Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

EUR/CHF - Euro Swiss Franc, November 07(see more posts on EUR/CHF, ) . - Click to enlarge |

FX RatesThe DAX also gapped lower before the weekend and gapped higher today. It is stalling just ahead of the earlier gap from last week (10460-10508). It is up about 1.6% in late-morning turnover. The strongest sector is the financials, up 2.5%, with the banks up 3.4%. Deutsche Bank is snapping a five-session drop. It fell 9.1% last week. It has recouped more than half of that today. More broadly, the Dow Jones Stoxx 600, which had not posted an advancing session since October 20 is up 1.2% today. Financials are up twice the overall market, followed by materials and energy. The S&P 500 is similarly poised to snap its longest decline since 1980. It may gap open (last Friday’s high was 2099). Since the middle of March, the S&P 500 not spent an entire session below its 200-day moving average and it has only closed below it once. It was approached before the weekend, and it held. |

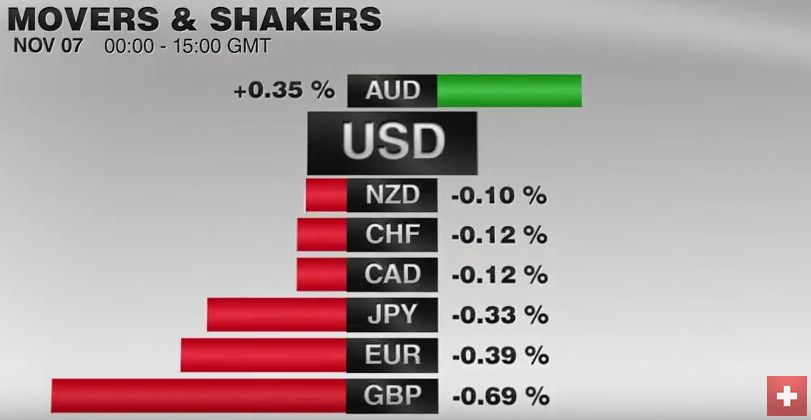

FX Performance, November 07 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| Emerging market equities are up almost 1%. The MSCI Emerging Market equity index has advanced on Monday’s in each of the past two weeks but proceeded to fall in the following four sessions. Support near 880 frayed and a move now above 890 creates scope for another 1% advance.

Core bond yields are firmer, with the 10-year UK Gilt leading the way with a 5 bp increase. The 10-year US Treasury yield is up four basis points to resurfaces above 1.80%. The Bund yield is up 1.5 bp. Italian, Spanish, Portuguese and Greek yields are 3-17 bp lower, respectively. |

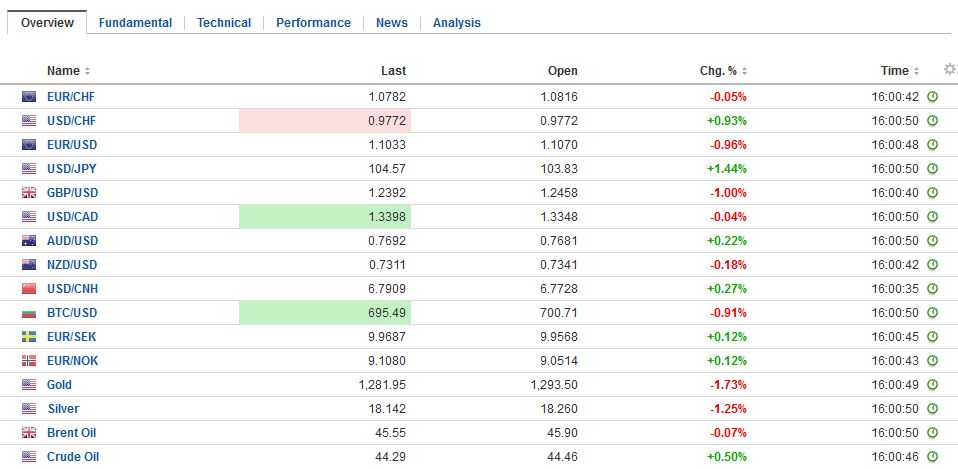

FX Daily Rates, November 07 (GMT 16:00) . - Click to enlarge |

| The euro rallied from $1.0850 on October 25 to $1.1145 before the weekend. The 38.2% retracement is seen near $1.1035. Today’s low thus far is about $1.1045. Look for sellers to come back in on a bounce toward $1.11. The dollar already recouped more than 61.8% of last week’s slide against the yen. That was found near JPY103.40. The intraday technicals warn of near-term consolidation.

