Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Forces emanating from the US and Europe are driving the capital markets.

The moves may be stretched technically, but the market adjustment has further to run as not even two Fed hikes are discounted for next year.

European political concerns and an ECB expected to continue its asset purchases have driven German 2-year yields to new record lows.

There are powerful moves underway in the capital markets. Some are new, and others have accelerated in recent weeks. The moves have stretched technical readings, but key drivers not only remain intact but may strengthen over the next week.

We argue that there are two main forces driving the shifting portfolio allocations.The first emanates from the US and the second from Europe.

There is growing confidence that the Federal Reserve will hike rates next month, and more next year. Nevertheless, the market does not have two Fed hikes priced in for next year, suggest there is scope for additional adjustment. Two hikes next year will likely be the base case for many forecasts. The dramatic rise in long-term Treasury yields is the direct consequence anticipation of fiscal stimulus when the economy is already growing toward trend. Both US presidential candidates’ programs call for fiscal stimulus. Trump’s was larger and included significant tax cuts as well.

While many of the comparisons between Trump and Reagan are superficial and faddish, one kernel of truth may be found in the policy mix. An expanding fiscal policy and a monetary policy that was becoming less accommodative characterized Reagan’s first term and coincided with the first dollar rally post-Bretton Woods. Of course, Trump as not assumed office yet, and he will have to negotiate with a more austere Republican leadership in Congress. A deft negotiator may secure Democrat support for spending increases and Republican support for tax cuts.

However, the economy that Trump will inherit is significantly different from what Reagan received. Presently, the US economy is growing near-trend, and unemployment has slipped below 5%. Many investors suspect that may prove to be inflationary. Four months ago the yield was just above 1.30%. It finished last month a little above 1.80% and closed last week near 2.35%. Ironically, despite the continued expansion of the US economy and rising price pressures, the 10-year bond yield is still below last year’s high seen in July near 2.50%.

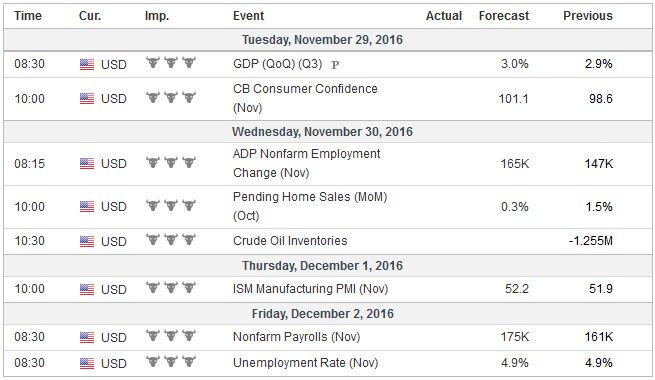

United StatesLong-term interest rates remain lower than what used to be associated with the current economic conditions and price pressures. The US 10-year yield peaked near 16% in Q3 1981. One does not have to assume that secular downtrend in interest rates is over. There have been other significant counter-trend moves. However, the trend could be over as deflationary forces have been arrested and global growth appear to be stabilizing. This week’s data is unlikely to alter views but may strengthen the appreciation of the solid economic performance since struggling in Q4 15 through Q2 16. Growth in Q3 is expected to be tweaked up to 3.0% in this week’s revision. The US economic data continues to be mostly reported stronger than expected. The NY Fed estimates that US economy is tracking 2.5% growth here in Q4, while as of the middle of last week, the Atlanta’s Fed model was more optimistic; tracking 3.6%. At the same time, investors will be reminded of the proximity of the Fed’s objectives. The core PCE deflator is expected to have remained steady in October at 1.7%. The Fed’s target is 2%. At the end of the week, the US reports the November jobs data. It is expected to show solid, even if not spectacular job growth of 175k-185k. The unemployment rate is expected to be unchanged at 4.9%, and hourly earnings are forecast to be steady at the 2.8% year-over-year, the highest rate in seven years reached in October. The bond market and the dollar, given the recent tight link, may be particularly sensitive to downside surprise in the unemployment rate or an upside surprise in earnings. Many are concerned about the protectionist signals sent by candidate Trump. The widening of the trade deficit the coming months as a result of growth differentials may make for fertile ground for the rhetoric to be operationalized. The implication of less commitment to free-trade while the US is a net international debtor (the world owns more US assets than American own foreign assets) is not clear. Those issues seem to be a medium term challenge, and by the time they are salient the world could look a lot different. |

