Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan My articles My siteAbout meMy videosMy books Follow on:LinkedINTwitterSeeking Alpha CFA SocietyEconomicBlogs EUR/CHFSwiss Franc: The EUR/CHF has fallen again to the SNB intervention levels of 1.08. The dollar has depreciated by more than 1%. Who has followed our blog, knows that the Franc is a proxy for global growth, in particular Emerging Markets. Today’s data from China let also the Aussie dollar, the Kiwi and the Euro rise.

|

EUR/CHF - Euro Swiss Franc, November 01 2016(see more posts on EUR/CHF, ) . - Click to enlarge |

|

GBP/CHFThe pound has fallen sharply again today after what appeared to be a good start to the week. GBP/CHF has fallen by almost 1.5% today and the pound has fared badly against all of the major currencies. Manufacturing data from the Purchasing Managers Index was robust and the sector has been supported by the recent weakness in the pound. This however was not enough to calm those Brexit concerns as shown by a big drop in the price of the pound. The Bank of England meeting is this Thursday and whilst no change in inters rates is expected there is a chance there may be some additional Quantitative Easing. I think this is unlikely though as the Bank has been blessed with a weaker pound which is helpful for British exports. Any further weakening in the price of sterling however would be counterproductive as it leads to inflationary pressures, something that has been well publicised of late with the recent “marmite gate” attempted price hikes. I would like to point out to my readers that Marmite is in fact made in the UK so quite why a 15% increase in prices is justified by Unilever is of concern. For this reason my view is that Mark Carney needs to start talking up the British economy rather than down. He can do this now as the economic indicators some four months on from the Brexit vote have been steady. If anything I see a boost for the pound this Thursday. |

GBP/CHF - British Pound Swiss Franc, November 01(see more posts on GBP/CHF, ) . - Click to enlarge |

Continued by Marc Chandler

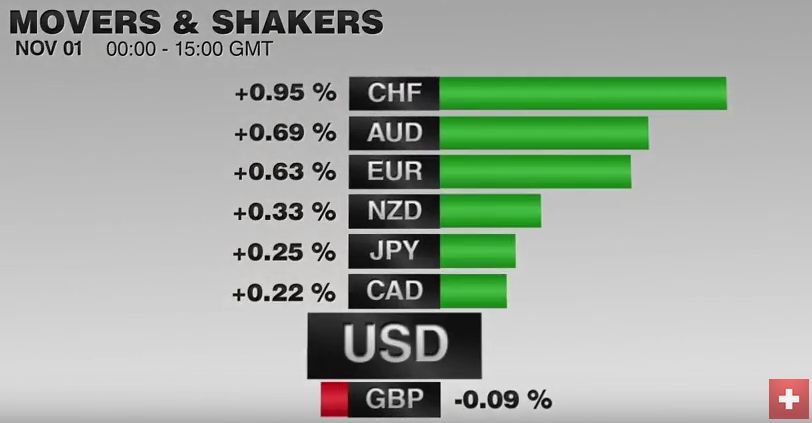

FX RatesThe US dollar is posting minor losses against most of the major currencies today. The Japanese yen is the exception, as the greenback continues to straddle JPY105. There have been several developments today, and the US also has a full economic calendar today. The most important of the developments was the upbeat message from the Reserve Bank of Australia. The Australia dollar is easily the strongest currency on the day, rising 0.7% against the greenback. It is poised for another run the $0.7700 area that has blocked the upside for the past several months. Australia’s AAA 10-year sovereign bond yield rose three bp to 2.80%. The two-year yield rose the same among to 1.675%. |

FX Performance, November 01 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| Sterling had already seen yesterday’s bounce on Carney’s one-year extension and the weaker US dollar tone. It reached $1.2280 in early in the European session and a low in North America yesterday near $1.2140. The 20-day moving average is found a little above today’s high. Sterling has not closed above this moving average in over a month. Above there, the high from the second half of October (~$1.2330) comes into view. |

