Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Jonathan Watson

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitter

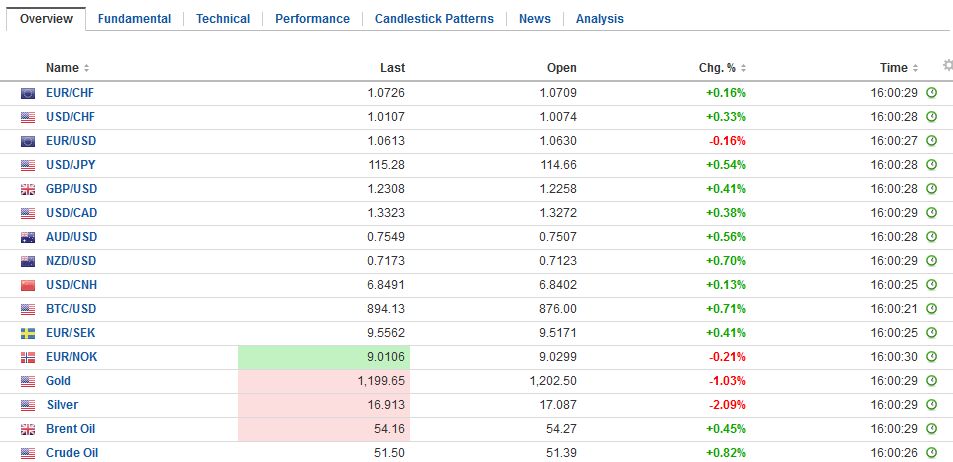

Swiss Franc |

EUR/CHF - Euro Swiss Franc, January 19(see more posts on EUR/CHF, ) - Click to enlarge |

GBP/CHFGBP/CHF has been range bound in recent weeks but anything but predictable! Of course one of the main, if not the main driver on this rollercoaster is the pound which has been much weaker and stronger according to the sentiments over the Brexit. On the whole the market is predicting the pound will be weaker in the future hence the big drops. So will GBP/CHF now gather pace and rise over 1.25 or could the next move be much lower below 1.20? There are various factors of late which we can signal as helping sterling, notably the PM Theresa May’s speech which indicated that the UK would aim for coming out of the single market and forging ahead a new relationship with the the EU. The prospect of the Supreme Court case favouring the previous claim and upholding the previous decision will also be beneficial to the UL and sterling. If you look to next Tuesday the 24th we have the Supreme Court case due which will give us the decision on this key component of GBP/CHF direction. Due at 09.30 am this announcement should be closely watched for news that could impact your rate. Looking further ahead we also have further news on triggering Article 50 and then as we get to the point of triggering apparently by the end of March the pound could be subject to further volatility. Finally we have the Franc which as a safe haven currency can strengthen in times of uncertainty globally. Depending on various events due this year the Franc might find it becomes a favourite once again and rates below 1.20 should in my opinion not be ruled out. |

GBP/CHF - British Pound Swiss Franc, January 19(see more posts on GBP/CHF, ) - Click to enlarge |

Federal ReserveWhile the US 10-year yield is unchanged, the dollar is consolidating its gains against the yen in a relatively narrow range of about half a big figure below JPY115.00. It has seen its gains pared more against the euro and sterling, where most of Yellen-inspired gains have been unwound. Sterling found support near $1.2250 and was bid up to $1.2335 by early in the European sessions. The euro recovered have a cent from $1.0620. |

