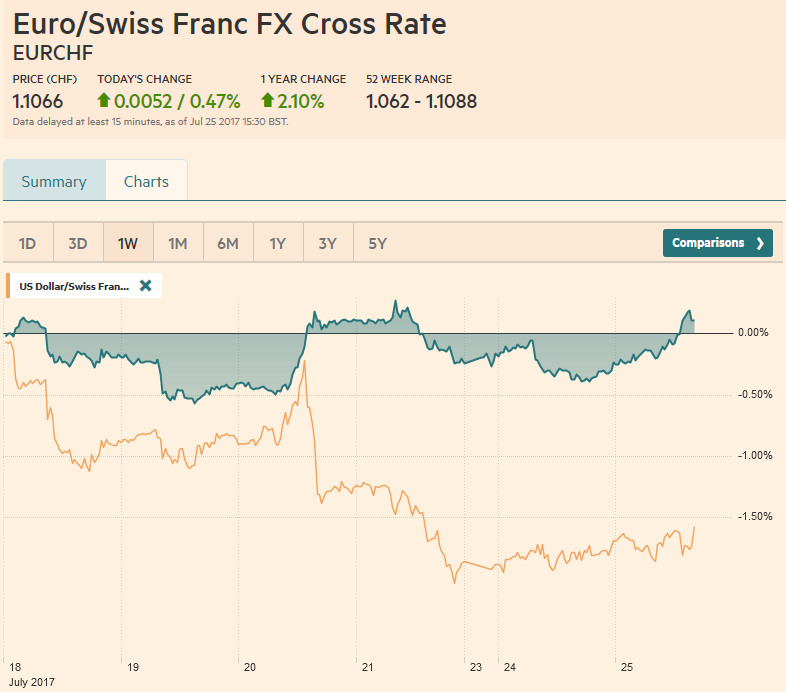

Swiss FrancThe Euro has risen by 0.47% to 1.1066 CHF. |

EUR/CHF and USD/CHF, July 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

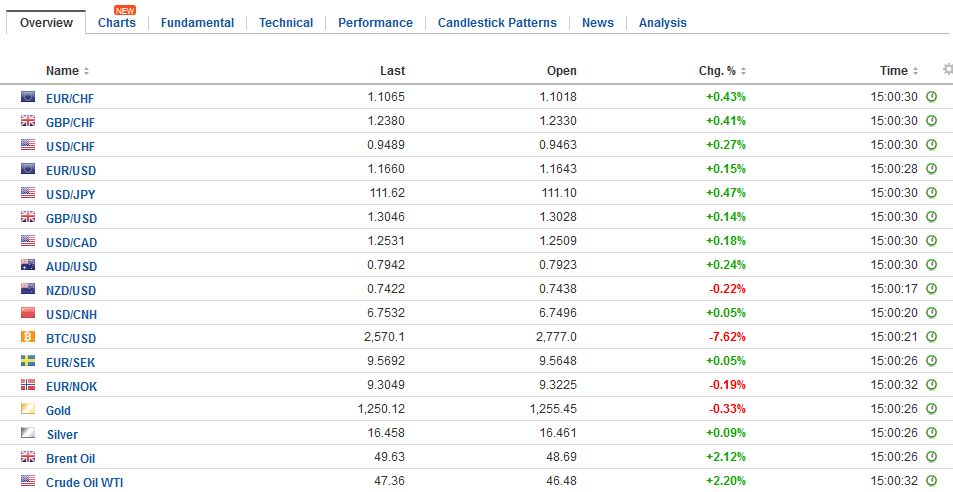

FX RatesThe global capital markets are subdued today; a dearth of fresh news and tomorrow’s FOMC meeting are making for light activity and limited price movement. The US dollar is little changed against most of the major currencies. The net change on the day through most of the European morning is +/- 0.15%. The exception is the Norwegian krone and Swedish krona, which is about 0.25% stronger. Benchmark sovereign 10-year yields are mostly firmer but by less than a single basis point, with some pockets, like Italy, Portugal, and Greece that are doing a bit better. Equity markets are mixed. The MSCI Asia Pacific Index fell 0.2%, its second day of losses, after a ten-day advance. It continues to trade in a narrow range at its best level in nearly a decade. Japanese, Chinese, and Korean shares eased, while most other markets in the region posted small gains. The disappointing news from Alphabet may have weighed on some technology shares in Asia. In Europe, the Dow Jones Stoxx 600 is trying to snap a three-day fall and is up 0.5%, led by the financials and materials. All sectors are higher. The German DAX has been underperforming for about a month, and that pattern continues today. |

