Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

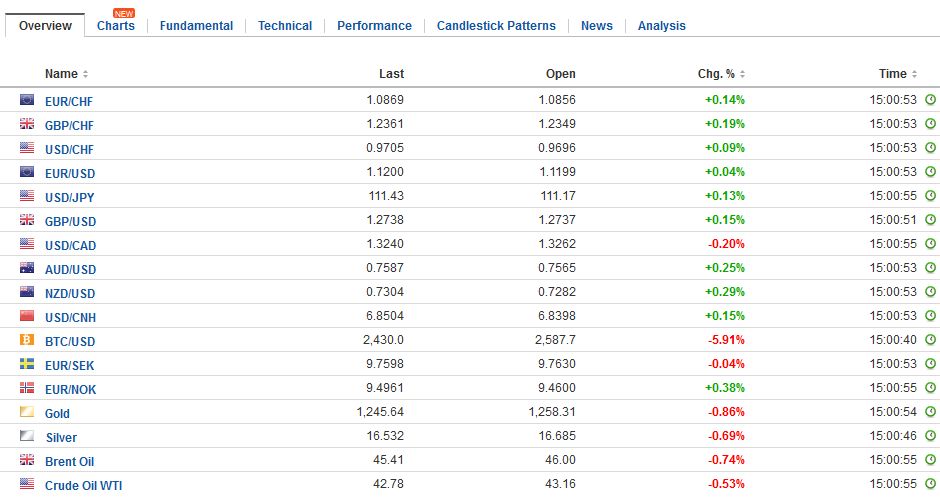

Swiss FrancThe Euro has risen by 0.16% to 1.0871 CHF. |

EUR/CHF - Euro Swiss Franc, June 26(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe US dollar is mostly slightly firmer as North American dealers return to their posts. Ideas that the UK Tories are getting close to a deal with the DUP appears to be lending sterling a modicum of support, as it tries to extend its uptrend into a fourth session. The Japanese yen is the weakest of the majors, rising equities, and yields, spurs the dollar to re-challenge last week’s high near JPY111.80. The way it which Italy has decided, with the EC’s permission, to close the two regional bank at a not insignificant cost to taxpayers was widely criticized in the media and by analysts. Italy’s second-largest bank, Intesa got a sweetheart deal. It is able to take over the failed banks assets, but not liabilities as had been the case recently in Spain. It was also given around 400 mln in guarantees in case some of the asset sour. It was granted about 4.8 bln euros to maintain its capital ratios. Senior bondholders and depositors were kept whole. |

FX Daily Rates, June 26 - Click to enlarge |

| Although we do not often look at it, and Bloomberg does not report it, the IFO service survey slipped to 13-month lows. This gives one the sense that the weakness of the euro, relatively speaking, boosts Germany’s trade sector, which is about goods more than services. Also, importantly, the euro may have initially ticked higher the headline news, but has come off after meeting offers near the pre-weekend high of $1.1210. There is a 525 mln euro option struck at $1.12 that is cut in NY today. Initial support is seen near $1.1175, and it may take a break of the $1.1140-$1.1150 area to be at all noteworthy.

Oil prices are higher for the third session. Recall that the August light sweet crude oil contract closed lower for the fifth consecutive week, but the downside momentum had begun easing after the middle of the week. The general pattern holds for Brent as well. The technical indicators warn that the market is over-extended and a further bounce is likely. We look for a move toward $44.00-$44.50 after closing near $43 before the weekend. |

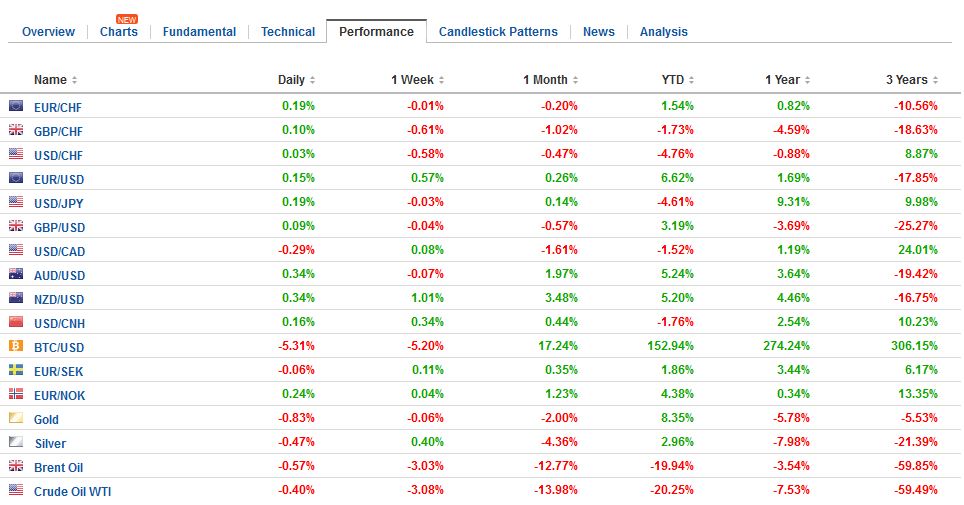

FX Performance, June 26 - Click to enlarge |

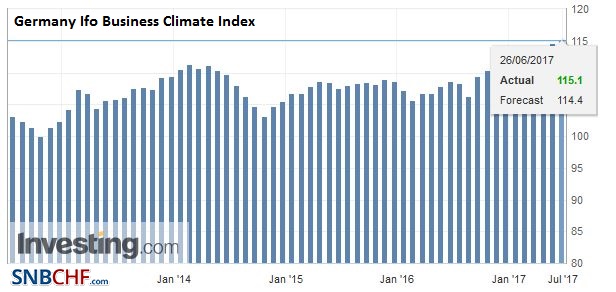

GermanyMeanwhile, the economic news of the day, the German IFO survey failed to excite the market. The survey was better than expected. The overall assessment of the climate ticked up to 115.1 from 114.6. It is the highest level since at least 1991. |