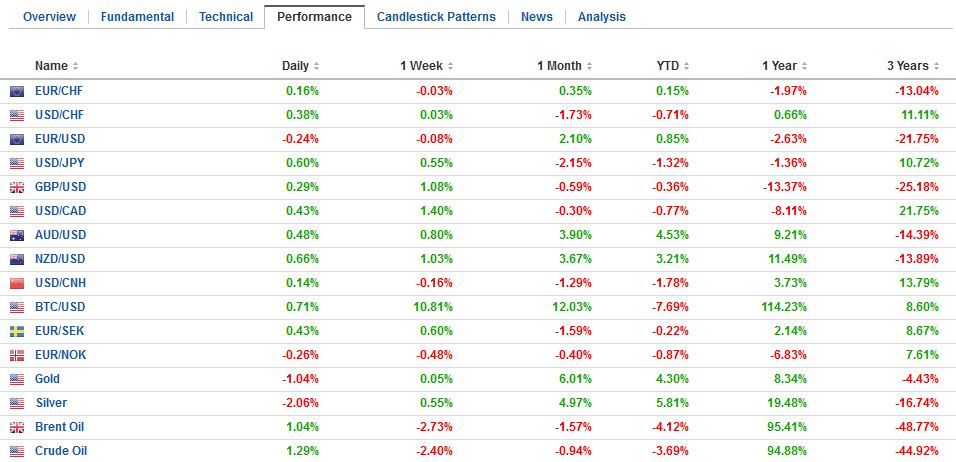

FX Performance, January 19 2017 Movers and Shakers Source: Dukascopy - Click to enlarge |

| The other talking point today is yesterday’s TIC data. The press is highlight the fact that China sold $66.4 bln of US Treasury bills, notes and bonds. It is the sixth consecutive draw down, and the largest since the end of 2011. The US Treasury reckons China still has $1.05 trillion of its paper. Japan reduced its Treasury holdings for the fourth consecutive month. The $22.3 bln liquidation brings the holdings to $1.11 trillion. China and Japan together account for the bulk of the reduced foreign holdings, which now stands at $5.94 trillion, the lowest since 2014. |

FX Daily Rates, January 19 - Click to enlarge |

| We would add two points to the discussion. First, there is often a lot of noise around bills. This may be especially true as the asset managers prepared for a Fed hike. The signal is the long-term flows. These rose $30.8 bln. The private sector is absorbing what official sales that are taking place. The pace is also fairly steady. The monthly average inflow in 2014 was almost $23 bln, and $26.5 bln in 2015. The average for the first eleven months of 2016 was $24.6 bln.

Second, we note that the Federal Reserve’s custody holdings for foreign central banks trended lower through the middle of November reaching about $3.111 trillion. It has risen by more than $70 bln. This data series is not directly comparable to the TIC data. The Fed’s custody data show practically no change from the end of October to the end of November. Our point is that the private sector appears to buying from official sales and that those official sales do not appear to worrisome, and may have actually increased more recently. |

FX Performance, January 19 - Click to enlarge |

EurozoneThe focus now shifts to the ECB. Of course, after adjusting policy last month, the ECB is highly unlikely to take new initiatives today. The most important new development since the December ECB meeting is the rise in inflation. Headline CPI stood at 1.1% at the end of last year, nearly double the 0.6% pace seen in November. We look for Draghi to push back. Like several other national central bank presidents, Draghi is likely to caution against exaggerating the increase in inflation, and see it as mostly reflecting the recovery in energy prices. The core rate is at 0.9% having bottomed at 0.6%. The ECB will have to wait until new staff forecasts are available in March to understand better if the trajectory of inflation has changed. Last month, Draghi acknowledged that deflation forces were almost vanquished. He can extend this analysis a little, but it may not yet be time to change the balance of the outlook quite yet. Still, there may be scope for another type of concession to the more hawkish contingent: the reference that rates will remain low or lower can be modified to suggest less risk of a lower rates. Draghi, like Yellen, will also likely recognize the high degree of uncertainty. In addition to the uncertainty around the policies and priorities of the new US Administration, Draghi also has to navigate through several elections, including Germany, France, and Netherlands. There is also some risk of elections in Greece and Italy too. |

Eurozone Consumer Price Index (CPI) YoY, December 2016(see more posts on Eurozone Consumer Price Index, ) Source: Investing.com - Click to enlarge |

