Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, January 11(see more posts on EUR/CHF, ) - Click to enlarge |

|

The pound has seen a sharp fall following the interview that Theresa May gave with Sky news on Sunday although there has been a small rebound this afternoon. GBP CHF exchange rates are hovering around 1.2350 for this pair. The pound fell sharply in morning trade but has since recovered as there still remains a great deal of ambiguity as how Brexit will take form. In my view yesterday’s fall was something of an overreaction considering we are still awaiting the verdict from the Supreme Court. The markets now eagerly await that Supreme Court ruling which may arrive later this week or next. The news could even come as soon as tomorrow and this will almost certainly give new direction for sterling exchange rates. Those clients looking to buy Swiss Francs may see a window of opportunity to buy should UK Prime Minister Theresa May lose the appeal as to whether she must consult Parliament before invoking Article 50. Those clients looking to sell Swiss Francs may wish to take advantage of the exceptional levels which are currently available. These next few months are undoubtedly going to be the most volatile we will perhaps see with Brexit fast approaching as we near to March. Data is light for Switzerland today so eyes look to UK manufacturing and industrial production figures released tomorrow which are likely to impact on the pound. The National Institute for Economic and Social Research Gross Domestic Product (GDP) estimate for the UK is released tomorrow afternoon and is seen as an excellent precursor to the official GDP numbers. |

GBP/CHF - British Pound Swiss Franc, January 11(see more posts on GBP/CHF, ) - Click to enlarge |

FX RatesReports that a file from a former UK intelligence officer, which has circulated among policymakers and reporters for sometime, claim that Russia has material to try to blackmail Trump. Senior people close to the President-elect were said to be in contact with Russia during the campaign. Yet these political developments have been unable to derail the dollar, which is edging higher against most of the major currencies today. The focus is on US politics and the high degree of uncertainty. The lead story in the Financial Times is that Trump’s nominee for Attorney General “Sessions retreats from Trump’s election rhetoric on in Senate hearing.” In particular, the paper identifies three areas of divergence, Russia, Muslims, and torture. Today, Tillerson, the former Exxon CEO, and nominee for Secretary of State is also expected to take a firmer line on the risks from Russia. |

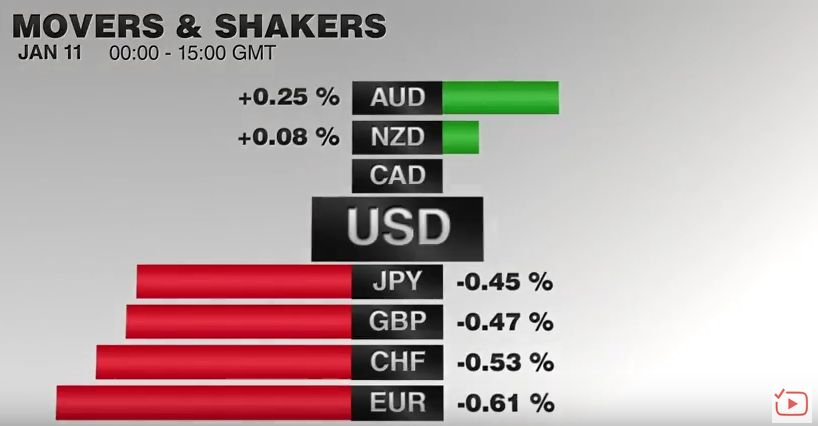

FX Performance, January 11 2017 Movers and Shakers Source: Dukascopy - Click to enlarge |

| Those hearings may be overshadowed to some extent today by Trump’s press conference, the first since July. The topic initially was going to be how he was arranging his extensive investments to avoid potential conflicts of interest, but the reports on Russia may be more immediate interest. And it is not like there is much US data to compete with these political developments. The MBA’s Mortgage Applications report is the only data on tap. The economic calendar picks up starting tomorrow with import prices and weekly initial jobless claims, followed by Friday’s PPI and retail sales.