Economic Events: United States, Week November 28 . - Click to enlarge |

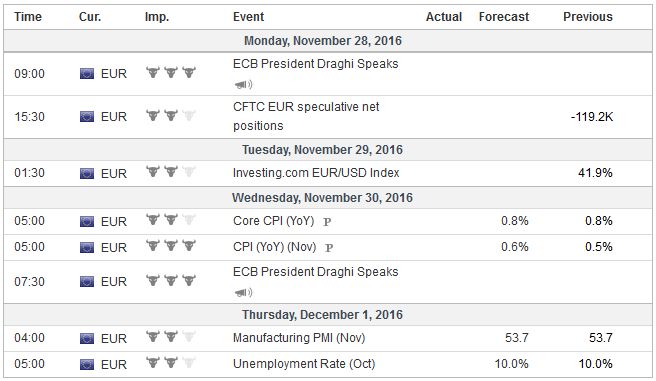

EurozoneThat brings us to the second driver of the shift in the investment climate: Europe. It is not the European economy per se. Eurozone growth is near trend, and the flash November PMIs raise the hope of some modest improvement. However, unemployment has been slow to improve. After finishing last year at 10.5%, it has been stuck at 10.0% since July. Money supply growth has stabilized near 5% since the middle of last and lending is slow. Both will be on exhibit to start the week. Those at the ECB who want to extend the asset purchases anchor their arguments in the weak price pressures. The preliminary CPI will be the last look at inflation before the ECB meets on December 8. The headline rate may tick up slightly to 0.6% from 0.5% in October. It would be a two-year high, but the increase since the 0.1% rise in July is largely a function of oil prices, as the core rate has been steady at 0.8% in recent months and is expected to remain there in November. The Austrian election is a do-over after the May election results were voided by the courts for the improper handling of postal votes. The populist-nationalist Hofer is polling a little ahead of the Green’s von der Bellen. A victory would make Hofer the first far-right head of state in Europe since WWII. The post may be largely ceremonial, but the symbolic victory may be underestimated by the focus on the Italian referendum. Expectations that the referendum will not be approved are widespread. The key unknown is what follows. Although Renzi has threatened to resign if the referendum fails, his signals have been ambiguous. If he resigns, the idea is that the PD would select a caretaker, perhaps a current minister, that would attempt to complete the political reforms and hold the parliamentary election as scheduled in 2018. However, Renzi could force an early election. It is a scenario he played down but came back to the fore last week. The most important point is that investors’ anxiety over the possibility that 5-Star Movement is swept is getting ahead of events. However, a weak government or a caretaker government means that the reform efforts slow. Italian assets have underperformed recently as the referendum drew near. The Italian 10-year premium to Germany widen nearly 50 bp over the past month, and at 1.85%, is the largest in more two and a half years. The rising sovereign yield (Italy’s 10-year yield has risen 63 bp over the past month, the most in Europe) is one of the factors that have weighed on bank shares. The Italian bank share index is back to its lowest level since early October. |

Economic Events: Eurozone, Week November 28 . - Click to enlarge |

GermanyThe prospect that the ECB could alter is self-imposed rules about its asset purchases, which would allow it to buy more German bunds helped drive the German two-year yield to new record lows last week. The yield fell tominus76 bp ahead of the weekend before closing near 74 bp. Although most of the media coverage has focused on the rise in US yields, last week, the German rate move was larger Its two-year yield fell almost eight bp, while the US two-year yield rose less than five bp. Another consideration that may have contributed to the pressure on German yields is the rising political anxiety. At the end of next week, Austria elects a new president, and Italy holds a referendum on constitutional changes to the Senate, after earlier reforms for the Chamber of Deputies was approved. |