FX Daily Rates, July 25 - Click to enlarge |

| The Australian dollar is firm, holding above $0.7900. Tomorrow Q2 CPI will be reported. The headline pace may pick up to 2.2% from 2.1%, but the underlying rates (trimmed mean and weighted mean) were likely stable or even a tad softer. RBA Governor Lowe speaks tomorrow as well. Given last week’s official comments that made the Aussie come off, Lowe’s comments will be scrutinized for clues into rate policy and the comfort level with the currency’s apparent upside breakout.

The Canadian dollar remains firm within yesterday’s ranges after rising past $0.80 yesterday for the first time since May 2016. The US dollar is straddling the CAD1.25 level. The low from May 2016 was near CAD1.2460, but it is difficult to call that support. There is little congestion ahead of the CAD1.2360 area, and the next important technical target is not until closer to CAD1.2160. At the end of the week, Canada report May GDP figures. The year-over-year pace will rise sharply as the May 2016 0.6% decline drops out of the comparison. Canada is poised to be the fastest growing G7 economy this year. Meanwhile, the euro is carving out a little shelf above $1.1600 even if the market appears to be hesitating ahead of last August’s high a little above $1.17. We suspect North American participants may initially try to extend the euros 20-tick range on either side of $1.1650 to the upside. Although the dollar spent a bit of time below JPY111.00 yesterday, it has popped back above and is now threatening to snap a five-day slide. Without better support from US Treasuries, the dollar may struggle to rise above JPY111.60-JPY111.80. |

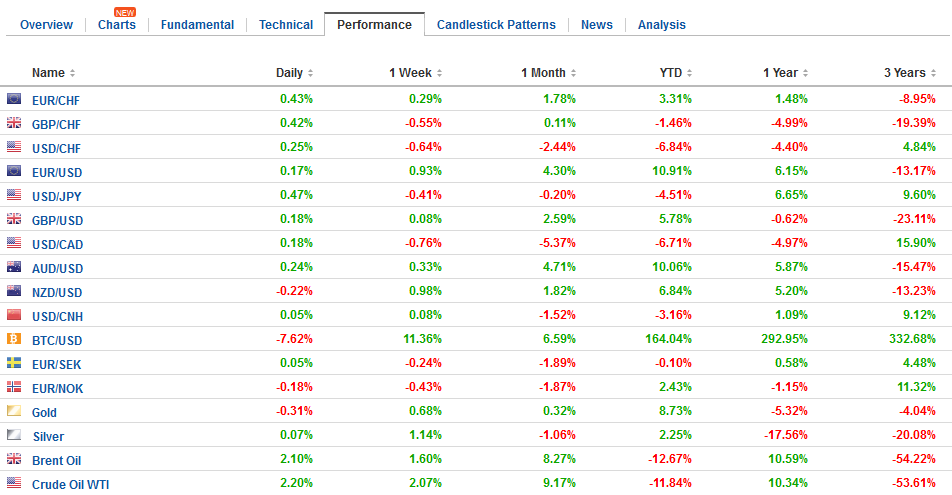

FX Performance, July 25 - Click to enlarge |

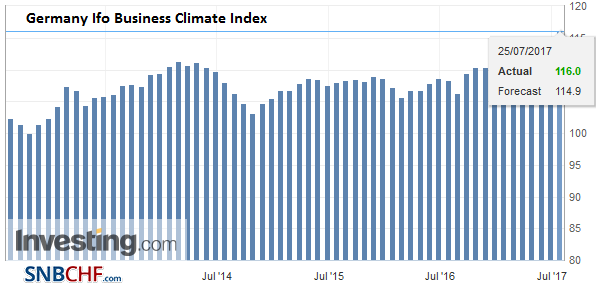

GermanyGerman business confidence remains strong. Even though the flash PMI suggested momentum was moderating, the IFO business survey found that the evaluation of the business climate has never been better (116.0 vs. 115.2). |