Sterling look set to end its six-day advance. The better dollar tone and Labour’s threat to block the triggering of Article 50 unless access to the single market is assured is taking a toll. Sterling’s pullback has met a 38.2% retracement of the rally (~$1.3390). The 50% retracement is at $1.2335. The intraday technicals suggest this is unlikely to be seen before a recovery back toward $1.2450. |

FX Performance, November 07 . - Click to enlarge |

EurozoneDomestic orders fell 1.1%, while export orders slipped 0.3%. Orders from the eurozone fell 4.5% after rising 4.2% in August. Orders from outside EMU rose 2.5%. |

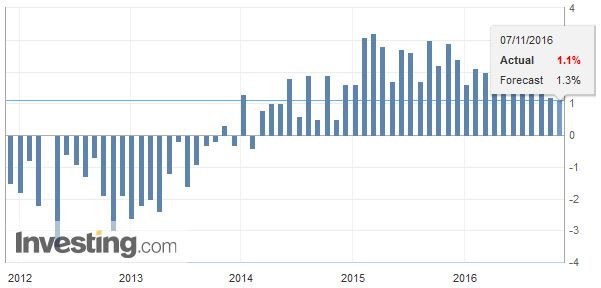

Eurozone Retail Sales YoY October 2016(see more posts on Eurozone Retail Sales, ) . Source: Investing.com - Click to enlarge |

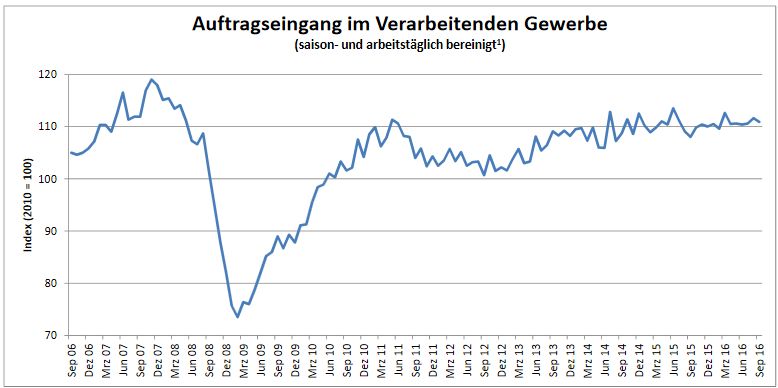

GermanyOutside of the US political developments, two economic reports standout. First, September factory orders from German disappointed, but the impact is blunted by the more recent October PMI recovery. Orders slipped 0.6% in September. The median forecast in the Bloomberg survey was for a 0.2% increase. August’s 1.0% gain was shaved to 0.9%. The year-over-year rate rose to 2.6% from a revised 2.0%. |

Germany Factory Order September 2016 . - Click to enlarge |

Spain |

Spain Industrial Production YoY October 2016(see more posts on Spain Industrial Production, ) . Source: Investing.com - Click to enlarge |

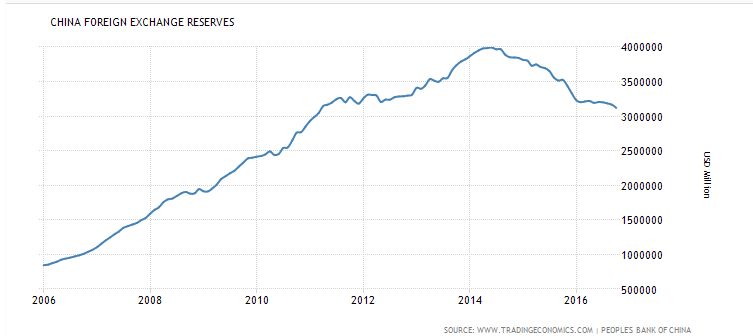

ChinaThe other economic report that is important to investors is China’s reserve data for last month. Reserves fell by $45.7 bln, the most since January, and about a quarter more than expected. Valuation shifts played a role. The other reserve currency assets fell (sterling -5.6%, euro -2.2%, yen -3.3%) and bond sold off, with 10-year Treasuries rising 10 bp, and Gilt yields up 21 bp, Bunds, and Oats up almost 15 bp. |

China FX Reserves 10 Years . - Click to enlarge |

| However, valuation does not explain it fully, and capital outflows appear to have increased. The yuan fell by 1.5% against the dollar in October. It fell about the same amount in May, when reserves fell $9 bln, and last December when reserves fell by $108 bln. In August 2015, when the yuan fell 2.7%, Chinese reserves fell by $43. This speaks to the lack of relationship between the size of the yuan’s fall and the amount of reserve pressure. |