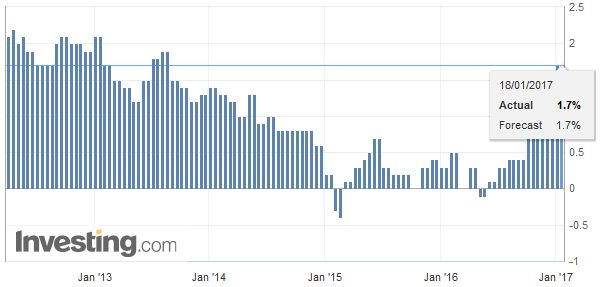

| The rise in German CPI to 1.7% can only increase the criticism of the German representatives of the ECB’s stance. |

Germany Consumer Price Index (CPI) YoY, December 2016(see more posts on Germany Consumer Price Index, ) Source: Investing.com - Click to enlarge |

United StatesUS data, including housing starts, permits, initial jobless claims, and January Philly Fed, will be overshadowed by the ECB press conference a quarter hour later. Yellen speaks late in the US, which will be early in the Asia’s Friday session but after yesterday’s comments, her views are a known quantity.

|

U.S. Housing Starts, December 2016(see more posts on U.S. Housing Starts, ) Source: Investing.com - Click to enlarge |

| Some observers saw in Yellen’s comments stronger confidence in the economy. Bloomberg’s calculation of the odds of a March hike increased to a little more than 34% from a little less than 30%. |

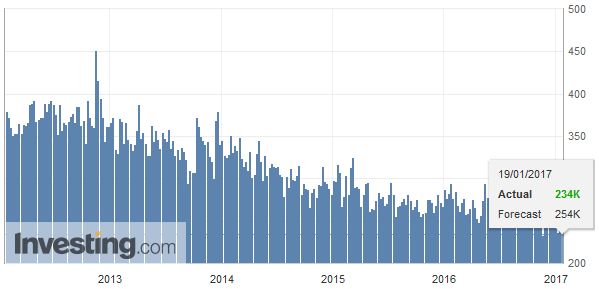

U.S. Initial Jobless Claims, December 2016(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

| The CME calculation was unchanged at a little below 20%. The March Fed funds futures contract slipped half a basis point yesterday (to 68.5 bp from 68 bp). It is now near 69.5 bp. |

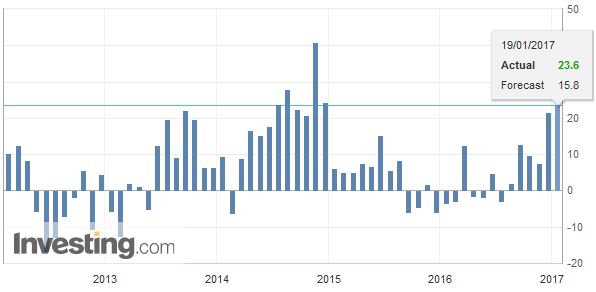

U.S. Philadelphia Fed Manufacturing Index, December 2016(see more posts on U.S. Philadelphia Fed Manufacturing Index, ) Source: Investing.com - Click to enlarge |

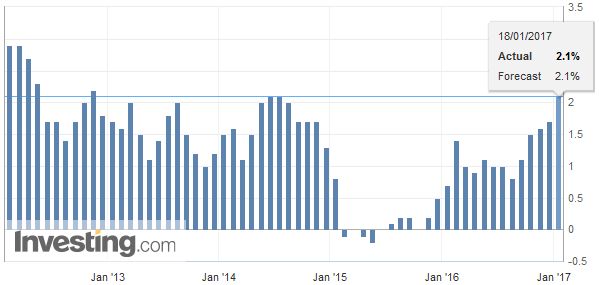

| Comments late yesterday by the Fed’s Yellen after headline CPI rose above 2% for the first time in a couple of years, and the largest rise in industrial output since November 2014, spurred a rise in US yields and the dollar. |