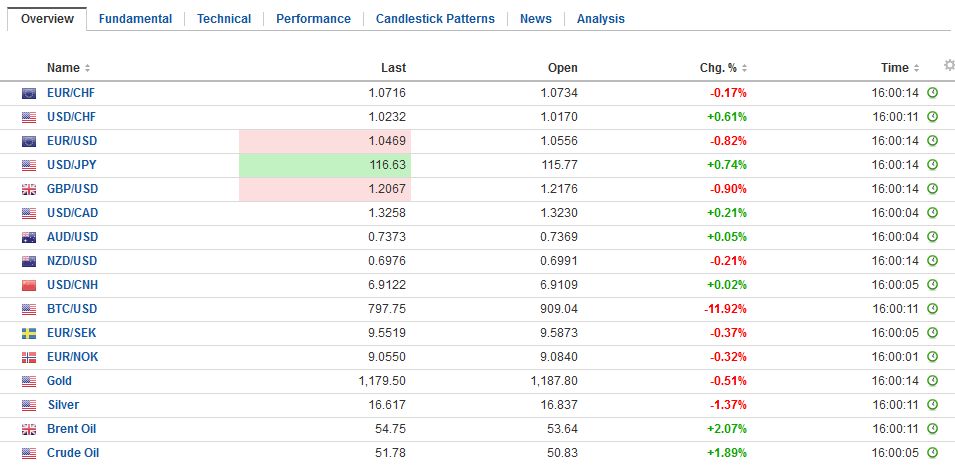

The euro poked above $1.0625 yesterday, its high for the year, but found keen sellers. As North American dealers return, the euro is back on the week’s lows a little above $1.0510. We have suggested a break of $1.080-$1.0500 would offer the first sign that the dollar’s correction that arguably began in mid-December is over. The dollar found support near JPY115.20 yesterday and has recovered to almost JPY116.50. There seems to be potential toward JPY117.50 the week’s high, but still a big figure off last week’s high near JPY118.60. |

FX Daily Rates, January 11 - Click to enlarge |

| Sterling has traded on both sides of yesterday’s range. As we noted earlier, the break of $1.22 earlier this week, for the first time since in more than two months, is important from a technical point of view. It now is acting as resistance and sterling was sold as this was approached in Asia. Sterling briefly dipped below $1.21 for the first time since October 25. A near-term low may be in place, and another test on $1.22 cannot be ruled out now.

The Australian and New Zealand dollars are among the best performers today and are extending this week’s advance. The Aussie is knocking on $0.7400, its best level since the Fed hike. A move above there would spur gains toward $0.7500. The Kiwi continues to trade in the same broad range it has been in since the second half of last week. The Canadian dollar is firm, and although, like the Aussie is near its best levels since mid-December, it is trading in a relatively narrow range for the last several sessions. |

FX Performance, January 11 - Click to enlarge |

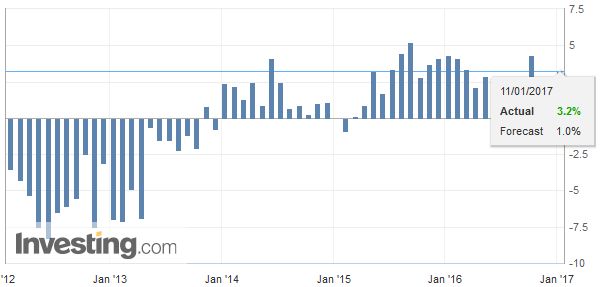

SpainIn fact, the economic calendar has been sparse today. The highlights are the continued reporting of national industrial output figures for November in Europe and the UK’s trade figures. The UK and Spain reported industrial production figures, and both followed the lead of France yesterday to report stronger than expected data. Spain’s industrial output jumped 1.8% in the month of November. The Bloomberg median forecast was for a 0.4% gain. The year-over-year seasonally adjusted pace is 3.2%, up from 0.6% in October (initially 0.5%). |

Spain Industrial Production YoY, December 2016(see more posts on Spain Industrial Production, ) Source: Investing.com - Click to enlarge |