Germany Ifo Business Climate Index, June 2017(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

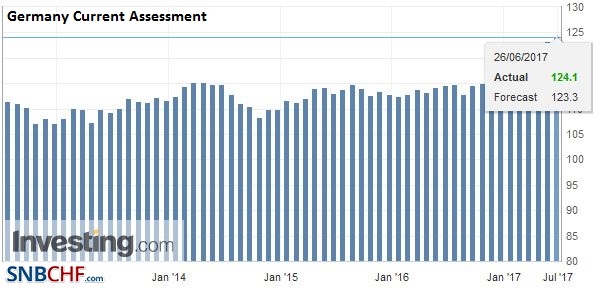

| The evaluation of current conditions rose to 124.1 from 123.3. This is also the highest reading in at least 26 years. |

Germany Current Assessment, June 2017(see more posts on Germany Current Assessment, ) Source: Investing.com - Click to enlarge |

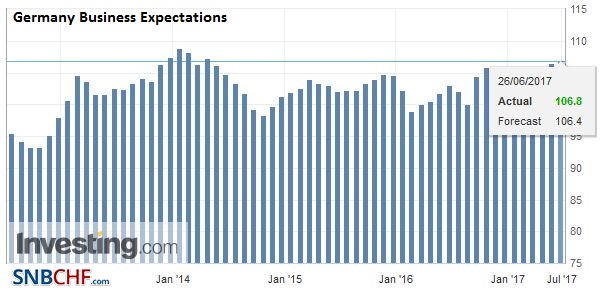

| The expectations component rose to 106.8 from 106.5. It is a three-year high. |

Germany Business Expectations, June 2017(see more posts on Germany Business Expectations, ) Source: Investing.com - Click to enlarge |

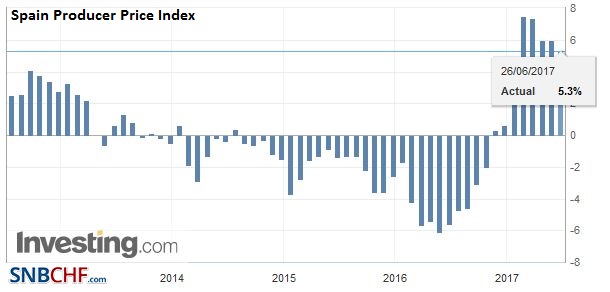

Spain |

Spain Producer Price Index (PPI) YoY, June 2017(see more posts on Spain Producer Price Index, ) Source: Investing.com - Click to enlarge |

United StatesThe US reports durable goods orders for May. The details of the preliminary report (orders excluding aircraft and defense orders, and shipments of the same) are expected to be better than the headline, which probably fell for the second consecutive month. Recall that durable goods orders rose an average of 0.6% in Q4 16 and 1.3% in Q1 17. If durable goods orders fall 0.6% as the median forecast in the Bloomberg survey suggests, then the average for the first two months in Q2 would be -0.7%. |

U.S. Durable Goods Orders MoM, May 2017(see more posts on U.S. Durable Goods Orders, ) Source: Zerohedge.com - Click to enlarge |

The Fed’s Williams has already spoken today (Sydney) and appeared to align with the Fed’s leadership, sticking with the need for gradual rate increases, and willing to look past the recent decline in core inflation measures. Tomorrow there is a flurry of Fed speakers, including Yellen, and the sole dissent at the last two hikes, Kashkari also speaks tomorrow. Later today, the ECB’s forum will hear from Draghi, Carney, and Kuroda.

Italy

It is important to recognize that this is not a case of Italy ignoring the new rules about the resolution of troubled banks. Italy exploited a loophole, and the EC approved. Italian officials argued that state aid was necessary to avoid economic disturbances in Veneto. The fact that the banks were not systemically significant also allowed greater flexibility.

The markets have initially responded favorably. Italy’s 10-year government bond yield is off three basis points today, which is the most in Europe outside of Greece, which was upgraded by Moody’s before the weekend. Despite the lack of debt relief from the official creditors, Greece is still exploring a return to the capital markets. That is essential if a fourth aid package when the current one ends in a year is to be avoided.

Italian equities have rallied, and the FTSE-Milan Index is up 1.4% to the lead the major bourses higher. The Dow Jones Stoxx 600 is up half as much, led by consumer staples and financials. The bank shares sub-index is up 1.3%, to snap a four-day drop. Italy’s All-Share Bank Index is up 3.3%, the most since Macron’s first round victory in the French presidential election in late April.

Separately, Berlusconi’s Forza Italia and the far-right parties did well in the second round of local elections. It won captured the governance of several cities including Genoa and Verona. The revival of Forza Italia is important. The PD and Five-Star Movement were both polling around 30%. This left Forza Italia and far-right parties, including the Northern League, dividing up another 30%. Mutual political interest rather than ideological goals pull the forces together.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,EUR/CHF,FX Daily,Germany Business Expectations,Germany Current Assessment,Germany IFO Business Climate Index,Italy,newslettersent,OIL,Spain Producer Price Index,U.S. Durable Goods Orders