U.S. Consumer Price Index (CPI) YoY, December 2016(see more posts on U.S. Consumer Price Index, ) Source: Investing.com - Click to enlarge |

| The US 10-year note yield rose 10 bp to 2.43%. It was the biggest rise in a month. The dollar snapped a seven-day drop against the yen with an exclamation point–a 1.8% jump, its best in a two months. |

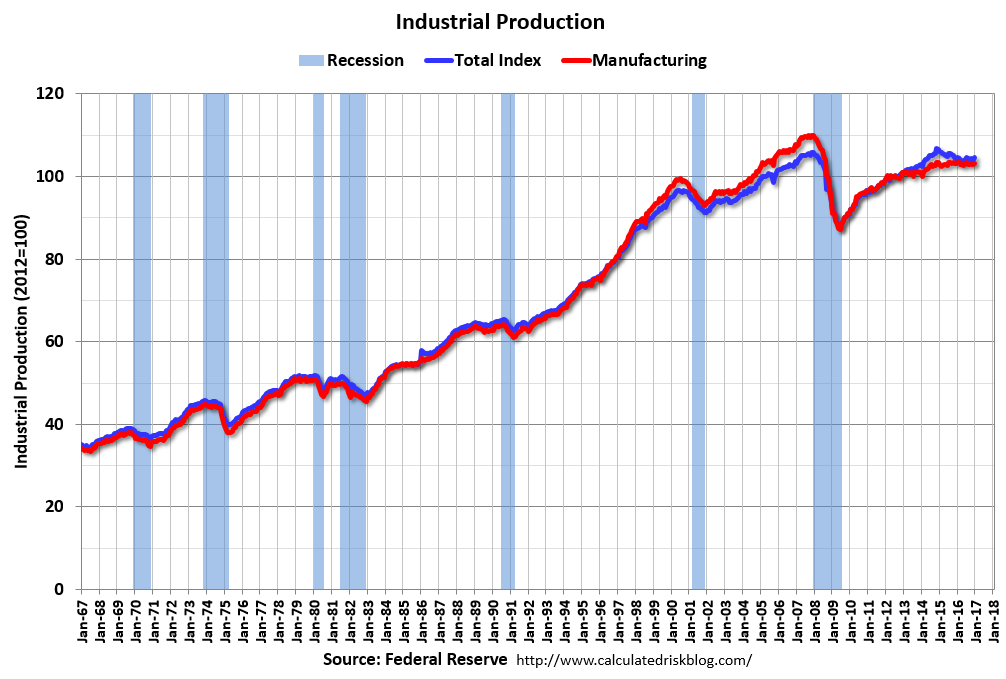

U.S. Industrial Production, December 2016(see more posts on U.S. Industrial Production, ) Source: macro.economicblogs.org - Click to enlarge |

Switzerland |

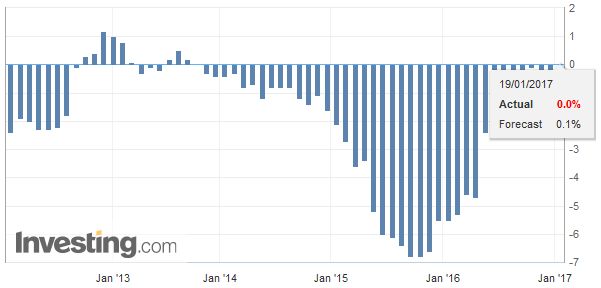

Switzerland Producer Price Index (PPI) YoY, December 2016(see more posts on Switzerland Producer Price Index, ) Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,EUR/CHF,Eurozone Consumer Price Index,FX Daily,gbp-chf,newslettersent,Switzerland Producer Price Index,U.S. Consumer Price Index,U.S. Housing Starts,U.S. Industrial Production,U.S. Initial Jobless Claims,U.S. Philadelphia Fed Manufacturing Index