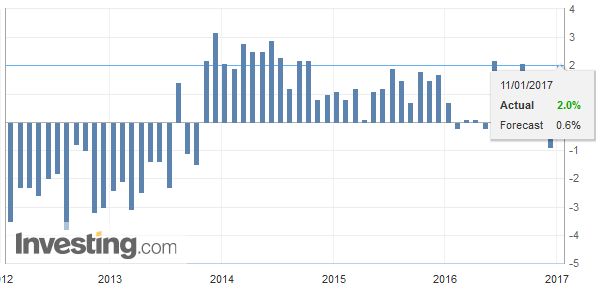

United KingdomThe UK’s industrial output rose 2.1% in November, and the October decline was shaved too -1.1% from -1.3%. This is the largest increase in seven months. The year-over-year pace stands at 2.0%. The Bloomberg median forecast was for a 0.7% pace. |

U.K. Industrial Production YoY, December 2016(see more posts on U.K. Industrial Production, ) Source: Investing.com - Click to enlarge |

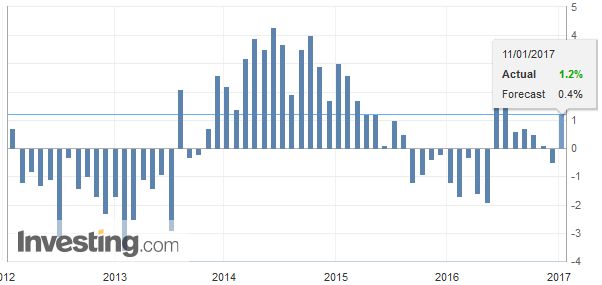

| Manufacturing drove the increase. It rose 1.3% on the month and 1.2% year-over-year. |

U.K. Manufacturing Production YoY, December 2016(see more posts on U.K. Manufacturing Production, ) Source: Investing.com - Click to enlarge |

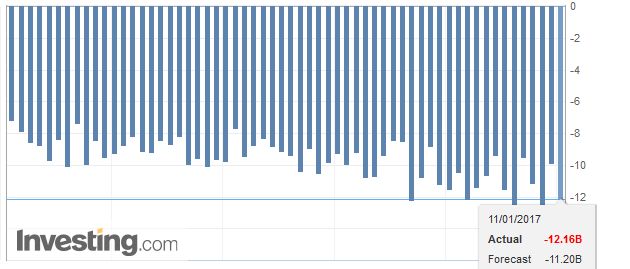

| On the other hand, the UK trade balance deteriorated more than expected. The overall trade balance (goods and services) rose to GBP4.167 bln, which is more than 10% larger than anticipated. The October shortfall was revised to GBP1.547 bln from GBP1.971 bln. The deterioration can be accounted for by merchandise trade. That trade deficit widened to GBP12.16 bln from a revised GBP9.885 bln (from GBP9.711 bln). Total imports jumped 8.4%. Imports of transport equipment (e.g., ships and aircraft) rose and the increase (GBP1.4 bln) accounts for around half of the trade deterioration. Exports rose 2.8%. |

U.K. Trade Balance, December 2016(see more posts on U.K. Trade Balance, ) Source: Investing.com - Click to enlarge |

Higher commodity prices are helping lift equity markets today. Oil is firming after approaching one-month lows, partly in anticipation of a 1.5 mln barrel build in US oil stockpiles. Iron ore prices rose 3% in China after a 5.5% gain on Tuesday. The MSCI Asia Pacific Index rose 0.2%. It has been up every day this week and has advanced five of the past six sessions and nine of the past 11. Korea and India markets led with gains of near 1.5% and 1.0% gains respectively. The Hang Seng’s 0.8% advance is notable because it is the fifth successive gain and the ninth gain in 10 sessions.

European markets are narrowly mixed. Germany, France, and the UK equities are edging higher, while Spain and Italy are slightly heavy. Telecoms and materials are leading the small gain in the Dow Jones Stoxx 600. It is the opposite in the bond markets. Core bonds heavy and peripheral bonds are firmer. The US 10-year Treasury is just below 2.40%.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,FX Daily,gbp-chf,newslettersent,Spain Industrial Production,U.K.,U.K. Industrial Production,U.K. Manufacturing Production,U.K. Trade Balance