Economic Events: Germany, Week November 28 . - Click to enlarge |

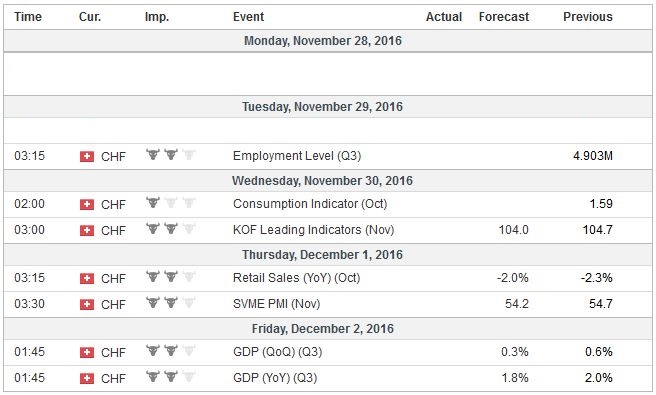

Switzerland |

Economic Events: Switzerland, Week November 28 . - Click to enlarge |

Looking further down field but already shaping scenarios for next year, the French presidential election. The prospect of a populist-nationalist victory is a source of anxiety. Investors are demanding a higher premium to hold French paper instead of German. On two-year money, the French premium has risen from 3-4 bp before the US election to 16 bp before the weekend, the largest since mid-2014. The 10-year differential widened from 31 bp to 55 bp, the most in a couple of years.

Meanwhile, EU tensions with Turkey have escalated following last week’s European Parliament non-binding resolution to end accession talks over Erdogan’s repressive response to the coup attempt. In response, Erdogan threatened to abandon the agreement to limit the immigration into Greece. The decision on talks resides the foreign ministers, not the European Parliament, and they are reluctant to break off accession talks. Should Erdogan re-open the borders, it would likely strength the appeal of the populist-right forces.

Elsewhere, OPEC is a wildcard next week. Since the summer, the ebb and flow of speculation about OPEC’s ability to reestablish some order to the oil market drove prices between roughly $42 and $52 a barrel (basis the front-month futures contract). The central problem is that Saudi Arabia cannot abide by sacrificing market share to other OPEC members, especially Iran, and Iran for its part cannot accept a freeze of output until it fully recovers from the embargo. That issue does not appear resolved, and that appears to be the reason Saudi Arabia pulled out of the meeting with Russia that was to be held on Monday (November 28). Meeting with Russia without a full agreement from OPEC members to cut output puts the cartel at a disadvantageous negotiating position. Separately, the restoration of Libyan output and the expansion of Kazakhstan’s production warns that it will be difficult to reduce supply.

More broadly, the CRB Index rallied 5.2% since November 14, but the momentum was sapped by energy and the grains. The price of gold has fallen about 10% in its three-week drop that has left prices at nine-month lows. Industrial metals have been the strongest part of the commodity complex, ostensibly on stronger US growth and a Chinese economy that is stabilizing.

Amid the portfolio adjustments, emerging markets have fallen out of favor, particularly bonds.The sharp rise in US Treasury yields forces many emerging market rates higher too. Rising rates and a stronger dollar lifts the cost for emerging market economies to borrow funds and to service their dollar-denominated debt. The MSCI Emerging Market equity index snapped a four-week, 7.5% decline last week. The 1.3% rise was broad-based. In contrast, major US indices, including the Russell 3000, are at record highs. Europe’s Dow Jones Stoxx 600 has rallied for three consecutive weeks for about 4%. It muted performance leaves it straddling the 100-day average, which is nearly 17.5% below the record high set in the middle of last year. Japan’s Topix has moved higher for eleven straight sessions coming into this week. It has advanced for three consecutive weeks (~8.5%) and in six of the past eight weeks.

Full story here Are you the author?

Tags: #USD,$EUR,France,Italy,newslettersent,SPY,US