FX Daily Rates, November 01 (GMT 16:00) . - Click to enlarge |

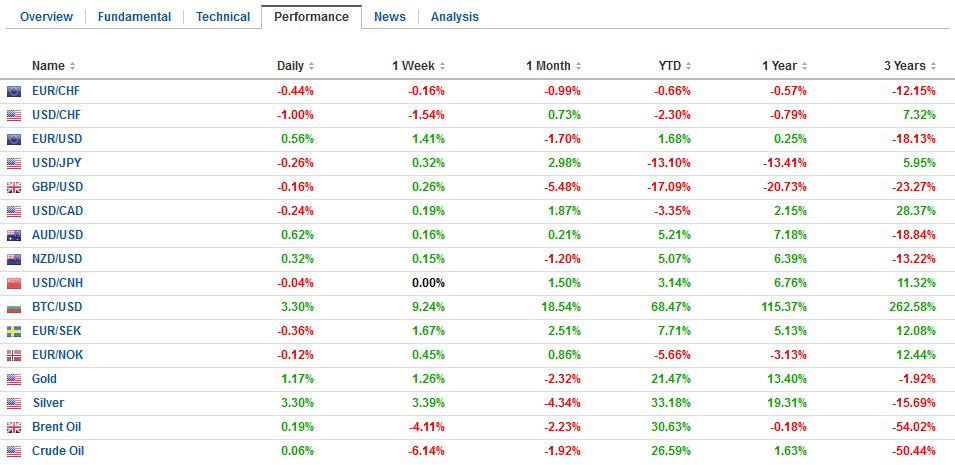

| The euro is also flirting with its 20-day moving average ($1.1005). Above there, the $1.1030-$1.1040 area beckons. That area houses a retracement and previous congestion. Support now is seen in the $1.0960-$1.0980 area. Its fortunes for the remainder of today’s session will likely be determined by new from the US. |

FX Performance, November 01 . - Click to enlarge |

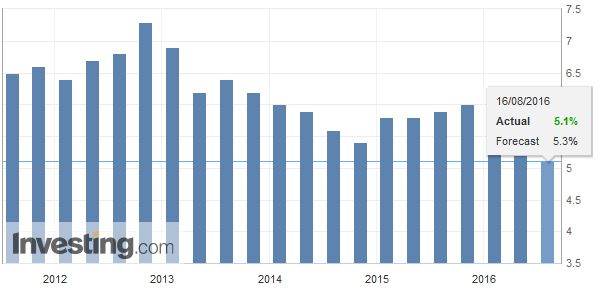

Australia and New ZealandThe RBA said as it kept the cash rate at a record low 1.5%, that current rates were sufficient to sustain the expansion. There was also the now regular concern over property prices. The RBA statement also acknowledged that currency appreciation could complicate the situation. The important takeaway is that the RBA appears to have shifted to a neutral bias and a rate. The market has reduced the odds of a rate cut next year to around one-in-three. Separately, Australia’s Oct manufacturing PMI rose to 50.9 from 49.8. The PMI is recovering from the sharp fall in August (to 46.9 from 56.4), and is back above the 50 boom/bust level for the first time since then. |

New Zealand Unemployment Rate, May - September 2016 . Source: Investing.com - Click to enlarge |

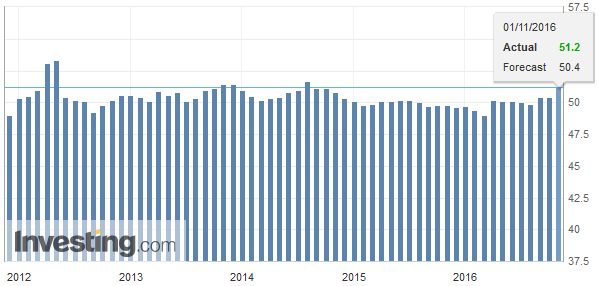

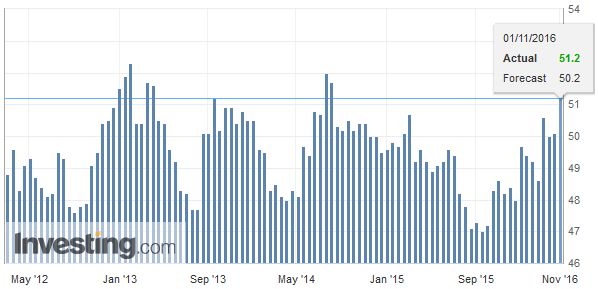

ChinaChina’s PMI also surprised on the upside. The official manufacturing reading rose to 51.2 from 50.4. This is a two-year high, well above the 50.3 median forecast in the Bloomberg survey, and the third month above 50. |