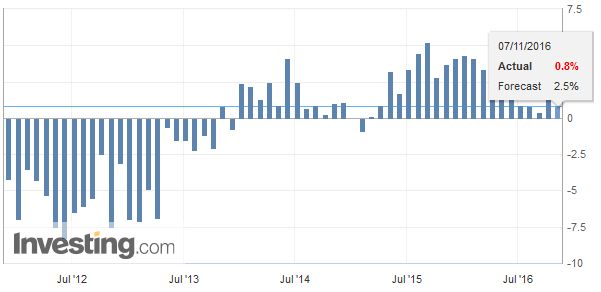

China Trade Balance, Otober 2016(see more posts on China Trade Balance, ) . Source: Investing.com - Click to enlarge |

| It may reflect the of lack of full transparency regarding intervention in the derivatives market. It also suggests that the currency remains highly managed. There had been much talk about officials propping up the yuan ahead of the October 1 formal inclusion into the SDR basket. Some see it stepping away during the national holidays in the first week of October, and others linked it to the seventh consecutive monthly decline in exports. |

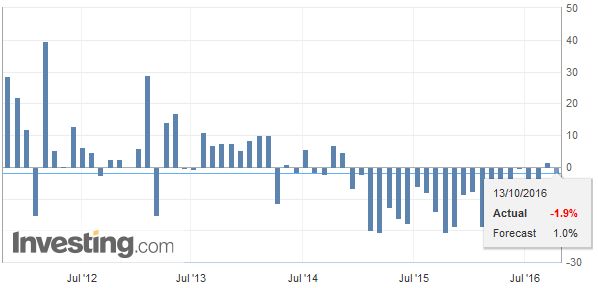

China Imports YoY, October 2016(see more posts on China Imports, ) . Source: Investing.com - Click to enlarge |

| China also reported its reserves in terms of SDRs. By this metric, Chinese reserves increased to SDR2.271 trillion from a SDR2.68 trillion. |

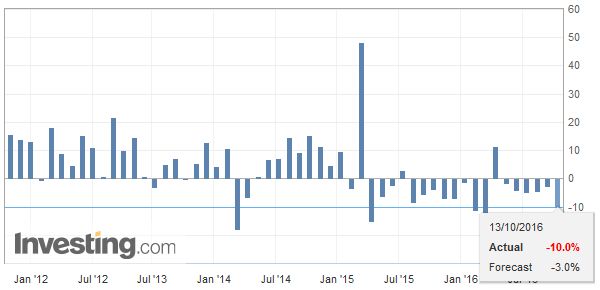

China Exports YoY, October 2016(see more posts on China Exports, ) . Source: Investing.com - Click to enlarge |

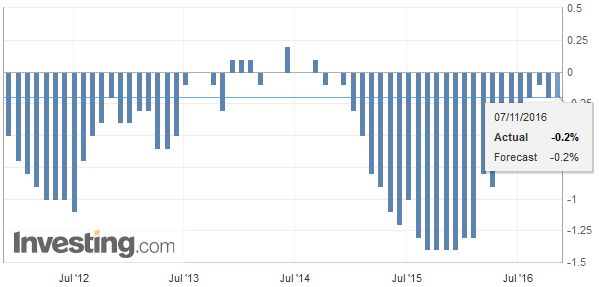

Switzerland |

Switzerland Consumer Price Index (CPI) YoY, October 2016(see more posts on Switzerland Consumer Price Index, ) . Source: Investing.com - Click to enlarge |

News that the FBI was once again ending its investigation into Clinton’s emails and use of private servers spurred sharp dollar against the major European currencies and yen. The dollar-bloc currencies fared better, while expectations of a rate cut late this week, weighed on the New Zealand dollar. Emerging market currencies, led by the Mexican peso, are mostly doing better.

Risk assets are doing better generally. Oil is recovering from last week’s outsized slide, despite the stronger dollar, as the Algerian Minister said OPEC would agree on output cuts next month, and a 5.3 magnitude earthquake struck within a couple of miles of Cushing, Oklahoma.

The MSCI Asia-Pacific Index broke the three-day down move to rise 0.4%. The Nikkei gapped lower last Friday and gapped higher today, leaving a bullish island-bottom in its wake. The Nikkei closed on its highs. Technically, it looks poised to re-challenge the seven-month highs seen last week near 17500.

Lastly, a word about the Mexican peso. It recorded a key reversal last Thursday, and there follow through buying on Friday. It had been embraced by many as a proxy for Trump, and its strength in the second half of last week (and the steady Fed funds futures) suggested some were looking past the latest tracking polls. The peso was marked sharply higher earlier today in Asia. The dollar hit a high a little below MXN19.55 last week and closed before the weekend at 19.02. It fell to almost MXN18.55 today. We continue to monitor a trendline drawn off the April lows that comes in near MXN18.50. The near-term risk now is on the upside for the dollar, with potential back toward MXN18.90.

Full story here Are you the author?

Tags: #GBP,#USD,$EUR,$JPY,China Exports,China Imports,China Trade Balance,Deutsche Bank,EUR/CHF,Eurozone Retail Sales,FX Daily,FX reserves,Germany Factory Orders,MXN,newslettersent,Spain Industrial Production,Switzerland Consumer Price Index