Germany Ifo Business Climate Index, July 2017(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

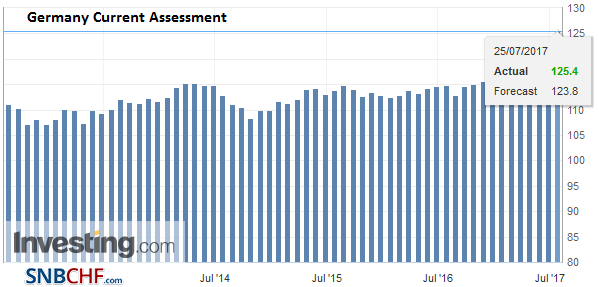

| This is not just a function of the current assessment (107.3 vs. 106.8). |

Germany Current Assessment, July 2017(see more posts on Germany Current Assessment, ) Source: Investing.com - Click to enlarge |

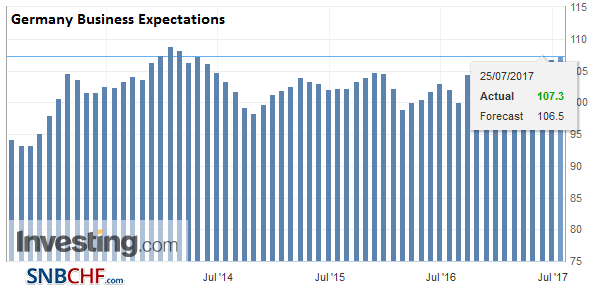

| Also expectations improved (125.4 vs. 124.2) to a new record high, as well. |

Germany Business Expectations, July 2017(see more posts on Germany Business Expectations, ) Source: Investing.com - Click to enlarge |

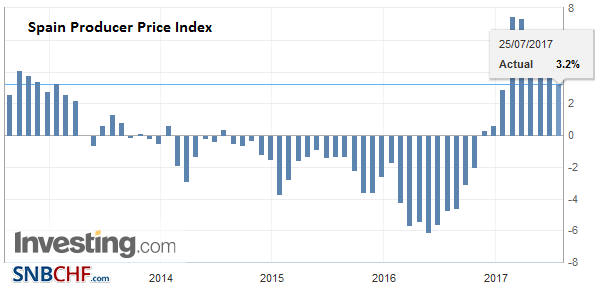

Spain |

Spain Producer Price Index (PPI) YoY, July 2017(see more posts on Spain Producer Price Index, ) Source: Investing.com - Click to enlarge |

United Kingdom

The UK-US trade talks continue today, but there less here than meets the eye. First, the UK make any agreement while it is still a member of the EU, and this is not going to change for 18 months (at least). Second, a new trade deal with the EU may limit what the UK can offer the US. Third, the UK enjoys a trade surplus (merchandise and services) with the US. This runs smack into the US administration’s “America First” thrust and its drive to reduce the US trade deficit.

The UK reports its first look at Q2 GDP tomorrow. A lackluster 0.3% expansion is expected to have followed the 0.2% pace in Q1. This is marked slow down after of the average quarterly expansion of 0.6% over the previous three-quarters. The year-over-year pace may slow to 1.7% from 2.0%. The IMF’s new forecasts trimmed this year’s expectation to 1.7% from 1.8%.

Ahead of tomorrow’s FOMC statement, today’s data will likely be of little consequence. Reports include S&P CoreLogic house prices (edging higher), Conference Board’s consumer confidence (a little softer) and the Richmond Fed manufacturing index (unchanged?). The political focus is on the Senate machinations over the health care efforts.

Before the weekend, the Senate Parliamentarian ruled that several key parts of the replacement bill do not qualify for fast-track rules (where a simply majority can pass it) and instead require 60 votes (which means Democrats). The health care debate has reportedly sapped the resources and time from other efforts. Moreover, housekeeping measures like the debt ceiling and spending authorization (FY18 budget) appear to be also subject to debate within the majority party. The T-bill market is already reflecting some of these considerations.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,Germany Business Expectations,Germany Current Assessment,Germany IFO Business Climate Index,newslettersent,Spain Producer Price Index,USD/CHF