China Manufacturing PMI, October 2016(see more posts on China Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

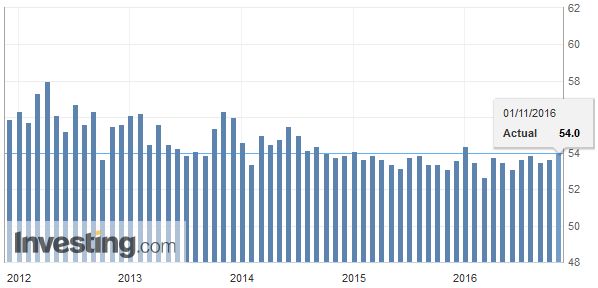

| The non-manufacturing PMI rose to a new high for the year. It stands at 54.0 from 53.7. |

China Non-Manufacturing PMI, October 2016(see more posts on China Non-Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

| Caixin’s manufacturing PMI rose to 51.2 from 50.1. This is also a two-year high. It gives further support to our contention that Chinese policymakers have the will and wherewithal ensure a soft economic landing. |

China Caixin Manufacturing PMI, October 2016(see more posts on China Caixin Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

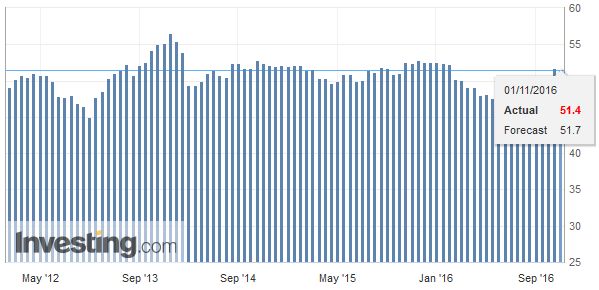

JapanAs widely expected the Bank of Japan left policy on hold (7-2 vote). As had been tipped, the BOJ pushed out when it is anticipating reaching its inflation target to around FY18 from somewhere in FY17. The BOJ’s message was still downbeat, recognizing the risks to growth and inflation were on the downside, and that recent price developments were of concern. The BOJ has not closed the door to additional measures. Separately, its manufacturing PMI was trimmed to 51.4 from the 51.7 flash, and 50.4 in September. It is the highest since January. |

Japan Manufacturing PMI, October 2016(see more posts on Japan Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

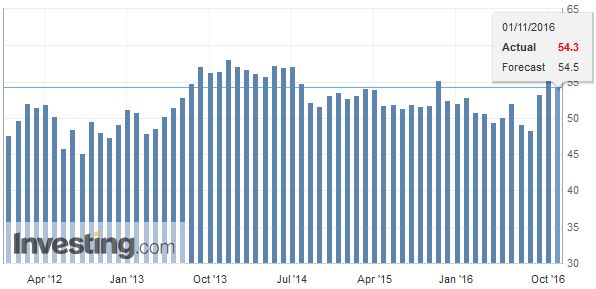

United KingdomAustralia, China, and Japan PMIS suggest Q4 is off to a good start. The UK broke the streak. Its October manufacturing PMI slipped to 54.3 from a revised 55.5 (from 55.4) in September. This was a little more than most had anticipated. Recall that the PMI had slumped to 48.2 in July (from 52.3 in June) after referendum shock. It subsequently rebounded sharply to two-year highs in September. It remains above 12 and 24-month averages (51.9 and 52.3 respectively). |

U.K. Manufacturing PMI, October 2016(see more posts on U.K. Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

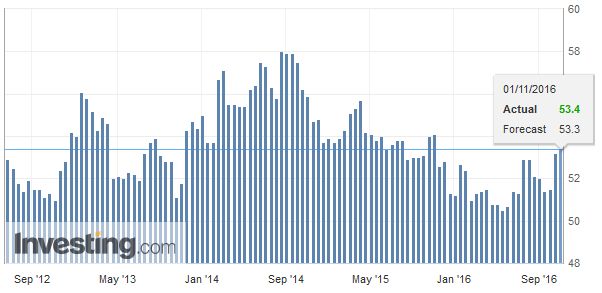

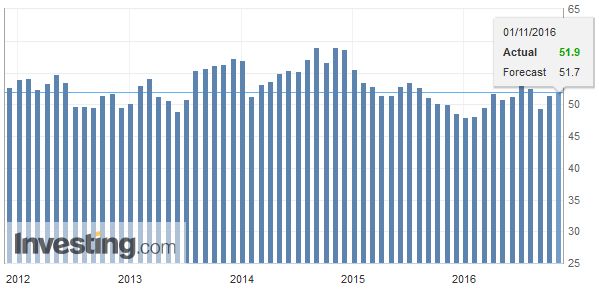

United StatesThe US news is expected to be upbeat. The Markit is expected to confirm the preliminary estimate at 53.2, the highest since July 2015. The ISM estimate is expected to continue to recover from the 49.4 hit in August. It stood at 51.5 in September. October auto sales will also be reported. Sales are expected to nearly match the September’s 17.65 mln unit pace, though foreign brands are expected to have picked up market share. |

U.S. Manufacturing PMI, October 2016(see more posts on U.S. Markit Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

| Canada reports August GDP. The median forecast is for a 0.2% rise after 0.5% jump in July, as the economy recovered from the wildfires’ impact. The year-over-year pace may be stable at 1.3%. A disappointing report would likely weigh on the Canadian dollar, as the greenback continues to hover around CAD1.34.

Although the API inventory estimate is reported after the markets close, commodity prices are radar screens. Copper and nickel prices are extending gains for a seventh session. Copper, nickel, aluminum, and zinc are extending their rallies. Gold is near a one-month high. On the other hand, oil prices are near one-month lows and consolidating yesterday’s large drop. Technically, there looks to be scope for another dollar drop in the December light sweet crude oil contract. |

U.S. ISM Manufacturing PMI, October 2016(see more posts on U.S. ISM Manufacturing PMI, ) . Source: Investing.com - Click to enlarge |

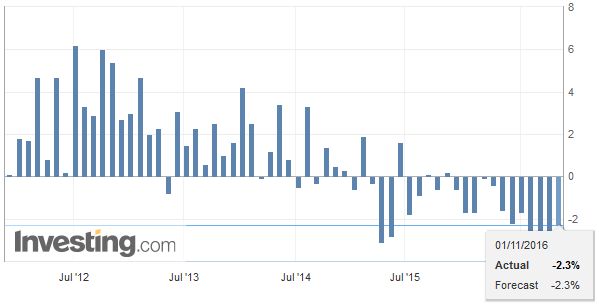

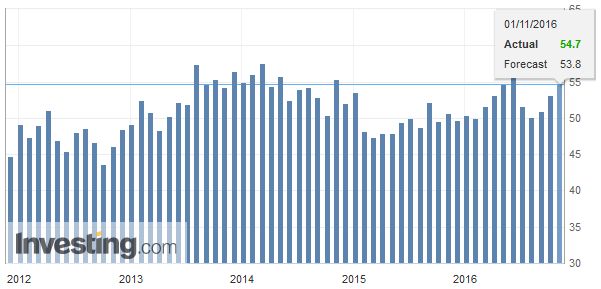

Switzerland |

Switzerland Retail Sales YoY, September 2016(see more posts on Switzerland Retail Sales, ) . Source: Investing,.com - Click to enlarge |

Switzerland SVME PMI, October 2016(see more posts on Switzerland SVME PMI, ) . Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,Bank of Japan,China Caixin Manufacturing PMI,China Manufacturing PMI,China Non-Manufacturing PMI,EUR/CHF,FX Daily,gbp-chf,Japan Manufacturing PMI,newslettersent,Switzerland Retail Sales,Switzerland SVME PMI,U.K. Manufacturing PMI,U.S. ISM Manufacturing PMI,U.S. Markit Manufacturing PMI